229: Property Investor UK/US update

10-09-2008

PropertyInvesting.net team

1. That Oil Price Weve Been Warning You About

In June 2007 when oil prices were $70/bbl we predicted that by end 2008 oil prices would reach $125/bbl. By April 2008 oil prices had overshot this projection and hit $147/bbl. In our view, this has done severe damage to the global economy the $1 Trillion annual oil import bill of the USA has starved the country of much needed capital. We believe it is no coincidence the length and severity of the credit crunch has correlated with record high oil prices.

And the credit crunch has been most marked in major oil importing nations. Some difficulties were encountered in August 2007 immediately after oil price starting taking off from $70/bbl to $90/bbl. They have culminated in US and UK banks going broke mid 2008 as oil prices sky-rocketted. Problems have been so severe that oil prices have now shot back down to $93/bbl as overall demand increases have been curtailed as many global economies have started to sink into recession.

And the credit crunch has been most marked in major oil importing nations. Some difficulties were encountered in August 2007 immediately after oil price starting taking off from $70/bbl to $90/bbl. They have culminated in US and UK banks going broke mid 2008 as oil prices sky-rocketted. Problems have been so severe that oil prices have now shot back down to $93/bbl as overall demand increases have been curtailed as many global economies have started to sink into recession.

Shades of 1971 and 1981 all over again. The lower oil prices will help revitalize these oil importing economies but its probably too little and too late the damage has been done. Its only surprising that inflation did not rise above 5% in the USA and UK as oil prices rose from $10/bbl in 1999 to $147/bbl by April 2008. Now expect inflation to come back down to reasonable levels as long as oil prices stay at or below $100/bbl. There is even a small threat of deflation as all asset and commodities prices have dropped significantly to mitigate the risk of incurring deflation, government would drastically drop interest rates to close to zero whilst pumping new money into the economy in the form of tax breaks and other spending incentives. To refer to our Special Reports on oil prices and the opportunities and threats they provide, please click on the links below:

191: Oil Price Update and Real Estate

187: Real Estate and the commodities super-cycle

186: Oil price starts to skyrocket as predicted - how to profit

180: Oil prices continue to skyrocket

172: Make serious money - best investment sectors

169: Oil supply crunch begins

protect yourself

168: Alarm bells ringing oil price shock now on the horizon

163: Making Serious Money as asset prices plateau resources and property

161: Resources winners and losers - ranked list for property investors

160: Find out the winners and losers in the biggest oil boom in history - about to happen...

159: Massive oil boom - the winners and losers - be prepared

158: Supply and demand scenarios - oil boom and the property investors insights

157: Impact of "Peak Oil" for Property Investment

151: Oil price $125 / bbl and rising

how to take advantage in property

150: Peak Oil shortly due to be reach unique insights for a property investor

148: Take advantage of the oil/gas/coal boom key insights

2 Self Regulating Market Forces

What the oil exporting nations have now learnt is that oil prices at $147/bbl causes recession in their major customers economies USA, Germany, France, Italy, Spain to mention a few. Furthermore these same countries are now developing alternatives to oil such as electric powered cars, solar, wind and other renewable sources. Its now most likely oil prices will stay in the $90-$125/bbl range until the global economy is back on its feet then expect oil prices to again rise above the $125/bbl level as increasing demand from China, Middle  East and India outstrips increases in supply whether this happens by mid 2009 or far later, in say 2011, is difficult to estimate all depends on how the global economy gets itself out of the banking crisis its current in. Note there are no Middle Eastern, India, Russian or Chinese banks going under - the Middle Eastern banks are flush with cash from high oil prices. Sovereign Wealth Funds will start buying cheap US and European assets soon, which should at least help shore up the economies. Indian and Chinese economies are still motoring along (10% and 8% GDP respectively) off the back of a massive boom in services and manufacturing industrial growth respectively. We would expect this to continue having human capital of 2 billion people will keep costs down, competitiveness up and help pay for high oil prices. Western economies will continue to suffer from high oil prices this will subdue real estate price growth.

