GETTY

Things have been getting increasingly tough for Britains buy-to-let owners. Tax relief is evaporating and legislation like the recently-minted Tenant Fees Act has increased the costs for landlords. Reams of additional regulation have hiked the amount time and effort required to make their properties habitable, too.

The emergence of Covid-19 has pushed the pressure dial up even further for buy-to-let investors. Mortgage payment holidays allow them to absorb the financial blow of renters who are unable to pay their accommodation costs today. But the rules only cover deferrals for three months and so offer landlords limited peace of mind.

Its a particularly difficult time for individuals whose rental properties are sitting vacant. Government lockdown directives may have loosened over the weekend, but there is still no word on when lettings agents can begin organising viewings again.

Finally, a ban on tenant evictions remains in place, putting the kibosh on any plans buy-to-let owners may have to sell or upgrade their property or to change the terms of their lettings.

Today In: Markets

Back To Work: Focus On Efforts To Reopen Takes Center Stage Amid Second Wave Fears

Stocks Fall As Investors Anticipate Rocky Reopening, Possible Coronavirus Second Wave

Simon Property Group Is Trading At A Historically Cheap Price

Yields Rise In Parts Of The UK

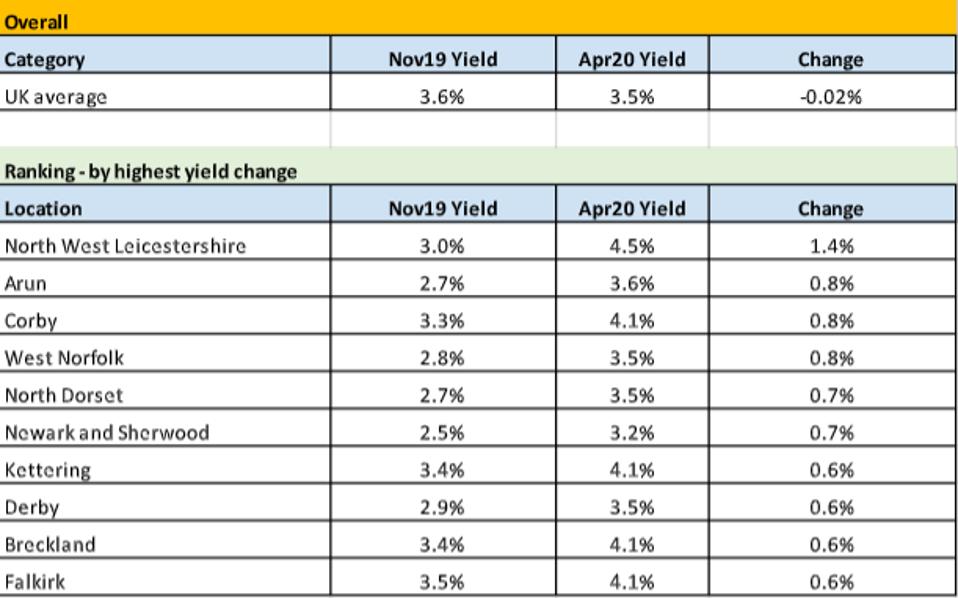

Its not all bad for landlords, though, as rental yields have held up in the face of the coronavirus crisis. Data from Howsy shows that the average yield has dropped just 10 basis points since December. It now sits at 3.5%.

In fact, the lettings management platforms latest study shows that yields have continued to boom in many parts of Britain.

Howsy predicts, too, that yields could pick up in the UK looking further down the line. It suggests that a fall in property prices, allied with high rental demand, could push investor returns higher.

That said, buy-to-let is not an asset class Im prepared to invest in. Government efforts to reduce buy-to-let returns have reduced landlord profits to a trickle in recent years. And the attack is likely to keep intensifying as lawmakers try to solve the supply shortage that first-time homebuyers are experiencing by forcing landlords to sell up.

I think potential buy-to-let investors would be much better off using their money to buy stocks instead. There are many reports out there revealing that long-term stock investors those that tend to buy their shares and then hold them for a minimum of 10 years tend to make double-digit annual returns.

The latest study from Vanguard Investment Management for example shows that these equity investors can expect to make returns of around 9.9% each year. Compare that to the current 3.5% rental yields that Britains landlords enjoy. And of course that latter figure fails to take into account buy-to-let costs like maintenance, insurance payments, mortgage instalments and the like. This is why I myself much prefer to invest in equities.