Spain: Rights at Risk in Housing Crisis

06-01-2014

A woman picks up her clothes from her room after receiving an eviction notice in Terrassa, Spain, October 19, 2012.

© 2012 Samuel Arranda/The New York Times

Shattered Dreams

The dream of owning ones own home has turned into a nightmare of foreclosures, evictions, and over-indebtedness. But its not simply a question of crushed aspirations. Its about government responsibilities to guarantee basic human rights, including the right to adequate housing.

Judith Sunderland, senior Western Europe researcher

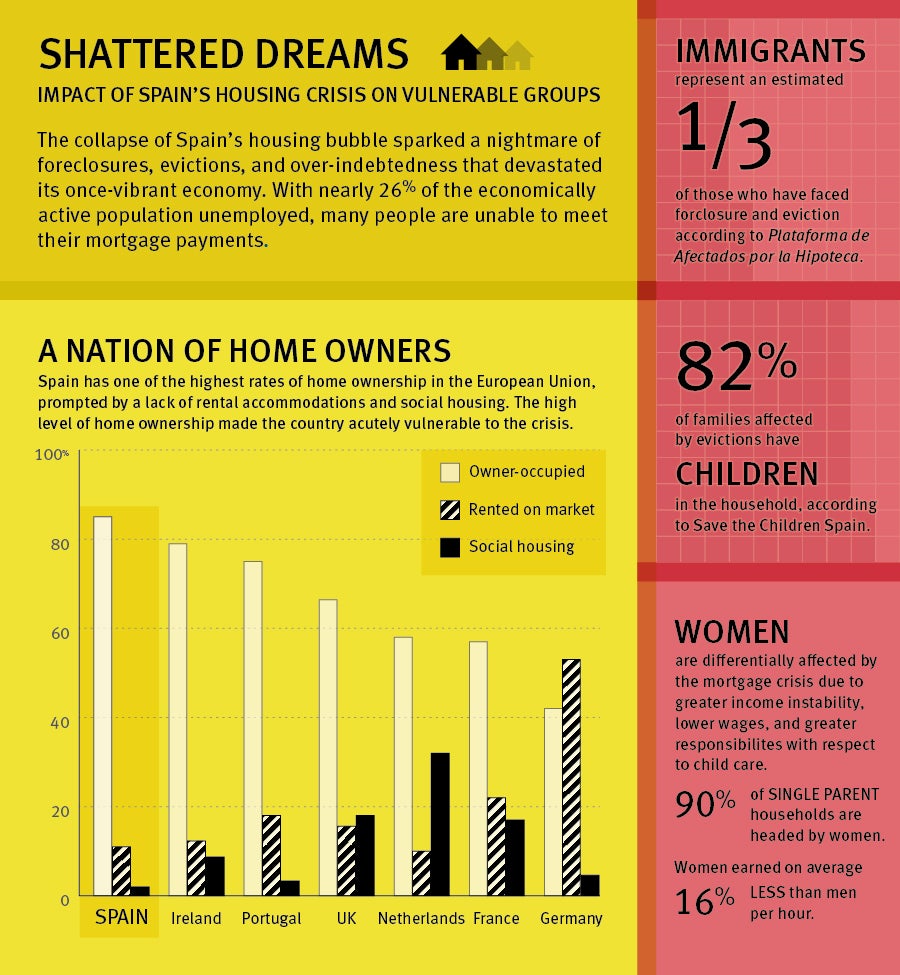

(Madrid) The Spanish government has taken insufficient action to alleviate the impact of the housing and debt crisis in Spain on vulnerable groups, Human Rights Watch said in a report released today. Tens of thousands of families have faced, or are currently facing, foreclosure on homes they bought at the height of Spains economic boom, when irresponsible lending made mortgages easy to come by.

The 81-page report, Shattered Dreams: Impact of Spains Housing Crisis on Vulnerable Groups, documents the hardships faced by families who lose their homes after defaulting on mortgage payments amid Spains economic recession and massive unemployment. The report is based on in-depth interviews with 44 women and men who have experienced or were facing eviction, civil society organizations, and government officials. Immigrants, women who head households or are victims of economic abuse from a former partner, and children are among the affected groups, Human Rights Watch found.

The dream of owning ones own home has turned into a nightmare of foreclosures, evictions, and over-indebtedness, said Judith Sunderland, senior Western Europe researcher and author of the report. But its not simply a question of crushed aspirations. Its about government responsibilities to guarantee basic human rights, including the right to adequate housing.

Spains social crisis around evictions and debt is set against the backdrop of a decades-long history of government policies aggressively promoting home ownership and borrowing at the expense of ensuring an appropriate and affordable stock of rental housing and sufficient investment in rental public housing. Irresponsible lending, unfair terms in mortgage contracts such as exorbitant default interest rates unscrupulous behavior by intermediaries, and the lack of oversight during the boom economic years created a perfect toxic storm whose consequences may be felt for years to come, Human Rights Watch said.

