534: Oil, currency printing and house prices

03-21-2015

PropertyInvesting.net team![]()

Energy Costs: A large part of the dynamics around the global economy is driven by energy costs. In times of high oil and energy prices, in the western developed nations that use huge amounts of energy per capita, the economies will often see:

-

High food and fuel inflation

-

Low GDP growth

-

High unemployment

-

High interest rates

-

Suppressed disposable incomes

-

High mortgage and lending costs

-

Lowering house prices

The converse is true when energy and oil prices are very low. The economy normally starts to grow quickly, interest rates drop and house prices shoot up.

Boost to GDP: The oil price crash from $110/bbl to $52/bbl is having the predictable impact of creating deflation - that is causing Central Banks all around the world to drive down interest rates even lower to try and boost inflation. But all the cheap money normally streams into property and the stock market we start to get property bubbles and stock market bubbles.

UK: We really need to expect to see UK house prices shooting up further as long as a Tory Coalition is formed in May as floods of cheap money, low mortgage costs and a housing shortage stimulate demand for people to purchase property in a very tight market particularly in London and southern England.

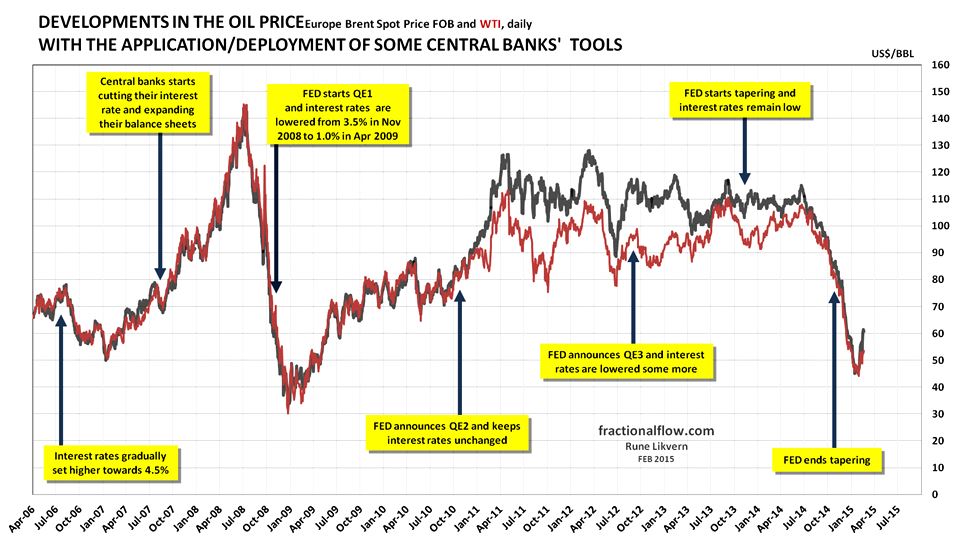

Record Low Interest Rates: So what is the underlying cause of the record low interest rates for such a long period? In our view there are two items working to drive inflation lower:

1. Migration Workers: Because of lax border controls and free moment within the EU - huge numbers of unskilled and skilled workers have flood  into the UK and this has created more competition in the jobs market, meaning workers cannot demand higher wages in service related jobs. If someone leave, they are simply replaced by another person coming in. If a worker underperforms, they are replaced immediately. This has been triggered by globalisation of the jobs market and European open borders where workers from all around the world come to London seeking opportunities. This then pushes up housing demand for both purchased and rental property, whilst keeping a lid on underlying inflation and keeping borrowing costs to a minimum. Rents rise as more workers arrive, and returns rise with it. Super-rich "Non-Doms" totally about 130,000 - mostly foreigners - have moved to the UK - mainly London - to invest and manage their global businesses. This has created huge numbers of service related jobs. For every "Non-Dom" there is probably about 10-20 people servicing their needs, and they may employ 10 to thousands in UK businesses they own or invest in. The point is - there are migrant workers of all types descending on the UK.

