257: Property investing, the UK economic situation and oil & gas

02-28-2009

PropertyInvesting.net team

PropertyInvesting.net team

How Bad Can Things Get?

No sign yet of the property market bottoming out. As long as the banks hoard cash and restrict lending to a minimum, property prices will likely slide further. Property prices are only worth what someone can borrow to pay for them. If there is absolutely zero borrowing possible for many years we have to consider how much cash we have in the bank then wed make an offer on a property. In such a doomsday scenario, instead of offering £150,000 for a  property you may only offer £30,000! Property is only worth what someone is willing to pay for it. If banks arent lending and no one has much cash, then you can imagine how little properties may be sold for, or worth. All very gloomy.

property you may only offer £30,000! Property is only worth what someone is willing to pay for it. If banks arent lending and no one has much cash, then you can imagine how little properties may be sold for, or worth. All very gloomy.

The banks are still suffering big losses, and governments are continuing to bail them out and nationalize the banks. This shows no immediate signs of slowing. As governments borrow more money to shore up the banks, their balance sheets deteriorate and their currencies devalue.

The

When To Call The Bottom?

At PropertyInvesting.net we dont see any reason to start purchasing additional investment property at this time we would prefer to see a clear bottom to the mark et. It does not look like there will be a rapid and pronounced turn-around. So for all cash rich property investors is there any big incentive for investing right now? Probably not. Wed wait a while longer - bigger bargains are likely to develop. Unemployment will rise further. There are likely to be more distressed sellers. Some large property funds will also be unwinding their over-leveraged positions. The earliest we can see a possible turnaround is late summer, or later. Unless you can pick out a spectacular bargain, why would an investor want to purchase now if they expect prices to drop a further 10%? In such an environment an investor has to be even more disciplined that in good times you are not a social charity. You have to look after your own bottom line, cashflow and business viability make sure you do not risk damaging your own bottom line to help someone you meet during a property purchase transaction that may need the deal more than you do. Always be willing to walk and feel comfortable with this. We are now into unchartered territory and no-one frankly knows whats around the corner. So be careful when you purchase in the current environment and as a rule, try and purchase property that is at least 20% below current benchmarked market value. This will protect your downside somewhat, and in the event of an upturn, will make your handsome returns IF things improve.

et. It does not look like there will be a rapid and pronounced turn-around. So for all cash rich property investors is there any big incentive for investing right now? Probably not. Wed wait a while longer - bigger bargains are likely to develop. Unemployment will rise further. There are likely to be more distressed sellers. Some large property funds will also be unwinding their over-leveraged positions. The earliest we can see a possible turnaround is late summer, or later. Unless you can pick out a spectacular bargain, why would an investor want to purchase now if they expect prices to drop a further 10%? In such an environment an investor has to be even more disciplined that in good times you are not a social charity. You have to look after your own bottom line, cashflow and business viability make sure you do not risk damaging your own bottom line to help someone you meet during a property purchase transaction that may need the deal more than you do. Always be willing to walk and feel comfortable with this. We are now into unchartered territory and no-one frankly knows whats around the corner. So be careful when you purchase in the current environment and as a rule, try and purchase property that is at least 20% below current benchmarked market value. This will protect your downside somewhat, and in the event of an upturn, will make your handsome returns IF things improve.

Best Property Investment Areas: As a rule:

1. When an upturn finally comes, the most likely place in the UK this will start is

-

regenerating areas

-

where new jobs are being created

-

where new infra-structure developments are taking place

-

where positive change is occurring

-

where excellent communication and improvements in communication are taking place with more jobs, leisure facilities, retail and close to areas of wealth creation

-

areas of improving wealth, health, education, schools

-

areas with increasing population and either restrictions in home building, or big improvements in the quality of homes being built

If you look at all these criteria, and look at the overlapping spheres of influence of these criteria what comes out is that the following areas are highly likely will do particularly well in the

- Shoreditch-Whitchapel-Hoxton

- Limehouse

- Hackney-Wick

- Haggerston

- New Cross Gate (Telegraph Hill,

- Croydon

- Cricklewood (regeneration one)

