Property Investing Insights

07-28-2015

![]()

More objective guidance and insights for property investors. Our aim is to help you improve your investment returns, flag key risk areas and stimulate strategic thought so you can position your portfolio to maximize gain, for our five thousand website visitors a day and the thousands of people signed up to your Newsletter. This Newsletter cover two key topic

1. The Commodities Super-Cycle What Next

2. Property Investment Trends

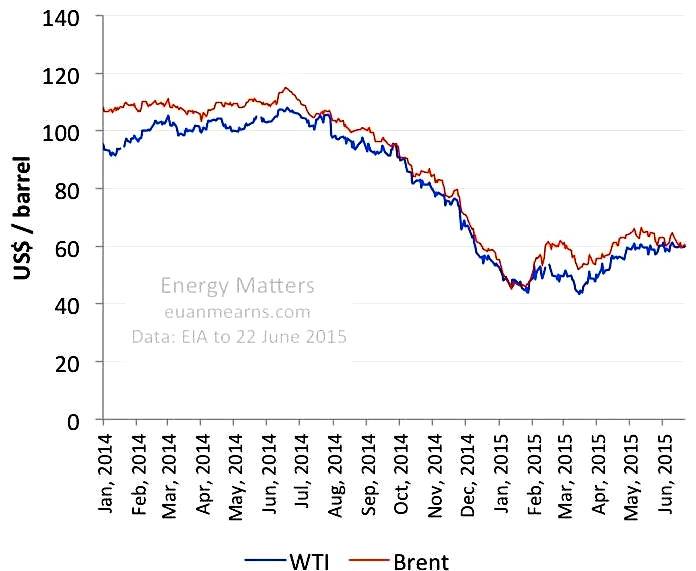

We started in mid 2014 with an oil price crash from $110/bbl to $55/bbl. This has been followed by a gold price decline from $1300/ounce to $1080/ounce and silver price decline feom $20/ounce to $14.50/ounce. Other commodities like sugar, copper, iron, wheat and platinum have also taken a beating.

What has caused this and what is its impact for property investors?

-

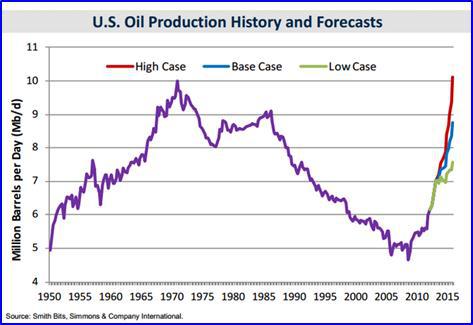

Firstly a glut of oil production was mainly caused by a massive increase of 5 million bbl/day of oil production from the USA over the last five years - from oil shales (multiple hydraulically fracced horizontal wells), coinciding with Saudi Arabia raising output and Russia keeping its production high. Meanwhile Iraq, despite the war in the north of the country, has increased its production and Iran looks like joining the increase after a breakthrough in negotiations with USA/Europe on lifting economic sanctions.

-

Meanwhile Chinas economy has slowed in part because its a maturing economy and its population is no longer expanding. Most economists believe Chinas growth in the use of commodities will drop sharply China might manage to grow its GDP whilst its commodity imports stay at fairly stable levels. The worlds big commodity growth engine has stalled and this could be set to continue.

-

The European slowdown exacerbated by the Grexit on-off fiasco and distraction has not helped.

The dollar has strengthened because many people think the dollar is the best of a bad bunch of currencies at least the US has new and plentiful supplies of oil available at >$60/bbl and remains a real petrocurrency.

Recession: The pessimists would say the decline in commodities is pointing strongly to a recession and the next thing that will happen is a stock market crash and banks getting into trouble again. This is certainly a possibly outcome, at which time gold and silver prices could go ballistic. In this scenario, property prices would come crashing down like they did in 2008. Likelihood 30%.