East and India outstrips increases in supply whether this happens by mid 2009 or far later, in say 2011, is difficult to estimate all depends on how the global economy gets itself out of the banking crisis its current in. Note there are no Middle Eastern, India, Russian or Chinese banks going under - the Middle Eastern banks are flush with cash from high oil prices. Sovereign Wealth Funds will start buying cheap US and European assets soon, which should at least help shore up the economies. Indian and Chinese economies are still motoring along (10% and 8% GDP respectively) off the back of a massive boom in services and manufacturing industrial growth respectively. We would expect this to continue having human capital of 2 billion people will keep costs down, competitiveness up and help pay for high oil prices. Western economies will continue to suffer from high oil prices this will subdue real estate price growth.

The only key exceptions are Norway and Canada both western oil exporting nations. The UK still hardly imports oil/gas, so it will be okay for a few years before the oil/gas decline further. Russia, producing 9 million barrels a day and supplying 30% of the European gas demand will also continue to prosper these economies should survive the current credit/banking crisis relatively unscathed. In theory, the UK should not do too badly either, but well refer judgment on that until we see how the current leadership handle the problems in the next few months. In summary, the market has called that oil is too high as this has led to a recession and banking crisis. If oil prices stay at the current level of ca. $100/bbl enough to keep Iran/Venezuela happy but not lead to a global recession, then its quite possible the US and UK economies will come out of a mild recession by mid 2009 and with it property prices should start rising again. If oil prices rise above $140/bbl again all bets are off! Expect a severe recession in the USA and UK plus further severe house price declines.