into the UK and this has created more competition in the jobs market, meaning workers cannot demand higher wages in service related jobs. If someone leave, they are simply replaced by another person coming in. If a worker underperforms, they are replaced immediately. This has been triggered by globalisation of the jobs market and European open borders where workers from all around the world come to London seeking opportunities. This then pushes up housing demand for both purchased and rental property, whilst keeping a lid on underlying inflation and keeping borrowing costs to a minimum. Rents rise as more workers arrive, and returns rise with it. Super-rich "Non-Doms" totally about 130,000 - mostly foreigners - have moved to the UK - mainly London - to invest and manage their global businesses. This has created huge numbers of service related jobs. For every "Non-Dom" there is probably about 10-20 people servicing their needs, and they may employ 10 to thousands in UK businesses they own or invest in. The point is - there are migrant workers of all types descending on the UK.

2. Technology in the Energy Sector: Just as Peak Oil seemed to be on us in 2005 when Peak Conventional Crude Oil hit two things happened in sequence, both in the innovative fast moving USA. Firstly, natural gas prices started rising in 2005 from about $4/mmbtu up to £12.5/mmbtu by end 2007 and with it, US oil companies started drilling long horizontal wells in shale gas deposits to seize this pricing market opportunity as gas supplies ran short. But these companies then flooded the market with gas and coincident with the US economic crisis and recession in 2008, gas prices crashed to $2.2/mmbtu. Rather than going bankrupt, these same energy companies realised that this technique of d rilling long horizontal wells and placing multiple hydraulic fracs into the shale also gave fairly good quantities of very light oil and condensate they discovered some areas that were particularly oil rich so called sweat spots. The problem in mid 2008 was that oil also crashed to $45/bbl so there was a short period that it did not make economic sense to drill either oil or gas wells, but by mid 2009 oil prices had recovered to $70/bbl and these shale drilling rapidly innovated and switched to drilling shale oil in North Dakota and West Texas. Word got around quickly and the boom was on from mid 2009 to end 2014 about 4.5 million bbl/day of US oil production was added a phenomenal amount, as oil prices rose from $40/bbl end 2008 to $110/bbl by 2010 and stayed close to that level for about 4 years. Every rig that could be sourced went to drill approx. 3 km long horizontal drains at a vertical depth of 2.5 3.5 km and many of these wells now had 15-30 fracs placed in each of them to boost production rates and oil recovery. Wells were drilled in a spider and other patterns with sometimes 12 wells from each surface location each with 15-30 fracs. It was a massive boom.

rilling long horizontal wells and placing multiple hydraulic fracs into the shale also gave fairly good quantities of very light oil and condensate they discovered some areas that were particularly oil rich so called sweat spots. The problem in mid 2008 was that oil also crashed to $45/bbl so there was a short period that it did not make economic sense to drill either oil or gas wells, but by mid 2009 oil prices had recovered to $70/bbl and these shale drilling rapidly innovated and switched to drilling shale oil in North Dakota and West Texas. Word got around quickly and the boom was on from mid 2009 to end 2014 about 4.5 million bbl/day of US oil production was added a phenomenal amount, as oil prices rose from $40/bbl end 2008 to $110/bbl by 2010 and stayed close to that level for about 4 years. Every rig that could be sourced went to drill approx. 3 km long horizontal drains at a vertical depth of 2.5 3.5 km and many of these wells now had 15-30 fracs placed in each of them to boost production rates and oil recovery. Wells were drilled in a spider and other patterns with sometimes 12 wells from each surface location each with 15-30 fracs. It was a massive boom.

US Rig Slowdown: The US production continues to skyrocket even as the rig count crashes partly because less drilling rigs are required to complete already drilled wells. Since the horizontal wells have already been drilled the batch completion process of pumping multiple fracs in multiple wells on a single well pad may take 6 months before the whole cluster of wells is put on-stream. We are now almost nine months from when the oil price started to drop sharply and 5 months since it reached a low of ~$48/bbl so we expect US production to start levelling off mid April.