Boom: The mainstream view is that the US Federal Reserve will be putting up interest rates in the next 6-12 months as will the bank of England as GDP growth and wage levels accelerate a tightening of fiscal policy being required because the economy is doing well. In this scenario property prices would initially increase sharply though the price rises would moderate once interest rates actually rose. Investors have called the end of the commodities super-cycle and believe a robust financial assets cycle is starting: Likelihood 30%

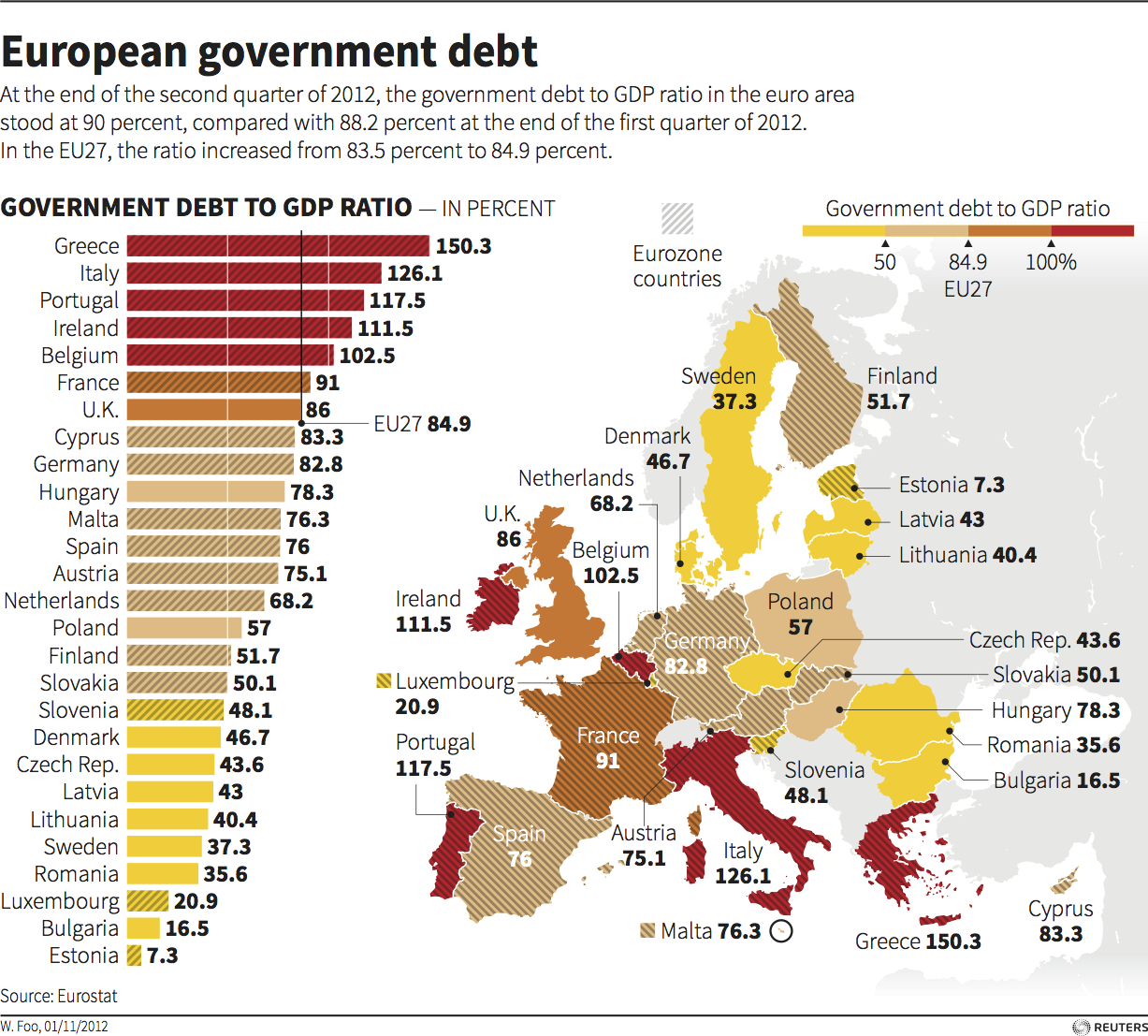

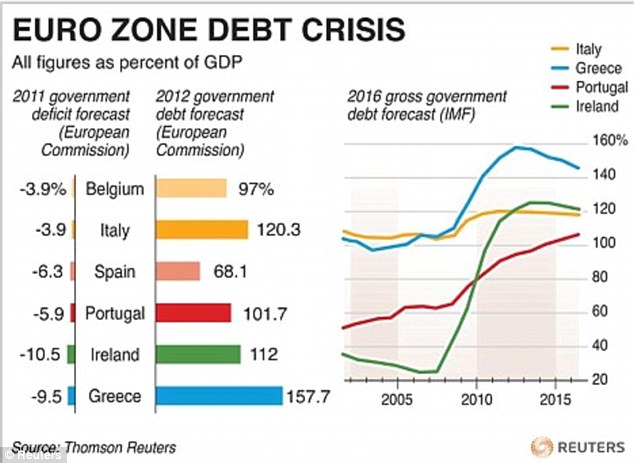

Debt: Its worth highlighting the big elephant in the room which is the gigantic government and private sector debts within Europe (also in the USA). The European Project as always doomed simply because one cannot have different national government and economies with one central interest rate, currency value and trading - without having some countries becoming completely out of kilter to the market. The less competitive less strong economies like Greece having the same currency and interest rates as mighty manufacturing giant Germany is bordering on a joke. The underlying reason for the European Project is commendable - to prevent WWIII - another World War. after the first war in 1915 then second in 1939 - government wanted to combine politically and financially to prevent wars. As the trend unfolds of course we will find the PIIGs country having larger and larger debts - payable to the stronger countries like Germany and to a less extent France. The tensions will mount and how much longer these debts that will never be paid off will be allowed to rise is the big question. For the time being its more kicking the can down the road. The PIIGs countries are bankrupt to all intense and purposes - and their Euro debts will expand as time moves on. If interest rates ever rise, they will be unable to even service these debts never mind pay them off. Of course Greece is unable to pay off its debts even at record low interest rates - an example of how unsustainable it is. Politicians know this. They are trying to keep the show on the road for as long as possible. One day, there will have to be a "reset" or at least a massive debt "haircut" for the bond holders. The European Central Bank is just trying to delay this for as long as possible. This situation which is rather uncontrollable is one reason why more foreign investors are flooding into the UK Sterling and London property. Despite the UK having a bad public sector debt situation - at least it and its banks are on the right path of keeping the government debt down as much as possible. International financiers have confidence in the Tory governments plans - hence they park their money in London. We have "average" debts and are on an improving trend.