3. What do we look forward to?

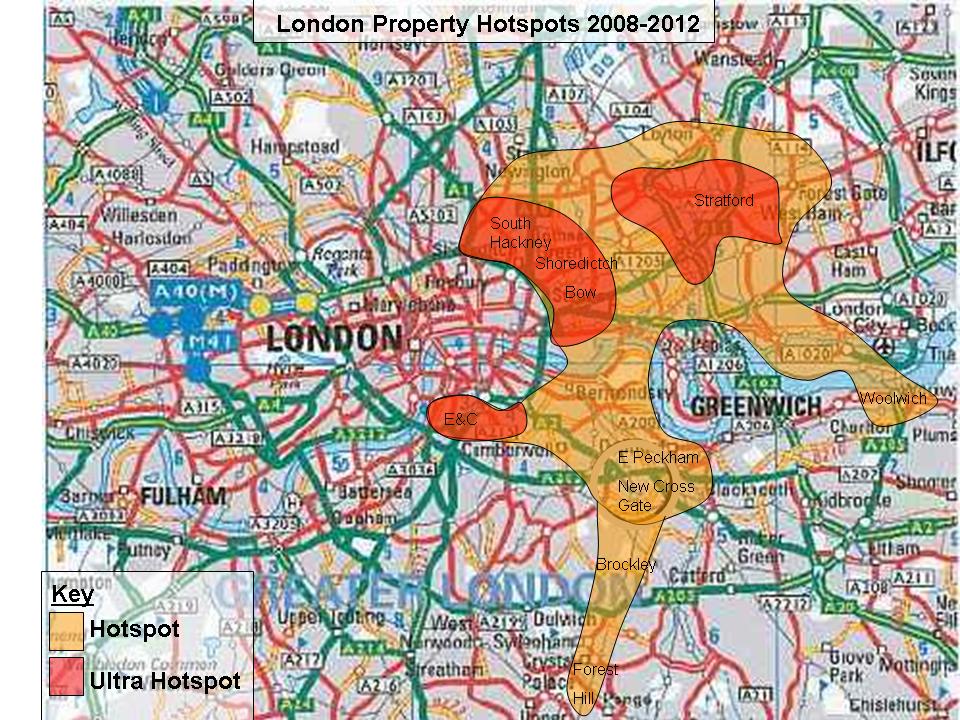

The current severe slowdown in the UK property market and the economy likely slipping into a recession is not good news. Where is the silver lining? We expect property prices to stablise in London and Southern England by mid 2009. This will be only three years before the London 2012 Olympics. Indeed this is very exciting to visualize investing in property on the low of the market say mid 2009 or earlier, then seeing prices rise as the Olympics get closer and major infra-structure projects are finished. This month we prepared a London hotspot map for the period 2008 to 2012. This is a summation of all our analysis on new infra-structure projects underway and planned.

The overlapping spheres of influence e.g. geographical proximity to the respective infra-structure improvements and regeneration, plus our knowledge of the local business-jobs environment has resulted in this map that you can use. There are a few areas it is profoundly difficult to envisage that in a 4 year time frame property prices will not rise examples:

· Stratford Olympics venue, massive retail development, new Eurostar station, Olympic village, parks etc - our favoured small investment area is about ½ mile SE of the centre locally know as Stratford Village two story Victorian houses and flats in quiet streets just north of Ham Park

· Hoxton-Haggerston on the fringes of the once severely distressed Hackney area in 2010 the new East London Rail Line will be finished along with a new station built at Haggerston this once marooned area with poor rail or no tube line will be opened up to the City of London wealthy jobs etc. Its also close to the Olympic venues at Stratford and not far from St Pancras terminal to Eurostar. Victorian property in quiet streets close to the new Haggerston station will see prices shoot up. Northern Hoxton is within walking distance to the City of London expect the ripple effect of this trendy artistic warehouse district to spread north towards Haggerston.

· Brockley the East London Rail Line opens 2010 and will connect Brockley for the first time to Whitechapel and the City of London, all the way to Highbury. Lovely Victorian property in this sleepy part of SE London will become far more desirable some lovely local parks and Telegraph Hill conservation area close by will see this suburbs fortunes transformed. New Cross, East Peckham, Nunhead, Forest Hill and areas west of Catford will also benefit.

· Nine Elms-Kennington-South Bank The American Embassy is moving to Nine Elms. This is on the South Bank close to the MI5 building at Vauxhall. This once depressed part of south London is being transformed no wonder why 0.5 miles from Chelsea, 0.5 miles from Westminster and some nice Victorian buildings. Excellent communication, South Bank arts are regeneration plus the London Eye have all helped. It takes 10 minutes by tube or bicycle to get to the City of London, Midtown and West End all equidistant. Expect prices to keep rising and ripple back further away from the Thames towards Elephant & Castle itself undergoing massive regeneration in the next three years. Its just so handy and central but also cheap prices are very likely to rise. The Olympics will also help. The only negative is that the Eurostar stops running to Waterloo but you can quickly get a rube to St Pancras, so it should not affect prices much.

Wed advise holding off until early to mid 2009, then straight into such areas. We also like Shoreditch, Bow, West Ham, Limehouse and Woolwich for similar reasons as outlined in our Special Reports.

Despite the banking crisis and credit crunch, we see the London economy outperforming other areas of the UK in terms of GDP growth in the next five years for the following reasons:

· Less reliant on public sector jobs - the Treasurys money has run out

· Less reliant on manufacturing jobs

· More reliant on financial services jobs downturn for a year then continued growth expected

· International centre for oil-commodities business

· Population growth of a further 800,000 people expected by 2015

· Building land is in short supply

· Olympics and infra-structure developments

· Airports and Eurostar transport expansions

· If London slips into a mild recession, the rest of the UK will be in severe recession

· Not enough properties being built especially this year

· International cosmopolitan centre for Middle Eastern, Far Eastern, African and American wealth management, property investment and tourism

4. Global Real Estate Problems Mount

Dont expect things to improve any time soon. The credit crunch started July 2007 and its now October 2008 with no sign of major improvement. The market crash on 6 October stocks down 6% in USA and 12-15% in Brazil and Russia have highlight just how precarious the global economy is at present. House prices continue to slide, inflation remains high and interest rates in Europe remain at 4.25% with 5% in the UK. UK house prices have dropped about 10% from their peak in mid 2007 (London -5%), with Irish house prices following a similar trend. US house prices have dropped by 10-15% from their peak, in some areas as much as 25%.