Security: Beyond any doubt, the problems in the Middle East are escalating. As the oil price has crashed, the government have been less able to make large social payments to keep their citizens appeased. A hugely increasing young population is becoming more and more restless with higher unemployment with the youth often manipulation from extremist groups, sometime through the internet. The poorer desert areas are being overrun by extremist groups and militias. Saudi Arabia is being surrounded autonomous groups of militia from different sects. There are ongoing and escalating conflicts between the Sunni and Shia populations. The Sunnis are supported by Saudi Arabia and Shia by Iran. Over time the more stable autocratic family run regimes have broken down starting in the so called Arab Spring - this has developed unstable democracies and autocracies with collapsing governments, law and order and given opportunities for extremist groups to prosper. Libya is a classic example. For property investors, if these security issues in North Africa and the Middle East subside and the US oil production continues to increase one can expect oil prices to stay low at around $50/bbl. However, if the security issues increase whilst the US production levels off and/or drops - particularly if there is a threat to Saud oil fields, then expect oil prices to rise sharply to $100/bbl as shortages occur and speculators bet on prices rising. For property investors, low oil prices are of course highly preferable because borrowing costs and inflation stay low, whilst property price inflation and hence asset values normally rise.

LNG Technology and Economies of Scale: Another technology that was developed in the 1970s that continues to benefit low energy prices is LNG (Liquid Natural Gas). This allows shipment of vast quantities of super-cooled gas to markets around the world and keeps a lid on global gas pric es. Economies of scale - particularly with projects in Qatar - mean the market is more competitive and gas prices lower because of this additional supply. the LNG plants get larger and unit processing costs decline with it. Shale gas in the US has also helped - and the start of LNG exports from the USA. This all helps keep inflation low and boosts GDP growth - higher disposable income, and boosting manufacturing. Wealth increases, as do living standards. It also prevents pipeline gas exporters from raising prices too high, since LNG can be imported to all coastal areas (note 80% of the world's population lives within 200 miles of the coast).

es. Economies of scale - particularly with projects in Qatar - mean the market is more competitive and gas prices lower because of this additional supply. the LNG plants get larger and unit processing costs decline with it. Shale gas in the US has also helped - and the start of LNG exports from the USA. This all helps keep inflation low and boosts GDP growth - higher disposable income, and boosting manufacturing. Wealth increases, as do living standards. It also prevents pipeline gas exporters from raising prices too high, since LNG can be imported to all coastal areas (note 80% of the world's population lives within 200 miles of the coast).

Oil Supply Demand Balance: The new US oil then flooded the market, and despite production outages caused by ISIS, poor security in Syria, Iraq, Libya, Nigeria and Yemen, the 4.5 mlllion bbls/day of additional oil was enough to drive oil prices from $110/bbl to $52/bbl because Saudi and OPEC did not want to cut back their oil production. It's estimated that major security issues have cut global production by about 3.8 million bbls/day though US production has added an additional 4.5 million bbls/day since 2008. Western developed economies are using less oil per capita whilst eastern developing economies are using more - both roughly balancing themselves out - with a slight increase of 1% a year in oil demand. Global oil production is still growing, however, demand is barely increasing and hence an oversupply of may be 1.5 million bbls/day that is creating an "overhang" that started mid 2014. The markets have then seized on this and this downbeat view has driven prices from $110/bbl to $52/bbl, also in large part because Saudi shows no intension of reducing their production.

