701 : UK Financial Crisis - Successive Mistakes Will Lead to House Price Crash - After Inflation and Rocketting Energy Prices

10-02-2022

PropertyInvesting.net team![]()

Beginning of Crisis: We are just at the beginning of a financial crisis in the UK. The chaos of the end September mini-budget tax cuts and Sterling tanking is just the beginning regrettably. Successive governments have printed huge quantities of the Pound Sterling to stimulate the economy over and above the basic GDP and productivity the UK has delivered, whilst exports and productivity have declined. The problems go way back to the 1980s.

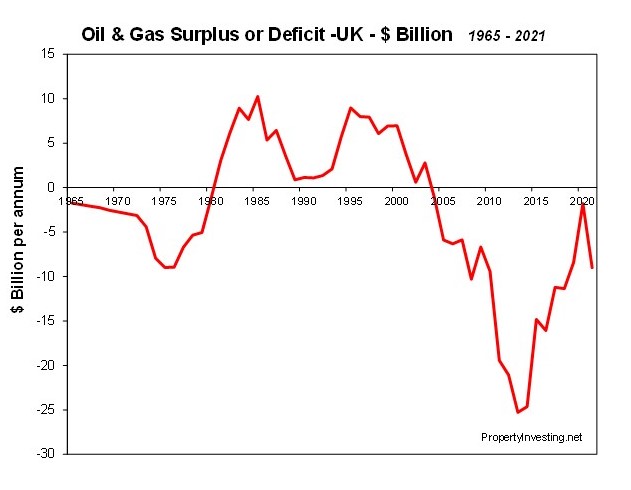

Historic Backdrop: US President Regan and the Fed Chairman Volkhert in the early 1980s wanted to kill off inflation, so they jacked interest rates up to 15% - as did the UK in tandem. This had the desired affect but it also closed down large swathes of old heavy industries in the UK. We became a more service oriented economy with the London financial sector driving growth. But at the time we had a huge benefit in that in the late 1970s we found huge amounts of oil and gas in the North Sea and rapidly became a net exporter or oil and gas with production far outstripping production. Over the years these royalties and taxes were largely squandered through public sector spending. We kept having large budget deficits. At the time the Pound was at least backed by oil and gas the Petro Pound some called it. Below you can see the combined oil and gas surplus-deficit in US dollars over the years - with bug surpluses from 1980 to 2004 then large deficits onwards - this does not include the huge deficit in 2022 caused by high oil prices and skyrocketing gas prices.

London Dominance Waning: Londons dominance in the financial markets increased through to 2015 at which time we were the number one financial centre in the world. We had escaped the financial crisis of 2008-2010 largely unscathed avoided the Euro-crisis woes - because we were able to print large amounts of money whilst Pound Sterling value remained high because of our historical reputation and strong governments, whether these were Centre-Left Blairite or the Cameron Centre-Right governments. On the whole the UK Chancellors seemed to have good economic advisers there was mis-management but the UK always go away with it. Trust was high in the governments and Parliament was a well respected institution. Again the Pounds was backed by oil, gas, the UK miliary and our global influence.

UK Peak 2015: London and the UK seemed to reach a peak in 2015 just before the Referendum. Growth and productivity were strong. Our trading with the Eurozone was robust. We had loads of mainland Europeans contributing to the UK economy London was booming financially and unemployment was low, with high paid company/corporate jobs were in good supply. Cameron had a small Tory majority and the government seemed to be working well with the public sector in delivering services and prosperity to the UK citizens. Around half of this growth was caused by a population boom as more people moved to the Uk to work mainly from mainland Europe.

Referendum: Then it all went horribly wrong, the self-induced damage from the Referendum. The Referendum was only advisory, and the critical mistake in our view is that firstly David Cameron chose to resign then Teressa May said Brexit means Brexit which cemented the Referendum as being a fait-de-complete. We then had years of wrangling and damage caused by Jeremy Corbyn destabilising the economy by causing mayhem and uncertainty in Parliament. Then we had Boris Johnson who at one point - just before the last General Election - was isolated almost a one man band who toured the red wall of the north in a Battle Bus saying we had an oven ready Brexit deal on the table. It was the best for Britain. It surprised everyone how successful he was at getting a huge Tory majority. At least we now had a strong government and would get Brexit done although most of the population thought it would do economic damage.