We expect things to deteriorate further until mid 2009, when we expect things will pick up again.

5. UK Update

In the UK interest rates fell Wednesday 8 Oct by 0.5% in an unprecedented global coordinated move the economy is now in crisis and a full recession is expected by year end. We now expect interest rates at 4.5% or below by year end the interest rates have been too high too long, and inflation will be considered a thing of the past by early 2009 as manufacturing, retail and also services economic sectors all sink into recession. The  Bank of England will be accused of acting too late in the economic cycle. The first rate reduction will probably be 9 October. The Treasurys lack of cash will not help since public spending will be tight and tax breaks non existent these will not help the economy. Gordon Browns leadership will remain under severe pressure and this will not help confidence in the UK economy. Expect the pound to slide. Oil prices dropping back will be broadly neutral since the Chancellor makes so much money from oil revenues in the North Sea (60% taxes) and at the petrol pumps (80% taxes). Remember, 90% of all oil revenue ends up with the Chancellor. We expect house prices in London and the SE to start rising mid 2009, with the rest of England lagging behind, possibly by a year. We do not currently recommend property purchase unless you spot a real bargain with high yields. Better wait until the bottom of the market is reached and our expectation, albeit this is very uncertain, is that this will be mid 2009 in southern England and later in the rest of the UK. Scotland will probably fair better than most other areas since property price rose very late in the cycle in this country. Aberdeen will continue to boom because of the high oil prices and North Sea and International oil activities.

Bank of England will be accused of acting too late in the economic cycle. The first rate reduction will probably be 9 October. The Treasurys lack of cash will not help since public spending will be tight and tax breaks non existent these will not help the economy. Gordon Browns leadership will remain under severe pressure and this will not help confidence in the UK economy. Expect the pound to slide. Oil prices dropping back will be broadly neutral since the Chancellor makes so much money from oil revenues in the North Sea (60% taxes) and at the petrol pumps (80% taxes). Remember, 90% of all oil revenue ends up with the Chancellor. We expect house prices in London and the SE to start rising mid 2009, with the rest of England lagging behind, possibly by a year. We do not currently recommend property purchase unless you spot a real bargain with high yields. Better wait until the bottom of the market is reached and our expectation, albeit this is very uncertain, is that this will be mid 2009 in southern England and later in the rest of the UK. Scotland will probably fair better than most other areas since property price rose very late in the cycle in this country. Aberdeen will continue to boom because of the high oil prices and North Sea and International oil activities.

We expect inflation to zoom down from its current high of 4.7% to about 2.5% by early 2009 as the drop in oil prices to ca. $95/bbl and the general global slowdown starts to take hold. This should give room for interest rates to drop as early as October 9th. Indeed, the threat of a severe recession is now so great, the Bank of England will need to drop rates, otherwise unemployment will rise significantly, GDP will drop like a stone and with it inflation. Its frankly time to act now, before its too late. UK rates were 5% until Oct 8th whilst US rates were 2.25% - a big gap considering the UK has similar problems to the US with regard to the credit crunch, banks going insolvent and property markets seizing up.