The economic crisis in Spain, with over 5 million unemployed, hit homeowners particularly hard. Spain has one of the highest rates of home ownership in the European Union as high as 85 percent and only 2 percent of the total housing stock is devoted to public or subsidized, rental housing. The recession in Spain followed a construction boom from 1997 to 2007, during which more houses were built in Spain than in France, Germany, and the United Kingdom combined, and real estate and construction constituted as much as 43 percent of the nations GDP.

Daniela, an unemployed single mother, was evicted in May 2011 for defaulting on her mortgage payments. Her oldest son, now 14, started having trouble at school when they faced foreclosure and eviction. He knew everything, she said. The school recommended he see a psychologist. She also went into therapy and took prescription medicine: I felt like I was in a black hole. But I have to have the strength to keep going. I have three kids, I dont have the luxury of being depressed.

Spanish authorities need to adopt measures to help a broader range of individuals and families avoid evictions, secure affordable housing, and ensure access to fair debt restructuring, relief, and cancellation, Human Rights Watch said. The government should move quickly to reform Spains bankruptcy law to provide a fair, accessible pathway to discharging debt. The European Commission should ensure that Spain correctly puts into effect a recent EU directive on mortgages.

Under international law, the right to adequate housing is a component of the right to an adequate standard of living. The right to adequate housing does not include a right to own property, or to retain ownership under any circumstances. It does, however, impose on governments obligations to ensure that policies and legislation progressively realize the right to adequate housing for all segments of society as expeditiously as possible. Affordability is a key aspect of this obligation.

In response to significant public pressure, including by the grass-roots organization Platform of Mortgage Victims, in November 2012, the Spanish government adopted a two-year moratorium on evictions for certain families. The eligibility criteria were slightly broadened in May 2013, but remain too narrow and in some cases conflict with international law. For example, only families with three or more children, one-parent families with two or more children, and two-parent families with a child age 3 or younger may benefit from the moratorium. Under international law, anyone under 18 is considered a child, entitled to the rights and protections laid out in the Convention on the Rights of the Child, including the right to shelter.

A three-year-olds family can stay in their home, but a four-year-olds cant, Sunderland said. The distinction is purely arbitrary and the government needs to have better and more rational and fairer rules.

An estimated one-third of those affected by the mortgage crisis are immigrants, well out of proportion to their share of the population. Many, particularly in the Ecuadoran community, were caught up in so-called crossed mortgages, in which two buyers guaranteed each others loans, and chain mortgages, in which the banks linked together a string of people, often strangers, guaranteeing each others mortgages. In these situations, if one person defaults on their mortgage, it can produce a chain reaction because of the others liability as guarantors.

Women heads of household face greater challenges because of their relatively greater income instability, lower wages on average, and greater child care responsibilities. Women still tied through their mortgage to hostile former partners may face what amounts to economic abuse a form of domestic violence not yet recognized in Spanish law in which the men refuse to collaborate in negotiating with the bank. The impact of housing insecurity on children is deeply worrying. The government has failed to consider adequately the impact on these groups when drawing up policies.

The mortgage crisis in Spain has pushed individuals and families into over-indebtedness because in the vast majority of cases, home repossession by the bank eliminates only a part of the debt. This, combined with the lack of an accessible personal bankruptcy procedure in Spain, leaves many saddled with significant debt they have no reasonable prospect to repay or cancel. Over-indebtedness can have a deeply negative impact on fundamental rights such as the right to an adequate standard of living. Measures taken so far by the government to alleviate the mortgage debt overhang are insufficient, Human Rights Watch said.

Its almost impossible for ordinary people to declare bankruptcy in Spain, meaning overwhelming debt will hound them to the grave, Sunderland said. People living with extreme levels of debt should have a fair chance at a fresh start.

Human Rights Watch wrote to eleven banks operating in Spain for their positions on issues tackled in the report. The views of the seven banks that replied are reflected in the report. Banks have responded to the mortgage crisis in various ways. The majority have signed on to a voluntary code of good practices promoted by the government, and banks have turned over just under 6,000 properties to a Social Housing Fund set up to give evicted families places to live at affordable rents. Restrictive criteria, the poor quality of the units banks have made available, and the fact that in many instances, people would have to move far from their neighborhood and social networks, have undermined this initiative. Just a few days ago, the Fund broadened its eligibility criteria, including allowing all families with children, regardless of their age, to apply.

Governments should be judged on how they manage the human fallout of the economic crisis, not just on macroeconomic indicators, Sunderland said. The Spanish government needs to take a hard look at its policies, and take into account a broader range of people facing social exclusion due to mortgage defaults.