Eight legal ways to sidestep inheritance tax

09-11-2018

This promotion by southbankresearch.com while not financial advice should be read carefully. It contains the important information, facts and figures you need to make an informed decision including the risks to your capital involved about our research. If you are unsure whether this type of investing is right for you, seek independent personal financial advice.

Former Wall Street insider reveals

Eight legal

ways to sidestep

Inheritance Tax

(And ensure your kids NEVER need to pay a penny to HMRC!)

HURRY: less than 100 copies remain today

£325k.

Thats when they start bleeding you dry

Helping themselves to all the money that youve left for your kids.

Its infuriating isnt it?

Youve worked hard all your life.

Youve saved diligently for your loved ones after youve gone.

Youve planned and set things aside.

Youve done everything you should. Everything youve been told to do.

Then the moment youre gone, HMRC come knocking

Saddling your children with a huge tax bill at the worst time of their lives.

And that £325k

That includes EVERYTHING you own.

Your house, your savings, your cars, your holiday home, your stocks and shares, your assets, your art collection

Literally everything.

Its all fair game to HMRC. Theres nothing they wont pilfer.

Theyll claim their slice of the pie 40% of your entire estate whether you like it or not.

My guess is your personal estate is way over the £325k threshold.

If you own a reasonably sized family home it almost certainly will be

Meaning, unless you keep reading this letter

Your kids will get stung after youve gone

Death tax is a veritable cash cow for HMRC.

Between 2017 and 2018, British citizens coughed up over £5.2 billion to the government.

You read that right £5.2 BILLION.

Thats £5.2 BILLION theyre taking from people in mourning!

To my mind, its not right.

As part of Britains largest underground investment research network, I want to show you EIGHT ways you can protect whats rightfully yours.

And ensure that when you go, your assets will benefit your loved ones as you intended them to

And NOT the taxmans coffers.

You wont read about these tax secrets in the mainstream arena. Youll likely have never heard of them, or even thought about them before.

Thats because our government doesnt want you to know about them.

Some might see them as "fringe" or "controversial". But these ideas are often the most lucrative too.

When you claim your exclusive guide today, youll discover EIGHT under-the-radar wealth "shields" that you can action today, including:

- How to ensure your children wont ever need to pay a penny to HMRC

- The "off-market" shares you can raid to supercharge your tax relief

- The "gift" you can make to shield a portion of your wealth from the taxman

- The niche property sector thats 100% exempt from "death tax"

In a moment, Ill show you how to keep HMRC at bay, and secure your loved ones future.

First, let me quickly introduce myself

My name is Nick Hubble

Ive been on the inside at Goldman Sachs, and Ill tell you now

The system is rigged against YOU.

The government bankers fund managers theyre not in it for you.

Theyre in it for them thats just a fact.

Theyll use you as a means to an end

Squeezing you for as much as they can to cover their backs on whatever scheme theyre running

And to collect their fat bonuses, year after year.

Its one of the reasons why I left Wall Street to become a senior strategist at the British division of an underground, global investment network.

I want to help regular investors like you make money.

As well as here in Britain, we have offices across five other continents, and an unrivalled stable of investment experts.

These include a former US government adviser, former Wall Street fund managers, a Pulitzer-nominated scientific journalist .

Cryptocurrency experts master traders, award-winning investors bestselling authors

One of our guys is the former chairman of the International Federation of Technical Analysts

Another managed £3 billion in client capital for HSBC

But youll probably have never heard of us

We dont pay to advertise on TV or in the press. And we dont receive marketing revenues from any outside agencies either.

We exist solely to help YOU make money.

Its an unusual business model.

And it demands that our investment research is better and more original than anything else out there.

In our 36-year existence weve grown from a tiny startup into a vast multinational organisation

Our London division has rapidly become the go-to place in Britain for alternative investment ideas

Including on income protection value investing breakout tech-stocks big picture portfolios retirement and more

All told, weve helped over 100,000 British investors make the most of their money.

Including people like AB who said:

Your services have helped improve my overall savings and retirement funding, and I hope that applies to many others

Another reader wrote in to say:

One of the best things I did this year (2017) was to subscribe to the amazing information and opportunities you guys provide

Plus Kevin, who said simply:

My experience has been excellent. I plan to remain a subscriber for a long time to come

Now we want to help you.