Stagflation: Another scenario is the kick the can down the road scenario meaning nothing much has changed. The global economy will not really take off, but muddle along and more bouts of money printing by the Europeans, Japanese, Chinese and then the Americans will be needed to stimulate demand and keep countries from slipping into deflation. In this scenario, interest rates would stay low and property prices would continue to rise - as investors worried about bad debt and the bond bubble, gold prices would rise sharply - possibly followed by oil prices. Likelihood 40%.

Scenarios: You can see that two out of the three scenarios of low oil prices lead to higher property prices - in about 70% of the outcomes. This is good news for the property investor. Low oil and commodities prices should act as a strong stimulus to developed countries particularly those that import large quantities of raw materials like South Kor ea, China, Holland and Germany the manufacturing powerhouses. Low oil prices lead to lower inflationary pressures and less reason to raise interest rates and hence property prices would normally rise sharply as an asset class. Of course if oil prices rose sharply because of supply (or security of supply) issues, property prices would normally drop as the global economy suffered.

ea, China, Holland and Germany the manufacturing powerhouses. Low oil prices lead to lower inflationary pressures and less reason to raise interest rates and hence property prices would normally rise sharply as an asset class. Of course if oil prices rose sharply because of supply (or security of supply) issues, property prices would normally drop as the global economy suffered.

Property Prices: The bottom lines is as long as no major recession hits or financial crisis breaks out UK and US property prices should continue on their merry upward spiral. All the talk of interest rates rising needs to be taken with a pinch of salt Central Banks have been saying this for the last 4 years and they keep kicking things down the road. They dont want to kill off a recovery especially when inflationary pressures are very subdued overall e.g. food, fuel, consumer prices.

Property Boom Super Rich Elite in Super Cities: As we have been saying for years all the money printing will manifest itself in sky high property prices in the super cities as the wealthy super-rich elite are the ones who have access to the almost zero cost floods of cheap cash from money printing sprees and this is then parked in London and New York real estate (or any big city the super-rich invest in Shanghai, Hong Kong, Singapore, Paris, Geneva, Monaco, Oslo, Luxembourg are good examples). Its no use buying property in Newcastle or Baltimore and expecting to see big gains these super-rich elite only buy property in the prime-select locations. We dont believe this trend will change over the years. More of the same is expected as the rich get richer and the poor and middle classes are taxes more and have no easy access to the ultra-cheap printed currency - relying instead on "tickle down" from the elite.