6. US Update

In the USA, the $700 billion Wall Street bail-out package has got support after political infighting and the blame game ended. This will put further negative pressure on the dollar, which will slide further. Because of this  further run on the dollar, oil price will probably rise to $100 to $125/bbl by year end. Interest rates dropped Oct 8th from their 2% rate (that was 3% lower than the UK earlier in the week). We believe real estate prices will stablise by year end and start increasing slightly from mid 2009 onwards as mortgage availability improves after the bloodbath in 2008.

further run on the dollar, oil price will probably rise to $100 to $125/bbl by year end. Interest rates dropped Oct 8th from their 2% rate (that was 3% lower than the UK earlier in the week). We believe real estate prices will stablise by year end and start increasing slightly from mid 2009 onwards as mortgage availability improves after the bloodbath in 2008.

To all those doubting Thomases the USA and New York will come back. Okay, the Wall Street crash of 10+% I a few days a fortnight ago and Congress rejecting the $700 Billion bail-out was not good news. Sounds distressing and depressing. The great thing about America though is the motivation of its people - Americans never give in. They have the following positive attributes that will always help lead to success - they:

- Are highly motivated

- Are hard working

- Are highly educated

- Are innovative creative ideas

- Are open-minded

- Have diverse people

- Have a private sector capitalist oriented society

- Have an increasing population

- Have good national security

- Have a politically stable democracy

This comment coming from non-Americans. To all those non-Americans - do not under-estimate the resolve, innovation and motivation of the American people. For this reason, long term, PropertyInvesting.net objectively believe property investment in the USA will be a good investment. New York is a special case. The current financial problems are severe, but they will not last forever. By 2010, things will have improved and the US economy will be growing steadily once more. A population growth of 2% per annum implies at least 2% GDP growth per annum.

The US economy is capable of being highly successful on its own. It's such a huge economy - its capable of keep itself propelling forwards at quite a momentum.

In future years, wealthy baby-booming US citizens will retire to southern warm or coastal regions such as:

- Florida

- California

- Arizona

- Carolina

- Nevada

- Colorado

- New Mexico

These will be the states with the largest population increase and likely house price increase. But New York will also see real estate price increases - the reason - financial services and international business.

The rich will get richer. They will seek the latest financial instruments, services and expertise - this is centralised in New York. Middle Eastern money will look to the USA for cheap and relatively secure assets dollar denominated. The gigantic transfer of wealth to oil producing nations like Russia, UAE and Saudi Arabia will make its way back to the USA - to New York into financial services and real estate. We predict the current market downturn will be temporary - conditions will improve mid 2009 and the next prolonged boom period or bull run will commence end 2009. How long this will last is difficult to say the problem is, when it finally ends, the baby-boomers will be retiring, pulling on their 502Fs legislation has been passed that makes it mandatory to sell certain pension fund shares in 2016 dont be in the stock market by then!

The rich will get richer. They will seek the latest financial instruments, services and expertise - this is centralised in New York. Middle Eastern money will look to the USA for cheap and relatively secure assets dollar denominated. The gigantic transfer of wealth to oil producing nations like Russia, UAE and Saudi Arabia will make its way back to the USA - to New York into financial services and real estate. We predict the current market downturn will be temporary - conditions will improve mid 2009 and the next prolonged boom period or bull run will commence end 2009. How long this will last is difficult to say the problem is, when it finally ends, the baby-boomers will be retiring, pulling on their 502Fs legislation has been passed that makes it mandatory to sell certain pension fund shares in 2016 dont be in the stock market by then!

Anyway, we hope the financial markets dropping 10% in the last few weeks have highlighted just how unsafe stocks are compared to property. Some people have lost all their savings through banks folding or companies going bust. At least with property, you have something tangible something useful and if the worst comes to the worst you might be forced to hand the keys over to the bank. And if youve only got 10% - 15% deposit, you loose this, not pleasant but its not the end of the world.

Anyway, hunker down, dont expect any big improvements for at least nine months and look forward to lower inflation, lower growth, less jobs, lower interest rates and suppressed asset price increases for a year or so. After this the bottom of the market with land shortages, building shortages, increasing populations and increasing trade with India, Middle East and China expect things to pick up end 2009. In London, the Olympics will then only be 2½ years away, so residential investment in East London looks particularly attractive in 2009.