You might be surprised at the options available to you chances are you wont realise theyre even on the table.

And Ill say now

There are two things Id like to share with you that you need to act on immediately.

But keep in mind, when you claim your report:

Eight legal ways to sidestep Inheritance Tax (And ensure your kids never need to pay a penny to HMRC!)

Everything youll read inside is above board and 100% legal. Its all based on current laws (that could change in future)

It all flies well beneath the radar of the mainstream financial press...

And our government doesnt want you to know about ANY of it.

Thats because they want to take as much from you as they possibly can.

In fact

Your family could be forced to

get a loan just to survive

Do you know what your current net worth is?

Or more importantly, how much your family will have to fork out to HMRC in the event of your death?

Well you should

Karen, 64 years old from London*, was shocked when her partner died suddenly.

Unfortunately, shed done nothing to prepare for the possibility of an inheritance tax (IHT) bill in the event of his death and neither had he.

As she flicked through the 50-page IHT guideline document for the first time, she realised that her deceased partners bank accounts had already been frozen.

She had no means of paying any of his bills (aside from the funeral an HMRC "exemption").

She wasnt allowed to sell his properties, or settle ANY of the final utility bills until the IHT penalty was paid in full.

The total amount?

On their £1.1 million estate, an eye-watering £440,000.

When she asked how she was expected to cover the £440,000, she was simply told to get a loan.

Eventually, months later and with mounting legal bills, Karen finally settled the £440,000.

Its £440,000 that shell never see again

£440,000 that will benefit the state and NOT her children

And during a time when she was grieving, that £440,000 was like a noose around her neck.

Think about that for a moment

What if you go, and leave your kids in the same boat? Would they cope?

Its something you shouldnt be leaving to chance.

Especially when you consider that

HMRC wants its share of your money BEFORE your children can even touch it!

Thats right

To be 100% clear, Karens example isnt a fictional account. Its a true story and its not a one-off. Its standard practice.

The taxman wants his money fast.

He issues his demand for settlement immediately.

BEFORE any assets have been passed on to your children.

So whatever your IHT liability is, it needs to be paid to HMRC before your family receives a penny from your estate.

Often, as with Karens case, the only means for them to pay will be from the assets within the estate itself.

So if its tied up in property, or stocks whatever your kids will need to find a way to pay the taxman, without touching anything within the "death estate."

That could mean having to endure the pain of selling off their own family home, their vehicles, or even their own business.

And HMRC demand its share is paid in full, within just six months of you passing.

After that, the interest starts.

As I said, the system isnt set up for your benefit. Its set up to benefit THEM.

And theyll stop at nothing to collect their dues

Theyll even tax you on money

youve already paid tax on

In a lifetime, the average household in Britain pays over £825,000 to the taxman.

Look at how much tax youve ALREADY been forced to hand over to HMRC.

Your wages are taxed by up to 45%...

Any profits you make from investing theyre taxed 25%

When you buy a house the stamp duty is as much as 13%

Whenever you drive your car you pay road tax

Then theres council tax National Insurance the list goes on and on.

And then when you die, the things youve already paid tax on are taxed again.

Worse still, its your family who has to foot the bill in the event of your death.

No one likes the thought of their relatives being chased for money after theyve gone.

But the only way to ensure the taxman cant get his mitts on your assets after youve passed

Is to get your affairs in order NOW.

For many, the realisation that theyll face a problem with IHT is something that creeps up on them.

Often, its too late in life for them to do anything about it, which can lead to a nasty surprise.

And the shocking truth is

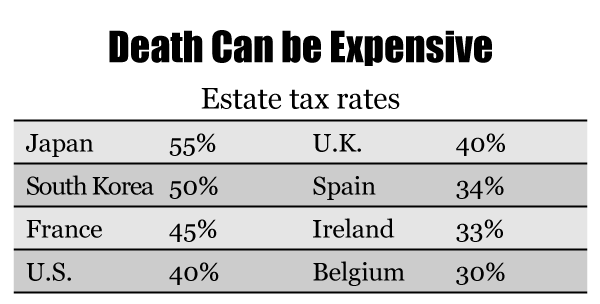

Here in Britain, were among the worst off on the entire planet when it comes to IHT.