Financial Paper Assets: For London property the commodities decline and shift into financial-paper asset classes like stocks and share and bonds for the time being will stimulate the banking-financial services sector and also help lead to higher London property prices off the back of banker bonuses and financial services profits. Strong economic growth and low interest rates will stimulate the financial classes into bubble territory. It's worth flagging as soon as interest rates start to rise sharply, these assets will become distressed quickly and a financial collapse would be far more likely. Even a 2% interest rate increase could cause real harm now - in view of the massive debts governments now have on their books - along with the private sector, and all the zombie banks propped up by fiat money. This is a consequence of the "too big to fail" policy of saving inefficient banks and business, and public sector entities.

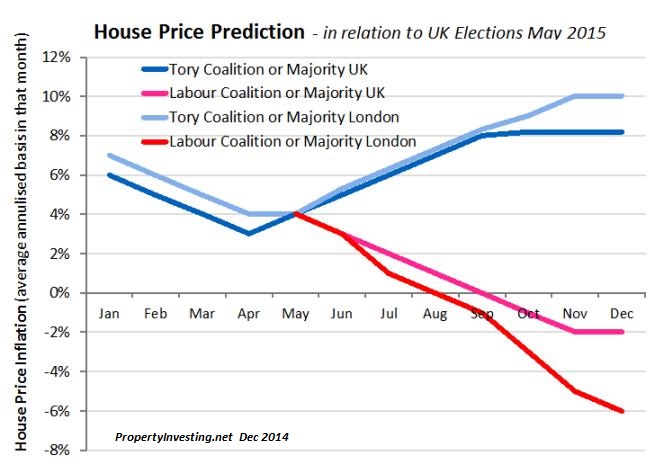

UK Outlook: With a new Tory government installed with a majority for the next 5 years, the Labour party in disarray with no good leader is sight, and turbulence in many developing nations around the world, we still think the global super-rich will be piling into London property for many years - the consequence is you will be hard pressed soon to find any flat for less than £250,00 in the Great London area as the housing crisis continues to worsen and floods of cheap money move into London from overseas. If inflation stays low, oil prices stay low and interest rates stay low then property prices will continue to shoot up for the next few years at least. Dont be surprized by this with oil at $50/bbl and other inflationary pressures so subdued in large part because commodities prices have dropped so much. International investors have great confidence in how the Tories are managing the economy - and the overseas options for a similar government are limited. Despite the UKs fairly poor balance of payment deficit and debts, the improvement in its financial situation and project growth will attract property investment into London as a safe haven - and with it - Sterling's value is likely to strength. This will also be attractive for investors in an uncertain world.

Labour turmoil: The General Election was a defining moment for the UK economy, prosperity and outlook for the next 5-15 years. Two weeks before the Election, most people thought Ed Milliband would be installed into Downing Street with a socialist coalition propped up by the SNP the bookies and experts had this at about 65% chance, as did the Opinion Polls. The Exit Poll changed everyones view within a minute of its release at ~10pm 7 May that Election Night. The Tories actually gained seats and achieved a 9 seat majority. Since then things have gone from bad to worse for the Labour party. Jeremy Corbyn the far left socialist who got enough votes to gain a nomination only 10 minutes before the deadline is now in second posit ion two recent polls have him as a front runner. This despite him being 100:1 to win at the outset and only let in to give the contest some interest and debate in part to highlight what the old school looked like. The Leadership contest has been divisive and the different factions are really starting to fight. Its possible the Labour party could completely split if Corbyn wins Corbyn is likely to be the Unions favoured choice, along with many students. If Corbyn wins, we believe Labour would be unelectable. That sad, if any of the others win, we dont give Labour much chance of ever achieving even a Coalition government in future because of the loss of the Scottish seats to SNP. However, even without these lost Scottish seats, Labour would still not have won the General Election. The Labour turmoil gives the Tories a chance to implement a more right wing series of policies, relatively unconstrained, albeit David Cameron is a moderate centrist who has certainly succeeded in capturing the centre ground, so dont expect anything too radical. In summary. Labour lost for three reasons: 1) no-one could take Ed Miliband seriously as a Prime Minister; 2) most people deeply distrust Labour with the economy; 3) almost everyone dreaded a Labour minority coalition government propped up by the SNP - with its unelected Leader running Westminster (she is not an MP for the UK).