7. Other Countries

For all those US and UK property investors that think things will be better in other countries, its quite possible they wont be. Just as an example, property prices have crashed 9.7% in Denmark in the last quarter. Iceland is suffering a massive run on its banks and currency over a sustained period of 12 months so far. Property prices are also dropping. Spanish prices are down a similar amount to the UK this is hardly surprising since so much Spanish property is purchased by Brits.

The Russian stock market has taken a big tumble so expect Russian prices become unstable they have boomed over the last eight years since the Russian banking crisis on the late 1990s. France and Italy have seen a severe property slowdown. German and Holland are stagnant, and prices in Norway have started dropping. In Latvia, prices dropped 20% from their highs in early 2007.

8. Comparison

Lets compare this to London London prices rose about 250% since 1997 to mid 2007 they have dropped 5% since mid 2007. Not too bad not yet anyway, although we dont yet know how City jobs losses will effect  the market towards late 2008. In the USA, prices are actually rising in Boston, parts of North Carolina, Dakota and parts of Texas. They have crashed by 20% in some parts of California and Florida, but in these areas, prices doubled in 5 years up to mid 2007. So overall, its not a pretty sight but for those UK investors who decided to go into property investment in 1997 instead of stocks and shares, the FT100 index is now lower than it was in 1997 whilst property has risen 240% - and if you have leverages your money, which were almost certain you will have done, your return on investment will have been amplified further. If your gearing is now 80%, you are exposed prices could drop by 20%. But of your gearing is more like 60% or 70%, its difficult to envisage prices dropping by 30 or 40% - its always possible but wed say its unlikely, particularly in places like London and southern England, or New York and Boston in the USA.

the market towards late 2008. In the USA, prices are actually rising in Boston, parts of North Carolina, Dakota and parts of Texas. They have crashed by 20% in some parts of California and Florida, but in these areas, prices doubled in 5 years up to mid 2007. So overall, its not a pretty sight but for those UK investors who decided to go into property investment in 1997 instead of stocks and shares, the FT100 index is now lower than it was in 1997 whilst property has risen 240% - and if you have leverages your money, which were almost certain you will have done, your return on investment will have been amplified further. If your gearing is now 80%, you are exposed prices could drop by 20%. But of your gearing is more like 60% or 70%, its difficult to envisage prices dropping by 30 or 40% - its always possible but wed say its unlikely, particularly in places like London and southern England, or New York and Boston in the USA.

9. Cuba High Risk Watching Brief

For the very adventurous property investor, you should have a watching brief on Cuba. President Castro handed over ruling power to his brother earlier this year. US relationships remain very tense, but over the next 5-10 years, these are likely to ease. Havana and Cuba are hugely under-developed. If conditions improve as sanctions are lifted and relationships with the USA improve, there could be massive inward investment from many different countries Europe, Middle East, Russia, America. Havana has a beautiful climate, beautiful architecture and scenic surroundings. Friendly people. The crumbling Hispanic buildings along the Havana waterfront-beaches has suffered 50 years of under-investment and lack of funds. Its worth keeping an eye on how things develop if we look at other countries that have opened up and see the massive capital value increases experienced, one can see that Cuba could also join these countries as barriers to entry fall, investment is encouraged and the country takes on a whole new business environment.

Some example of countries that have opened up in the past 20 years and have been transformed South Africa, Czech Republic, Dubai, Russia, Poland, Solvenia, Slovakia, Bulgaria, China, Croatia, Montenegro. The potential new entrants to this property investment world are Cuba, Libya, Lebanon, Iraq, Ukraine, Belarus, Algeria, Vietnam, Angola, Oman, Democratic Republic of Congo all countries that seen problems in the last 20 years where it is probable (though not for certain of course) that the business environment for property investment will improve.

back to top