COVID Money Printing: Then COVID struck the government struggled to cope and more self-induced harm was done with non-compliant gatherings/parties, Cummings trip to Durham, accusations of corruption or low standards. The media spent far too much time complaining about a few drinks parties meanwhile the economy was tanking, inflation was raging and Brexit was not getting done and Putin was moving his forces to threaten Ukraine even early Feb 2022 the main news was about Boriss parties it was crazy. The Bank of England printed huge amounts of currency to try and prop up the failing economy. Record low interest rates and money printing stimulated a housing boom despite the economy tanking. How can we have the economy stopping whilst house prices boom you might quite rightly ponder. If you double the money supply, give everyone money for staying at home, then say it does not cost anything to borrow despite the economy being broken, you will see massive demand for property whilst very little supply is coming onto the market through shutdowns prices will rise.

Energy Mess - Woke ESG: On the energy scene - from March 2020 to March 2022 firstly we had this Woke view that once COVID had hit, oil prices tanked from $80/bbl to $20/bbl and gas prices crash, we could all do without hydrocarbons no to fossil fuels. We would replace them with solar and wind, close down our nuclear power plants and ban coal burning. After all there would be less business travel people would tele-conference and everything would be fine and dandy its what we need to fight climate change and this was the top priority. Oil and gas companies and anyone working for them were ostracized. Banks and companies fast-tracked ESG mandates/rules, stopped investments in fossil fuels and cancelled development permits offshore in the North Sea (e.g. Cambo). This culminated in COP26 Oct 2021 when the UK pledged to transition rapidly away from oil and gas we did not need these dirty industries anymore. We would get by with wind and solar.

Russia and Gas: In early Feb 2022 Germany refused to sanction the start of Nordstream 2 people giving a lame excuse that the HQ of the pipeline should be in Germany rather than Switzerland. We did not need Russias new gas pipeline. Then end Feb 2022 as if by concerted timing to catch the Woke ESG mad Europeans of their guard Russia invaded Ukraine and the European energy security was put in doubt. A mad scramble over the summer ensued to fill gas storage that led to an eight fold increase in spot gas prices. Roll back ten years and the Europeans were happy to link gas prices to a basket of crude oil prices but when these rose to $100/bbl, they broke contracts by demanding prices were set by spot market prices which were low at the time with plentiful gas from Russia and Norway. Roll on to 2022 and we are now paying the equivalent of $400/bbl for our gas prices another EU directive that spectacularly back-fired. Now Liz Truss has come out saying the ban of fracking in the UK has been lift as if this will help deliver even one additional molecule of gas in the next 10 years. Nice sound-bite what a rubbish wasted distraction. This flip-flopping of both UK and European energy policy had led to the 3-4 fold increase in energy costs that have fed massively into the inflation figures. Likely 3.5% of the 9% UK inflation is caused by this Woke ESG Energy Policy crisis mess which in large part is self-induced by years of relying on Russian gas at the detriment to our own energy security. To name but a few rubbish strategies:

- The EU switching to spot gas prices

- Germany shut down its nuclear power plants

- Prolonged maintenance shutdowns of French nuclear power plants summer 2022

- Relying on Russian gas rather than imports via LNG from friendly countries

- The UK shutting down its only gas storage facility the Rough Field - 5 years ago

- The UK stopping the permitting of the new Cambo Oil Field development Oct 2021

- Germany refusing to start operations in Nordstream 2 in Feb 2022

- Many governments, banks and companies mandating ESG committees stopping the sanction of new projects during COVID and before CoP26

- Germany spending decades developing gas pipelines with the Russia to the detriment of their and other European countries energy security leading to massive inflation

- The Netherlands curtailing gas production in Groningen gas field in 2020 after some tremors and cracks in buildings appeared

UK Policy Mistakes: After massively overstimulating, the UK thought it could raise interest rates slower than the USA that has a massively more robust economy and is energy self-sufficient and our currency would stay nicely pegged to the dollar. This was naïve of the Bank of England. Then the Tory party ganged up against the person that has single handled won them power ousted their Prime Minister Johnson and Chancellor Sunik then replaced them with light weights Liz Truss and Kwasi Kwarteng both of whom in our view lack the necessary competence and experience. It seemed their was no coordination in the Bank of England raising rates by only 0.5% (whilst the US had raised their rates by 0.75% the day before) and the emergency mini-budget that gave away massive tax cuts to the top 5% that were unfunded.

Pound Start of Crisis: By Sept 28 2022 the UK financial markets tanked with Sterling dropping for 1.12 to a low of 1.03 to the dollar. It only recovered because the Bank of England re-started money printing (or quantitative easing as they call it) because they started buying UK Guilts because yields had skyrocketed from 4 to 5.5% and pension funds were getting into trouble with margin calls on debt based investments. UK pensions started to go down the pan.