ion two recent polls have him as a front runner. This despite him being 100:1 to win at the outset and only let in to give the contest some interest and debate in part to highlight what the old school looked like. The Leadership contest has been divisive and the different factions are really starting to fight. Its possible the Labour party could completely split if Corbyn wins Corbyn is likely to be the Unions favoured choice, along with many students. If Corbyn wins, we believe Labour would be unelectable. That sad, if any of the others win, we dont give Labour much chance of ever achieving even a Coalition government in future because of the loss of the Scottish seats to SNP. However, even without these lost Scottish seats, Labour would still not have won the General Election. The Labour turmoil gives the Tories a chance to implement a more right wing series of policies, relatively unconstrained, albeit David Cameron is a moderate centrist who has certainly succeeded in capturing the centre ground, so dont expect anything too radical. In summary. Labour lost for three reasons: 1) no-one could take Ed Miliband seriously as a Prime Minister; 2) most people deeply distrust Labour with the economy; 3) almost everyone dreaded a Labour minority coalition government propped up by the SNP - with its unelected Leader running Westminster (she is not an MP for the UK).

Trends: The context to this is that property investors in England and Wales should now plan on the next 5, 10 and possibly 15 years with a Tory government and with it policies that will broadly follow the pattern below:

· lowering taxation (except for buy-to-let private landlords with high borrowing)

· reduced regulation

· decreasing deficits and public sector spending with smaller government

· continued implementation of pro-business policies

· slight reduction in the size of government and public sector

· lower deficits

· lower balance of payments deficits

· stronger sterling

· lower borrowing costs

· stronger financial markets

· booming services sector in London

· continued high levels or net inward migration

· challenge to EU rules and regulations, particularly those affecting the financial sector

· pro-property ownership policies and rights

· broadly pro-landlord and policies

· lower likelihood of widespread buy-to-let and landlord licensing and registration

· freer markets with less regulation and government interference

· pro-private sector home building policies

· lower unemployment, higher employment

· moderate wage growth being capped by immigration and longer working hours

· lower public sector spending

· lower social security payments and spending

· healthier economy of hard working individuals

Outcome - Positive Property Investment Conditions: This is all context for the conditions for property prices movements which look resoundingly positive at the moment because we will get the following economic conditions:

· Pro-business policies

· Pro-wealth creation conditions

· Lower interest rates

· Strong sterling

· Lower inflation

· High GDP growth

· Higher employment

· Low wage growth

· Far more immigration

· Accelerating influx of global super-rich

· Continued non-dom status making London a safe tax haven for the super-rich

· Moderate-low levels of building

· Continued lack of home supply due to planning-environment and "nimby" factors

· Rising rental prices

· Rising house price

· Rising land price

· Rising wages (3%)

· Low inflation levels (around zero % for most of 2015)

Money Flows Into England: These different outcomes and policies are of course inter-linked. Because of the lower deficits and public sector spending, Sterling will be stronger, meaning inflation will be lower and borrowing costs will be lower for longer. There is far less likelihood of a run on Sterling and financial meltdown in the City. Financial markets will look very favourably on the management of the economy when compared to our competition European mainland and the USA. Because the economy will grow strongly in the private sector, employment levels will stay high and demand for housing high. Demand for both rental and property purchase should remain high boosted by record employment levels. The dearth of new housing will put added strain on an already severely constrained market in southern England. More inward migration will occur as the European economy struggles and more jobs are available for EU migrants in the UK. The large inward migration should put some sort of a lid on wage levels particularly unskilled labour. Every year another 110,000 arrive in London and swell its population. This trend is set to continue as young families move in from overseas and existing and new migrants tend to have larger families. If anything the population growth rate will actually accelerate further so in five years time, London will pobably be adding 120,000 people a year. Meanwhile only 35,000 new homes are being build, almost all luxury flats. So for young families, it will be increasingly hard to find for example 3 bedroom houses at affordable prices.

of the economy when compared to our competition European mainland and the USA. Because the economy will grow strongly in the private sector, employment levels will stay high and demand for housing high. Demand for both rental and property purchase should remain high boosted by record employment levels. The dearth of new housing will put added strain on an already severely constrained market in southern England. More inward migration will occur as the European economy struggles and more jobs are available for EU migrants in the UK. The large inward migration should put some sort of a lid on wage levels particularly unskilled labour. Every year another 110,000 arrive in London and swell its population. This trend is set to continue as young families move in from overseas and existing and new migrants tend to have larger families. If anything the population growth rate will actually accelerate further so in five years time, London will pobably be adding 120,000 people a year. Meanwhile only 35,000 new homes are being build, almost all luxury flats. So for young families, it will be increasingly hard to find for example 3 bedroom houses at affordable prices.