- South Bank - Kennington

- Battersea (areas around the power station)

- South Acton (as close to

Inflation

If the  could lead rapidly to inflation. The CPI inflation is unfortunately still running at 3% - well above the government target of 2% despite the recession and oil prices crashing from $147/bbl to $40/bbl. Okay, RPI is dropping like a stone to close to zero because retailers are in distress and are off-loading stock and trying to retain volumes at the expense of margins. Consumer demand has probably kept up a bit better than most people thought they would but many shops are closing. A big retail shake-out is occurring. Commercial property prices have crashed particularly in peripheral retail areas many vacant shops now litter the high streets. Overall, we believe there will be:

could lead rapidly to inflation. The CPI inflation is unfortunately still running at 3% - well above the government target of 2% despite the recession and oil prices crashing from $147/bbl to $40/bbl. Okay, RPI is dropping like a stone to close to zero because retailers are in distress and are off-loading stock and trying to retain volumes at the expense of margins. Consumer demand has probably kept up a bit better than most people thought they would but many shops are closing. A big retail shake-out is occurring. Commercial property prices have crashed particularly in peripheral retail areas many vacant shops now litter the high streets. Overall, we believe there will be:

1 Continues downward pressure on

2 RPI inflation dropping to ca. -2% by year end

3 CPI inflation dropping to ca. +1% by year end

4 Unemployment continuing to rise

5 House prices as a whole dropping a further 10% in 2009

6 Early signs of a recovery by end 2009

7 UK GDP dropping -4.0% in 2009 (-2% in

To explain our prediction on UK GDP, we need to dig deeper into the current GDP numbers per sector to explain this. It's important for property investors - with key question, do you focus on areas hit hard by the recession (Birmingham) or areas least hard by the recession (London)? And - how come London will not be as hard hit at Birmingham?

In the last quarter, overall GDP dropped 1.5%. However, this masks some big differences per sector:

-

Manufacturing -7%

-

Services -1.5%

-

Property Letting +0.3% (still growing believe it or not)

-

Consumer spending -0.9%

-

Investment -5.9%

-

Exports -5%

-

Government spending +2% (the public sector again!)

As we have been advising since 2004, best to avoid areas exposed to manufacturing - and things are really starting to deteriorate sharply now. Manufacturing sectors most exposed are cars, metals and engineering. Those less exposed are petro-chemicals and oil/gas. The least exposed are utilities and food manufacturing. Meanwhile, financial services actually grew in Q4 2008 - all the stock market turbulence of course increased transactions and activity - mainly concentrated on London! When you look at the socio-economic fabric of the UK and the overlapping spheres of influence of these sectors - this would imply the following:

Areas most exposed to recession:

West Midlands - Birmingham

East Midlands - Nottingham-Derby

South Wales - industrial zone midway between Swansea and Cardiff

North East - Sunderland/Teeside

North West - Liverpool (peripheral industrial areas in Lancs)

Scotland - Glasgow

Areas least exposed to recession:

South East

South West (many public sector and services jobs - from London)

Scotland - Edinburgh and Aberdeen

Areas in the middle:

North West - Manchester

North - Leeds/Bradford/Humberside

Scotland - rest of (large proportion of public sector jobs should help Scotland for a while)

London could be hit hard if business travel, tourism, and business services are hit harder - and foreign money dries up, but there is not much sign of this as yet. London will also benefit from the massive construction efforts in Low Leas Valley in preparation for the Olympics in 2012 and associated rail/tube upgrades.

So despite the headlines - it could be insightful you to know that financial services and public sector are both growing still - whilst engineering/manufacturing is being hit very hard - when or if manufacturing will ever recover is open to question, since much of this activity will be transferred to lower cost areas abroad. If we had more Green Tech jobs (renewable energy jobs - tidal, solar, algael-biodiesel, wind, wave) it would help - we could put the UK's engineering excellence to work on good energy saving projects. But alas, the funding for such potential stellar growth projects seems to be lacking for both research and execution phases.