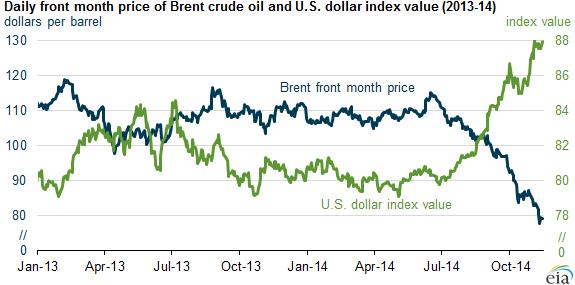

Fiat Currency Printing: Another important thing to consider is the correlation of the oil price with the US dollar. In general:

-

when the dollar declines, oil prices rise

-

when the Fed prints dollars, oil prices rise

-

when interest rates rise and the dollar rises, oil prices drop

Switch in Printing: At this time, the Fed has stopped printing currency, interest rates look like they could start rising (this is the market perception anyway) and the dollar has been rising in value against other currencies in part because of the expanding US economy, off the back of the shale oil boom and lower oil prices, and also because European Central Banks and Japan are printing gigantic quantities of their currency. All these we believe are very important factors that are driving oil prices in dollar terms lower. All but a few commentators on oil markets have not considered this. In the extreme, one could argue the drop in the oil price is almost entirely related to the switching of currency printing from the USA to Japan and Europe - meaning investors/speculators prefer to buy the dollar since inflation looks benign in the USA - tipping oil prices in dollar terms down globally. In any case, the low oil prices should create a big economic boost for most developed nations and this should start to feed through to higher house prices in the next few years.

Gold is Money - Currency is not Money: You might note we refer to "fiat currency printing" rather than "money printing". All western currencies are fiat - e.g. Central Banks print more into circulation. The only "real" money is gold - which cannot be printed (only mined to a limited extent at vast cost and engineering-environmental resources). Gold is valued at $1200/ounce - but costs close to that to mine. We still maintain that one day, since debts are so vast, there will become a tipping point where debts in the UK, Japan, China and USA will become so enormous the only way to pay them back will be to print like crazy at which time gold prices will go ballistic from their current levels. Whether this is in 6 months or 6 years, we really don't know, but it will happen eventually.

Property Price Set to Rise Further: So what does this mean for the property investor? Well for all those who have property in western developed nations, its rather good news because it now seems that are plentiful oil supplies in the USA at prices over about $70/bbl. So the days of >$110/bbl oil seem to be over at least for the next year or so, as long as a massive regional war does not break out. This should boost economies reliant on oil imports like the UK, France, Germany, South Korea, Holland, Spain, Italy, the USA and Greece. It should stimulate tourism, spending and GDP growth particularly as interest rates will be drive down and central banks will need to print currency (mainly through bond purchase schemes) that will then find ultra-cheap cash that people will then put into property. This should then drive property prices higher. The bottom line is, in almost all areas in the USA (except North Dakota and Texas), UK (except Aberdeen), France and other oil importin g nations these low oil prices driven by technology developments in the energy sector will boost property prices.

g nations these low oil prices driven by technology developments in the energy sector will boost property prices.

Election: For UK property investors, if the Tories form a new government - our guidance is immediately to "put the foot down" on the accelerator of property investment by mid May. One strategy is to search and make an offer before the Election result then exchange and complete after it becomes clear - this is a way to risk mitigate against a possible Labour-SNP Coalition that would have major negative repercussions for property investors and house prices alike on both sides of the border. Property investor should hope that the current economic plans are maintained by a government that can effectively manage the economy and has the confidence of financial markets and businesses in London - that the Tories and Lib Dems in their Coalition certainly seem to have. Credit to Nick Clegg for helping keep the Coalition on the road to economic recovery and allowing the redressing of the disastrous period of spending and debt increases inherited from the last Labour government only 5 years ago.

Summary: When the US government prints currency, the dollar declines, oil prices rise and house price and GDP growth is subdued as energy/food/consumer inflation rises and disposable incomes drops. The dollar has strengthened in large part because of plentiful oil and gas production in the USA - a boom - since the financial crash in 2008. Because of this new oil and strong dollar, oil prices have collapsed and this is now boosting GDP growth in Europe and keeping borrowing costs very low - which then in turn boosts property prices. We expect this to continue in Western Europe through 2015 and in the UK but only if the Tory's form the new government.

We hope this Special Report has given you some pointers as to why economies grow strongly, then contract and the impact on property prices of oil prices. If you have any queries, please contact us on enquiries@propertyinvesting.net