Population Boom: Overall southern England will become more overcrowded, with rapid economic expansion that will help with UK Treasury with tax receipts and prevent what would have been high debt levels and financial turmoil had Labour got into power. The downside will be overcrowded public transport, roads and more pressure on the housing situation as the population of southern England continues to boom.

Nimby Rules: Dont expect any real change in the housing situation though the environmental, planning and Nimby factors plus lack of available low cost financing will prevent large new housi ng estates being build. In London we will see more high-rise luxury apartments being built with starting prices of £800,000 or more. But we will not see many affordable homes being built. In London, any apartment that is for sale for say £250,000 at the lower end of the market will see its price rise sharply as wages rise and the housing crisis worsens. More and more people will pack into each flat and home in London. Ex-council flats in central London will be selling for >£500,000 and even concrete ex-council flats will see their prices rise sharply.

ng estates being build. In London we will see more high-rise luxury apartments being built with starting prices of £800,000 or more. But we will not see many affordable homes being built. In London, any apartment that is for sale for say £250,000 at the lower end of the market will see its price rise sharply as wages rise and the housing crisis worsens. More and more people will pack into each flat and home in London. Ex-council flats in central London will be selling for >£500,000 and even concrete ex-council flats will see their prices rise sharply.

There are a few further underlying socio-economic aspects that are helping drive property prices up in London and the UK:

Greek and mainland European turmoil: The uncertainty in whether the Euro will last is making wealthy foreign investors put their money into London and the UK as a safe haven they can also see Sterling rising with the new Tory majority and this further reduces their risk if they purchase London property.

Oil Price: This is having a gigantic effect on property prices. The reason is that oil prices crashed from $110/bbl Aug 2014 to $55/bbl by Jan 2015 cause underlying deflation in food and go ods and some services. This has driven economic growth in the UK a net oil importer and kept a lid on inflation and borrowing costs leading to rising property prices and a big economic boost just as it looked like the world could slip back into a recession mid 2014. The underlying reason for the oil price slid is the boom in shale oil through fraccing in Texas and North Dakota. The bottom line is fraccing is boosting house prices! By supplying cheap oil that has driven normal inflation down and house price inflation up. Of course the converse is true if oil price rise sharply again something to watch out for, though at this time, it looks like oil prices wil stay low for at least another 18 months also because more Iranian oil should be coming to market soon after the sanction start to be lifted end 2015. As we have described many times because, oil prices over $100/bbl are bad for house prices, and oil prices around $50/bbl are very good for property prices in the UK. Its certainly worth keeping a close eye on oil prices.

ods and some services. This has driven economic growth in the UK a net oil importer and kept a lid on inflation and borrowing costs leading to rising property prices and a big economic boost just as it looked like the world could slip back into a recession mid 2014. The underlying reason for the oil price slid is the boom in shale oil through fraccing in Texas and North Dakota. The bottom line is fraccing is boosting house prices! By supplying cheap oil that has driven normal inflation down and house price inflation up. Of course the converse is true if oil price rise sharply again something to watch out for, though at this time, it looks like oil prices wil stay low for at least another 18 months also because more Iranian oil should be coming to market soon after the sanction start to be lifted end 2015. As we have described many times because, oil prices over $100/bbl are bad for house prices, and oil prices around $50/bbl are very good for property prices in the UK. Its certainly worth keeping a close eye on oil prices.

Below for reference are some of our most recent report regarding the oil price:

534: Oil, currency printing and house prices

525: Oil Price Modelling and Impact on Property Investment

523: Oil Prices Crash to $55/bbl impact for Property Investors

519: Oil Price Dropping - Stock Market Crash Warning - Start Of Recession

518: UK Oil Production Collapse and Deficit

Fraccing Prevents Global Recession: We dont know what happens behind the scenes with the ruling elite, but one scenario is that the USA and Saudi Arabia collectively saw that high oil prices at >$100/bbl were cause severe damage to the global economy and they were worried about China, Europe and oil demand in mid-2014 and that the world was heading into recession. The USA had flooded the market with shale oil from fraccing, but Saudi could have reduced their oil production but chose to increase it causing an oil price collapse to $55/bbl. Most people think they were going for market share, but some people think they wanted to secure a long term oil market, boost oil demand whilst preventing the world from collapsing into a recession. The $55/bbl have had the desired effect of boosting demand and the global economy and reducing the possibility of interest rate increased through higher inflation. Just when it looked like a recession was on the horizon mid 2014, lower oil prices came to the rescue. This was only possible because of a 5 million extra barrels available since 2010 from USA oil shale fraccing. So one could argue faccing came to the rescue and prevented the global recession.