In fact

Britain is the fourth most expensive

place to die on Earth

You might have thought that a hefty IHT bill was par for the course whatever country you live in.

Its not.

In China, India, Russia, Sweden and even Australia

Your estate isnt taxed at all. And your kids dont have to pay a penny after youve gone.

Even in places like Italy and Austria the amount theyre liable for is an absolute pittance compared to what we have to cough up here in Britain.

And I should know

My parents have moved to Austria and Australia largely to sidestep IHT.

source:taxfoundation.org

As you can see from this table, only three countries on Earth pay more IHT than Britain

Japan, South korea and France.

I dont know about you, but it makes me feel like were being robbed blind!

Is it fair?

No.

Can you do something about it?

Yes.

But you need to put a long-term plan in place, beginning right away.

Some of the things youll read about in your exclusive report require immediate action.

The longer you wait, the less chance youll have to use them to your advantage.

This isnt something that you can sit back, forget about and just hope itll work itself out. That wont fly.

Your family WILL pay the price, if you fail to act.

Its that simple.

But follow the ideas in your report closely, and your children may never worry about having to paying a single penny to HMRC after youve gone.

In a moment Ill show you how to claim your copy, but first, let me ask you a question

Do you want to be clobbered by HMRC or leave your wealth to your loved ones?

It should be an easy one for you or anyone in Britain to answer.

But the figures tell a different story

More people than ever before are leaving their estate to the taxman, and not their loved ones.

Between 2010 and 2017, the number of families paying IHT in Britain is up 160%. By 2020 it's forecast to nearly DOUBLE again.

As I said, in the last year we paid £5.2 billion in IHT to the taxman a record.

And as you can see from this chart, the rising value of property in the UK is one of the main reasons why more and more people are now above the IHT threshold.

.png)

Their assets are at the mercy of the taxman.

Maybe yours are too?

Well they neednt be.

So

Let me show you how to turn this situation to your advantage

Your family can prosper from your estate after youve gone.

Theres one simple move you can make TODAY that will ensure your kids will never have to worry about covering an IHT bill in the event of your death.

Its the first thing youll discover in your report, titled:

Eight legal ways to sidestep Inheritance Tax (And ensure your kids never need to pay a penny to HMRC!)

Its something you probably wont have thought about before. You probably wont read about it in the mainstream financial press either

- It DOESNT involve investing in stocks

- It DOESNT involve setting up a trust

- It has NOTHING to do with property

- You DONT need to "gift" anything to anyone

- And you DONT need to change your marital status or anything significant like that

In fact, this is something that you can do easily today in no more than a couple of hours.

Its not overly complicated. Its 100% legal, and its ethical. Its not even a loophole. Its just something many people dont know about.

And I want to get you up to speed right away because, without giving too much away here the sooner you can act, the better.

In your exclusive report, Ill reveal all.

Along with seven other steps you can take to ensure this whole situation plays out favourably for you and your family.

In a second Ill show you how to get hold of a copy quickly and easily.

But right now Id like you to understand what were all about here at Southbank Investment Research.

And explain why weve produced this exclusive guide that you can claim today.

Introducing our first-of-its kind investment advisory

There are ALWAYS ways to protect your money from the clutches of the government and our fragile financial system

While making potentially enormous returns at the same time.

You have to be bold think differently and be willing to consider ideas that you simply will not read about in the Financial Times or Bloomberg.

Some regular investors may see these ideas as too out there

The fact is, there has NEVER been a better time to start thinking like this and to start preparing for things that could help your family prosper, after youve gone.

Safeguarding whats rightfully yours NOW is just the start.

In your exclusive guide, well show you how your family can avoid paying inheritance tax altogether.

But theres a lot more Id like to show you today

Including the secret, profitable actions you can take to secure long-term wealth. And to protect what you have in the wake of potential financial disaster.

Or in other words

To get a portion of your money "off-grid" and OUT of the broken financial system by any means necessary

To share the ideas that could turn potential financial disaster into jackpot events for you and your family

To show you the secrets to making money no matter how bad things get in the financial system

In Zero Hour Alert we share these ideas with you on a regular basis.