Capitalism Is Replaced By Social Models

One underlying problem little discussed in the mainstream media is that the policies being enacted currently by the  y performing business entities. To use tax payers money to bail out poor businesses is an extreme social policy a capitalist policy would be to let them fold, then a more efficient and well run entity would acquire them and add value rationalize and consolidate improve economic efficiency and returns. For the

y performing business entities. To use tax payers money to bail out poor businesses is an extreme social policy a capitalist policy would be to let them fold, then a more efficient and well run entity would acquire them and add value rationalize and consolidate improve economic efficiency and returns. For the

Where Has Private Enterprise Disappeared To?

Years ago, successful businessmen became politicians when they became financially free and looked forward to another challenge - to help steward the country and it's economy. They were businessmen turned politicians.

In 2009, the country is almost exclusively run by professional politicians that have never had any experience or training in business. They went straight from public school, to University then into the political arena. Most have a background in climbing the political career ladder many have not even worked within the civil service. The days of people like Michael Haseltine (a multi-millionaire book publisher businessman) moving into politics seem to be at an end. This is worrying because what it means is the decision makers nationalizing banks and controlling the economy have no key competencies to do so they have no skills in economics  or how business is run. What this means longer term is open to question. One notable exception is Vince Cable who worked most his life as an economist for Shell - and it is noticable!

or how business is run. What this means longer term is open to question. One notable exception is Vince Cable who worked most his life as an economist for Shell - and it is noticable!

However, what we have seen is a systematic massive taxation increase since 1997, massive public sector expansion, increases in red tape and regulation and increased deficits often at the expense of entrepreneurial enterprise and private business. Manufacturing has been in terminal decline it represents a mere 11% of the current GDP. Many school leavers see benefits in a safe pension in the public sector rather than the excitement, stimulation and risk of setting up their own business and investing we find this a real pity. Those graduates that move into the private sector prefer media and financial services to engineering, technology and disciplines to produce something material. Risk is almost a swear word. Business is blamed for the recession whilst the government spends hundreds of billions of pounds on public sector expansion programmes mainly salaries, pensions, consultant and often needless new public sector buildings.

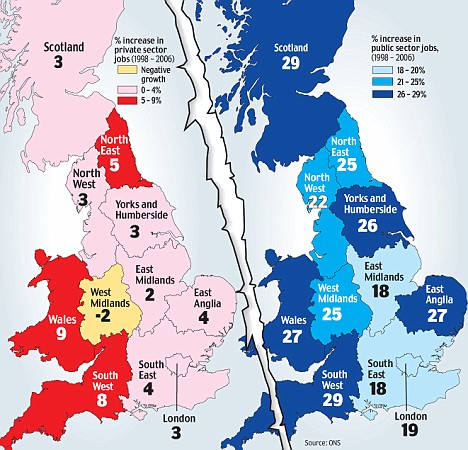

So why the public sector expansion? The cynics would say - a long held view - that public sector workers are far more likely to vote Labor - so to boost their numbers increases the chance of winning elections. Look at the chart above - Scotland now has 29% more public sector workers than in 1998 - but private sector jobs have only risen 3%! Who's paying for the public sector jobs? In the West Midlands - the wing territory - private sector jobs have declined by -2% whilst public sector jobs have risen by a massive 25% - extra-ordinary.

The incentives for school leavers are stacked in the wrong direction with regret and one of the last people it seems the government appears to be interested in helping is the buy-to-let private landlord. It often looks like any help is by accident think back to the SIPPs in 2005 and the U-turn the government made when it (and the media) realized it would actually significantly help property investors. Not all things are bad but overall, we see talk of helping banks, tenants, individual home owners with their mortgages - but never a word for the buy-to-let landlord who proceeds to get more heavily regulated by the day by the public sector that has just doubled in size in ten years with efficiency and productivity dropping and pension liabilities sky-rocketing.

For all those that expect to see a nice fat public sector pension in 10-15 years time, forget it were pretty sure the government will dilute this obligation either through ending inflation index linking, increase normal retirement age or reducing pension payments in general. Hence we believe that having a public sector job is actually a high risk option because when jobs losses occur and pensions are dropped or reduced it will be difficult for these employees to start over again. To those young people leaving School and University think carefully before joining the public sector theres no more money left to expand it and the skills you will pick up will not support finance independence. And put zero to the value of a pension in 35 years time therell be too many retired baby-boomers to pay for it, the youngsters of today will be last in line with no manufacturing left and massive energy challenges prices rise.