Fraccing Good For Environment: For those that believe fraccing is environmental damaging, consider this. The USA has quietly been drastically reducing its CO2 emissions because of a switch from coal to natural gas this was only possible because the shale gas fraccing boom 2005-2012 which sent gas prices down from $12/mmbtu in 2007 to $3.5/mmbtu in period 2009-2015. Meanwhile Germany with all its investment in Renewables has been the biggest developed increaser of CO2 emission because it switch from Nuclear to Coal burning after Fukushima. So the message is fraccing leads to low priced gas that then replaces coal and cleans the environment, both CO2 emission, soot and reduces deaths due to coal mining accidents (running at thousands a year worldwide). Anyway, we can understand in the UK why people dont want to see fraccing in their back-yard since it leads to more lorries, some minor development in pristine countryside and the perception of industry which can lead to property prices declining (in a similar way to wind turbines) so dont expect UK shale gas to take off. There are simply too many Nimbies and faccing seems to be something that attracts more radical movements that want to demonstrate about the government. In the USA the are vast tracts of desert with hard-up farmers that are only to delighted to get a cut of revenues and see the jobs boost in their de-populated areas. Also in the USA the oil/gas industry is in general favourably received since they understand it means prosperity and jobs and the USA was built on this foundation. But in the UK, the gas/oil business seems to be met with dis-trust, so dont expect any movement in shale gas for at least the next 5 years.

Globalized Money Circulation Impact on London Property. Ever since the financial crisis of 2007-2008, Central Banks have been printing digital money out of thin air. Its not worth the paper its not printed on some say. This colossal money and debt mountain prevented economic collapse in 2008 but the consequence was a developing bubble in asset prices. The most wealthy 3% own over 50% of all assets globally and as wars have spread through the Middle East of relatively stable autocratic regimes crumbled (Tunisia, Libya, Egypt, Syria, Iraq) the wealthy elite have looked to place their wealth into safe haven assets. They have shifted wealth to places like New York, London, Geneva and Singapore. They have done this to protect their family wealth and from seizure by new governments. This has help drive central London property prices into the stratisphere. If Labour had g t into power, they would have targeted the wealthiest 5% - particularly the overseas investors. But since the Tories gained majority power they are unlikely to want to drive wealthy overseas investors away to competing cities like Geneva, Paris, New York. Ys, they will try and increase their tax take and gain their fair share, but not enough to drive these people away. Lets face it, London has the most interesting culture, nightlife, tourism, history, shops and best education, open diversity (schools, Universities) compared with the competition and we speak English so its no wander people from all around the world invest in London property. We simply dont see this changing in fact, if anything we see this accelerating as people realise that the Tories will be in power likely for the next 15 years and their investments will be relatively safe. Hence just dont be surprized to see central London property prices rising even more sharply from id 2015 onwards.

London Festivals: Another great attraction for London is its festivals that seem to get better and more frequent as years go by. For the rich super elite, its easy to be accepted on t his festival social circuit simple because no-one really cares about background most Brits are very open. So the whole summer period is packed with pleasures like for example:

his festival social circuit simple because no-one really cares about background most Brits are very open. So the whole summer period is packed with pleasures like for example:

· Henley regatta

· Oxford and Cambridge Boat Race - Putney

· Wimbledon

· Queens Club tennis (Barons Court)

· Chelsea Flower Show

· Tate Gallery shows

· Ascot, Epsom

· Wentworth and Sunningdale Golf

· Glastonbury Festival (Somerset)

· Cricket

With this as context, its still possible to buy one bedroom flats in places like New Cross for £250,000 that is only 1½ miles from the City, so although most people talk about a London property bubble, we actually thing its got some way to go particularly as price rises continue to ripple out to places like Bexley, Tooting, Enfield, Mill Hill, Sutton and Upminster.

We hope this Newsletter is helpful as part of your property investing toolkit and provides some interesting perspective - has helped stimulate some positive thoughts on how to improve your business. If you have any queried, please contact us on enquiries@propertyinvesting.net .