And if youre worried about your family being stung with a devastating IHT bill later in life

Or the fragility of the global financial system

Its absolutely vital reading.

Its headed up by me, Nick Hubble, and my colleague Boaz Shoshan a man who has personally helped manage millions of pounds of wealthy clients capital.

Put simply, our aim is to show you what you wont find elsewhere: the unvarnished truth about our establishment and our fragile financial system and the steps you need to take to survive and profit from it.

Each month as a Zero Hour Alert reader you'll get a REAL insight into what's happening in the global financial system...

Paired with actionable ways of turning those problems on their head and getting a portion of your money OUT of the broken system for good.

Chances are these "alternative" financial moves will help you sleep a lot better at night and could end up making you a hell of a lot better off.

The bottom line is:

I dont want the government to take your money.

I dont want you to be hurt by the fallout from the next potential financial crisis.

So I want to show you the simple measures you can take to ensure your money isnt at the mercy of the taxman, or our fragile financial system

Starting with your exclusive report: "Eight legal ways to sidestep Inheritance Tax (And ensure your kids never need to pay a penny to HMRC!)".

Remember what youll discover the moment you read your report:

- How to ensure your children wont ever need to pay a penny to HMRC

- The "off-market" shares you can raid to supercharge your tax relief

- The "gift" you can make to shield a portion of your wealth from the taxman

- The niche property sector thats 100% exempt from "death tax"

Before you claim your copy however, I should remind you that this is a strictly limited offer

Less than 100 copies are available today and I expect them to be snapped up quickly.

My advice to you is:

Take action immediately.

If youre serious about protecting your "death estate" then you need this report in your hands right away.

And the moment you say the word, youll get an extra bonus

An automatic

30-day no-obligation FREE trial of our first-of-its-kind investment advisory, Zero Hour Alert

You wont need to do a thing after youve claimed your copy of your inheritance tax report.

Youll instantly begin receiving our latest research in Zero Hour Alert for FREE

And youll get all the benefits of a fully paid-up member without having to make a long-term financial commitment.

Heres whatll happen, the moment you claim your exclusive inheritance tax guide:

- Ill rush you over your report: "Eight legal ways to sidestep inheritance tax (And ensure your kids never need to pay a penny to HMRC!)"...

- Youll begin your FREE trial of Zero Hour Alert and receive your first issue direct to your inbox

- Youll get access to the members area where you can read all the past issues and get all the latest updates

- Plus youll be able to get in touch with me and my team directly with any questions you may have about inheritance tax or anything else you read in Zero Hour Alert

As I said, thats all yours under no obligation for the next 30 days.

And its all yours to keep regardless even if you decide Zero Hour Alert isnt for you.

So read your exclusive report and all the past issues

Check out our latest updates and decide whether Zero Hour Alert is right for you.

As you know

Here at Southbank Investment Research, our insiders are the best in the business.

Some of our guys have walked away from managing hundreds of millions in client capital for some of the worlds biggest institutions to come and work for us.

Our founder Bill Bonner has written bestselling books and made award-winning documentaries.

He doesnt publicise this of course: advertising isnt what were about.

Were a private intelligence network for investors who are serious about making money.

Our goal is bring you original, independent investment research that could help you achieve your investment goals and more.

Im talking about the kinds of ideas that you certainly wont find elsewhere.

Ideas that the establishment dont want you to know about.

Sidestepping "death tax" legally is just the start. Its one of the first things you need to do to safeguard your next generation of family wealth.

But I also want to go a step further

And in addition to your inheritance tax report and FREE no-obligation trial of Zero Hour Alert

I want to send you a FREE bonus report

Its titled:

Stealth Wealth: Four Ways to Get Off the Financial Grid.

And itll introduce you to ways to move your wealth away from the fragile system, out of the hands of the taxman, sheltered from politicians and immune to whatever happens in the markets.

The moment you read it, youll discover

- The exact amount of cash you should put aside as an emergency fund (and the exact denomination you should use too)

- The particular types of gold bullion you should buy and types you should avoid. (Case in fact: you do NOT want to buy 99.999% pure gold. I show you why)

- The secret hidden system for buying gold anonymously

- How to transfer wealth anonymously without detection including the four-step process you need to follow to get started

- One of the only investments that: (1) can be consumed, (2) can be sold, (3) performs well, (4) can be held for long enough to survive a financial crash, (4) diversifies your wealth, (5) has a big demand, plus much, much more...