One of our specialities is the analysis of oil supply and demand and the impact this has on the economies of countries around the world. The good news is that the

One of our specialities is the analysis of oil supply and demand and the impact this has on the economies of countries around the world. The good news is that the

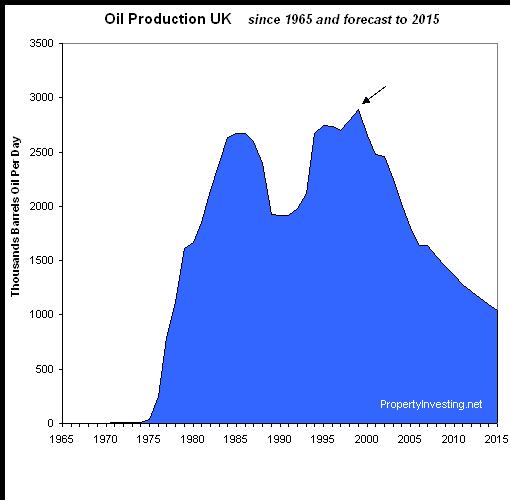

UK Oil Production - from 1965 to 2009 and forecast to 2015 - in severe decline

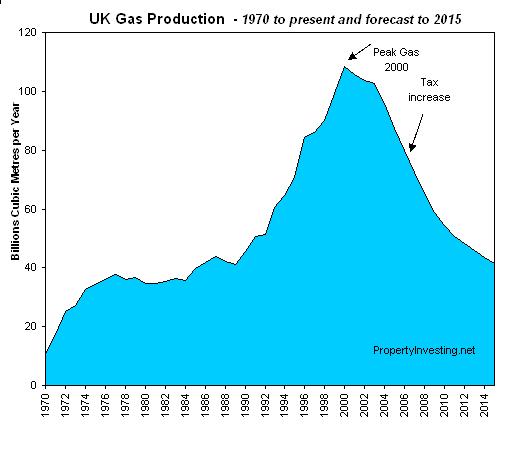

UK Gas Production - declining with "Peak Gas" year 2000 - from 1970 to present and forecast to 2015

Future of Energy

Oil, gas and energy provide the fuel for the global economy. Since oil prices crashed from $147 bbl in July 2008 to $40/bbl at present, oil investments have almost halved. Many projects have been cancelled or delayed particularly the Canadian Oil Sands developments. Oil exploration has declined. Drilling has  reduced and general production activity has waned. There is little incentive to boost production when much of this oil costs $20 to $40/bbl a barrel to extract after taxes. Meanwhile OPEC have cut production by a massive 4.5 million bbls/day some 8% of the total world daily production. But, we believe Peak Oil has already been reached it was back in July 2008 and coincided with $147/bbl and a supply crunch before the world sank into recession in large part caused by the high oil prices (leading to inflation, higher borrowing, stress in payments, overheating and thence economic decline). The world will never produce as much oil as it did that month. The oil decline rate will increase as low oil prices stifle developments. Demand has dropped about 3% in the last year. Supply has been cut by a planned 8% - with 70% OPEC compliance - this is about a net 5%. But its just possible the underlying un-reported oil depletion (or decline) rate could increase from zero to 5% because of lack of investment in the next year or so. This would mean that when demand picks up after the recession, there will be a rapid supply-demand imbalance again similar to the one w