Nordstream: Then to make matters worse Nordstream 1 and 2 pipelines were both bombed most likely by the Russians that have put these two gas pipelines out of action for months (if not years). A few days later the Norway to Poland pipeline began operations which interestingly crosses the Nordstream 1 and 2 lines in the same Swedish/Danish Baltic area. We only hope this new line wont be the next to be bombed also causing massive methane emissions, pollution and gas ignition danger. Just a few days later on 30 Sept, Germany unanimously voted against sending further weapons to help the Ukrainians post Russian annexation of SE Ukraine. It looks like Putins tactics worked end Sept the combined bombing of Nordstream likely a distraction tactic whilst he did a sham Donbas Referendum then annexation and hell likely declare victory in October. Meanwhile the Germans sit there looking stupid.

Financial Contagion: But this is just the beginning. What a mess. On the one had the Bank of England is aggressively raising rates and on the other hand they are monetary easing by buying Guilts from thin air. Propping up the Guilt market because international investor dont want to buy UK Guilts because prices are dropping and yields are going up. The UK Bond market is at a precipice.

Two fifths of all mortgages were pulled end Sept so borrowing will become far more difficult along with drastically higher rates. In our view it is almost certain now that a major house price correction or even crash starts late September. We rolled over in September and now it will be heading down and the only question in our view is how quickly and severely and when will it end.

The shear arrogance and/or incompetence of the government from an economic standpoint needs to be highlighted along with the Bank of England that should be ashamed of themselves for printing so much Sterling then being way behind the curve on interest rate rises despite massive self induced inflation. In early 2022 we had interest rates at 0.25% and inflation rising to 7-8% - a gigantic 7% behind the curve despite a growing economy that was well past the COVID. Interest rates are normally set at above inflation to allow savers to get a return, not 7% below!

Very few people particularly those with assets wants to see a house price crash. But that looks odds on what we will now get because of the Bank of England and government incompetence.

Accelerating Pace of Crisis and Change: Everything is accelerating the pace of financial crisis and change is dramatically increasing and something big is going to break we believe in October 2022. This could be one or more of a number of things:

- Full scale UK bond market crash currency crash - yields and rates going ballistic - causing economic melt-down and close to hyperinflation in the UK (or Bank of England keep rates too low also causing very high inflation)

- Russian attacks on other European infrastructure -for example subsea fibre-optic cables, oil pipelines, gas pipelines - using drones, submarines to sow the seeds of doubt and confusion

- Russia invades somewhere else

- Russian possible use of tactical nuclear weapons further escalation

- European energy crisis worsens with blackouts and gas curtailment in certain countries

- China uses the confusion/chaos to invade Taiwan (unlikely but possible

For the UK investors its difficult to know what to do for investments at this time. We expect all asset prices to drop at least for the next 6 months.

- Stocks likely to tank by another 30% or more

- UK Bonds likely to tank further with yields rising

- Sterling likely to tank further

- House prices likely to crash

Labour: In addition now firmly on the horizon for May 2024 is a Labour government. They are likely to spend more, devalue Sterling even further and cause interest rates to rise further. We believe the currency markets are front running this outlook they know the chance of the supposedly fiscally prudent Tories getting back into power in May 2024 is remote now, so they are dumping their Sterling in anticipation who can blame them? It looks like the 1970s all over again. Before we found North Sea oil that saved us. Though this time, one cannot see anything that will save the UK.

For UK investors, the only ray of hope is to:

- Put cash into gold that is priced in dollars and should at least keep close to the dollar in price with an upside of rising far higher in dollar terms as financial contagion continue

- Buy US 20 year Treasuries these have dropped 50% in the last year but should rise back again as inflation in the USA drops and the inflation exported all around the world by the high dollar causes crises in weaker economies (e.g. Italy, UK, Greece, South America, South Asia).

- Invest in oil and gas companies as long as oil/gas prices stay high even during a global recession (risky)

- Buy Bitcoin priced in dollars currently $19,200 per coin - downside is likely around $12,000, upside in a 5 year timeframe is ~$100,000 per coin. For a riskier alt coin - buy Solana current price $33/coin, downside to $20/coin upside in a 5 year time frame is $500/coin. So for non US investors, as your currency likely declines further against the dollar even if the price does not rise, you might gain in dollar terms.

The UK investors its best to avoid UK property until after the likely price crash albeit it may never return to high prices because of a post May 2024 Labour government with rent price caps, licencing and further draconian tax increases and regulations, Labour will target property owners and landlords for new taxes - fines and penalties. Regret this special report contains very little good news or hope.

The advice to people blow retirement age - keep your job - and try a "side gig" business or investments on the side, that generates income. Avoid taking on debt. And watch out as the economy worsen - then Labour get into power May 2024.