Everythings revealed inside your bonus report.

Its yours for FREE the moment you claim a copy of our IHT guide and begin your FREE trial subscription to Zero Hour Alert.

This is an unmissable opportunity for you to ensure your family is set up for life after youve gone.

But only the first 100 people who contact me today will receive their guides and a no-obligation trial of Zero Hour Alert.

This is a strictly limited run, so if you are interested then dont wait around.

Everything youll read about in your reports will give you an enormous edge over 99% of other investors out there.

But I should point out: all of the moves outlined in these two reports come with their own risks attached.

Thats why you should always think carefully when you invest your capital. Any investment involves risks that could result in you losing money. The value of any investment can go down as well as up.

The question you have to ask yourself is:

Whats the REAL risk to your capital?

My answer is having it at the mercy of the taxman, or tied up in a broken, corrupt and fragile financial system.

Making a few simple moves to ensure your wealth benefits your family and not the taxman

Plus taking 1-2% of it OUT of that system, is just good common sense to me.

Im sure you agree.

But the fact remains, doing this isnt risk free.

You will need to plan carefully, and some of the ideas in your exclusive inheritance tax guide may require professional assistance from your IFA.

Plus alternative investments can be hard to sell. In financial jargon this is known as being "illiquid". It means if you need to sell something in a hurry, it can be hard to find a buyer quickly. That's part and parcel of having some of your capital outside the system. It's not the same as a share portfolio you can cash in with a few clicks of a mouse.

To state the obvious: that's the whole point. The financial system itself is built on instant liquidity and vast numbers of buyers and sellers. That's the benefit... though it comes with its own risks, as we've been discussing.

Getting out involves different risks. Another is many "alternative" investments aren't regulated or covered by the Financial Services Compensation Scheme or Financial Ombudsman. That means you dont have the same level of "protection" as you would with traditional investments.

I think the risks are worth it. And once youve read your exclusive reports, I think you will too.

So lets get our work into your hands right away. Because the fact is

This is information you wont

find ANYWHERE ELSE

Thats a shameful indictment of our leaders, our media and our economists.

But its the sad truth.

Look at the Wall Street Journal. Look at the Financial Times. Are they providing real, practical steps to help people sidestep in legally, and to get your wealth off the grid?

No!

Most media outlets dont even cover stories like this. Thats because the establishment has a vested interest in the status quo.

Most analysts would rather toe the line and pretend the academics, politicians and economists in charge of the system have everything under control, and that the systems working just fine for everyone.

But the truth is

Its set up to benefit them and not YOU.

People dont want to hear whats really going on.

Government doesnt want to hear it. Theyre the biggest debtor on the planet. They dont want to hear the end of the credit bubble is coming because they wont be able to borrow anymore!

There are almost no serious financial actors who want to see the truth and want to talk about the truth.

Its only we the independent financial publishers that can honestly report on whats going on. And show people how to prepare.

We dont take advertising. Were not part of the financial industry. Were not economists who are paid to look the other way. And were not big government.

Were the only ones who are willing to tell the truth.

Thats why more 100,000 people pay to read our work here in the UK.

And its why we have such a loyal following of investors and savers.

In fact, since we started publishing our alternative ideas and insights, weve opened a lot of peoples eyes to whats really happening in the financial world.

As one reader put it, our work is:

A must read to REALLY understand what a calamitous situation we are living in growing worse by the day and intensifying exponentially. ITS A WAKE UP CALL and NOT TO BE IGNORED! Failing to prepare is PREPARING TO FAIL!

Another summed up my attitude to crisis preparation exactly, saying:

Dont trust or rely on the government but take action yourself to prepare for financial Armageddon.

For some readers, our work is nothing short of life changing. This note alone made every word we publish worthwhile:

Throughout some of my darkest moments of despair I have turned to reading your emails, not only as a search for 'a way out of the rat race , new forms of income, and a way of working from home' but also a source of positivity on which to focus.