reduced and general production activity has waned. There is little incentive to boost production when much of this oil costs $20 to $40/bbl a barrel to extract after taxes. Meanwhile OPEC have cut production by a massive 4.5 million bbls/day some 8% of the total world daily production. But, we believe Peak Oil has already been reached it was back in July 2008 and coincided with $147/bbl and a supply crunch before the world sank into recession in large part caused by the high oil prices (leading to inflation, higher borrowing, stress in payments, overheating and thence economic decline). The world will never produce as much oil as it did that month. The oil decline rate will increase as low oil prices stifle developments. Demand has dropped about 3% in the last year. Supply has been cut by a planned 8% - with 70% OPEC compliance - this is about a net 5%. But its just possible the underlying un-reported oil depletion (or decline) rate could increase from zero to 5% because of lack of investment in the next year or so. This would mean that when demand picks up after the recession, there will be a rapid supply-demand imbalance again similar to the one w e predicted in September 2007 (spotted in date from June 2007) leading to the skyrocketing of oil prices over a short period of time possibly 6-12 months. We believe the scene is set for this scenario to occur just as the global economy pulls out of the recession, it will be hit by far higher oil prices and this will thence stifle growth, increase inflation, increase interest rates and cause further financial hardship for all oil importing nations. This is the reason why we have advised over the years to avoid investing in property in countries that have no oil production countries like:

e predicted in September 2007 (spotted in date from June 2007) leading to the skyrocketing of oil prices over a short period of time possibly 6-12 months. We believe the scene is set for this scenario to occur just as the global economy pulls out of the recession, it will be hit by far higher oil prices and this will thence stifle growth, increase inflation, increase interest rates and cause further financial hardship for all oil importing nations. This is the reason why we have advised over the years to avoid investing in property in countries that have no oil production countries like:

We have a neutral stance on the

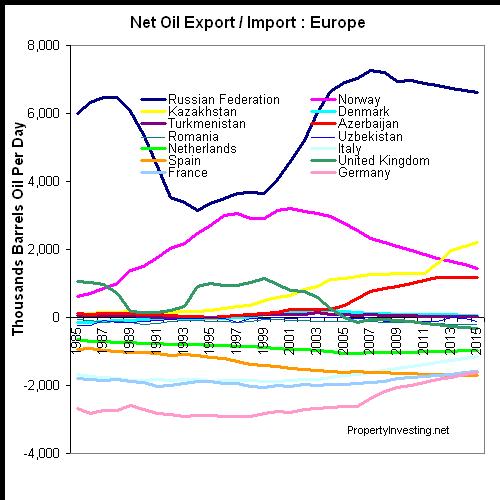

European and UK Oil Production Surplus and Deficit - Russia and Norway have big surpluses

If and when the oil prices rise again, the big winners will be

So for the property investor, the key messages are to focus investments in areas:

- with positive exposure to high oil and gas prices

- experiencing positive affects from regeneration, infra-structure developments, jobs and population growth

- exposed to an expanding private sector (whilst avoiding areas exposed to publics sector jobs and manufacturing jobs in the

We hope you have found this special report insightful if you have any comments please get back to us on enquiries@propertyinvesting.net

For further insights into the affect of oil prices on property investment, please refer to these Special Reports

- 251: Peak Everything !

- 246: Peak Oil - called July 2008 - massive switch needed despite $35/bbl oil

- 244: It's the oil price again - it caused the recession

- 243: Oil price crash sows seed for next massive oil spike

- 242: Oil, Cars & Property - what we'd do if we were UK Prime Minister

- 238: Oil, Cars & Real Estate - what we'd do if we were Pres. Obama

- 191: Oil Price Update and Real Estate

- 187: Real Estate and the commodities super-cycle

- 186: Oil price starts to skyrocket as predicted - how to profit

- 180: Oil prices continue to skyrocket

- 172: Make serious money - best investment sectors

- 169: Oil supply crunch begins protect yourself

- 168: Alarm bells ringing - oil price shock now on the horizon

- 163: Making Serious Money as asset prices plateau - resources and property

- 161: Resources winners and losers - ranked list for property investors

- 160: Find out the winners and losers in the biggest oil boom in history - about to happen...

- 159: Massive oil boom - the winners and losers - be prepared

- 158: Supply and demand scenarios - oil boom and the property investors insights

- 157: Impact of "Peak Oil" for Property Investment

- 151: Oil price $125 / bbl and rising how to take advantage in property

- 150: Peak Oil shortly due to be reach - unique insights for a property investor

- 148: Take advantage of the oil/gas/coal boom - key insights

UK areas most positively exposed to higher oil and gas prices are Aberdeen, Stonehaven and London.

Gas Pump Prices - are likely to rise in 2010 onwards