Instead of being a crumbled wreck drowning in tears, torment & worry I read your emails and I am filled with a sense of encouragement, hope and determination that I can do this, albeit alone... I can & will turn things around for my little man & myself!

With hindsight one of the best things I did this year (2017) was to subscribe to the amazing information and opportunities you guys provide!

A HUGE thank you & hug for all the information & 'inspiration' you have given me in my search for a new beginning.

One reader even wrote to tell us that thanks to our joining the dots hed made his first million from our recommendations!

Believe me: nothing makes me feel better than receiving notes like these.

But I have to tell you, right now, I am really worried that a lot of our subscribers and many, many ordinary investors are going to get caught totally by surprise by inheritance tax, and when the next inevitable crisis hits.

That's why we created Zero Hour Alert.

And that's why I'd like to send you the full details on exactly how you can turn this situation to your advantage.

That all starts with my invitation to you today.

Just say the word and

Ill send you your inheritance tax guide and get you started with your FREE no-obligation trial of Zero Hour Alert immediately

In fact, heres everything youll get, right away:

1. EXCLUSIVE GUIDE: Eight ways to sidestep inheritance tax (And ensure your kids never need to pay a penny to HMRC!). Worth £50.

Plus, youll automatically begin receiving

2. MONTHLY RESEARCH: on the first Friday of each month we'll send you your monthly newsletter, Zero Hour Alert. We'll keep you up to date on exactly what's going on regarding this financial crisis, and show you some unusual and incredible ways to make money now and as it begins to unfold. Youll get complete, unrestricted access to the Zero Hour Alert members website for the whole of your 30-day trial (worth £99).

Plus as an extra special bonus, youll also get this FREE report (worth £45):

Stealth Wealth: Four Ways to Get Off the Financial Grid.

I'll also keep you up to date on what I am doing to protect myself. I'll make sure you stay abreast of changes to the inheritance tax laws and government interventions.

But thats not all

Every day the markets are open, youll receive our "paid subscribers only" e-mail called Southbank Investment Daily.

In short, we report on all the work we are doing... the most interesting investment ideas... what we're researching now... and what we expect to happen in the months to come.

Our publisher, Nick OConnor, sits down and writes this email every morning himself. It's free for paying subscribers of our work... but it gives you an insight into the network and thinking behind our research.

Now Im sure youre wondering

How much does this Zero Hour Alert package cost... and how can you get started?

Well, a one-year subscription to Zero Hour Alert normally costs £99 per year

Factor in the value of your inheritance tax guide and bonus report (£95 value), and thats research worth £194

But right now you can get everything (worth £194), for just £4.50.

Why so cheap?

Well, to be honest, our business really only works if our subscribers stick with us for the long-term. But we realise you've got to try our work first, to see if it's right for you.

And that's why, through this letter, we're making it so cheap, and so you can try it with no obligation.

Let me be 100% clear

You'll receive your exclusive guide:

Eight ways to legally sidestep Inheritance Tax (and ensure your kids dont pay a penny to HMRC)

Immediately.

Thats yours to keep regardless.

Then youll have the next 30 days to see if Zero Hour Alert is for you or not.

Youll get access to EVERYTHING. All the back issues, the special reports, the members area .

And within your 30-day no obligation trial youll also receive the next issue of Zero Hour Alert...

Try it for 30 days, if you like it, you dont need to do anything and well automatically renew your subscription for a year at the knock-down price of £49, saving you £50.

In other words, by taking me up on this offer, you are agreeing only to TRY my work to see if you like it.

Plus dont forget your BONUS report:

Stealth Wealth: Four Ways to Get Off the Financial Grid.

Both reports are yours to keep regardless even if you decide not to continue beyond your trial.

I cant say fairer than that.

I know it will be one of the best financial moves you ever make.

And the very fact you're still reading this letter tells me how seriously you're taking this.

That means youre exactly the kind of investor I want to be working with, and for.

Now there's only one thing left to do

Youll still get to review everything on our secure order form.

But once youre happy, enter your details at the bottom of the form and your order will be processed immediately.

You'll have access to all of our work in a matter of minutes.

But please remember, only the first 100 investors who contact me today will be successful.

So please dont wait around.

Click here now to get started.

Best,

Nick Hubble,

Chief Strategist, Zero Hour Alert