293: Property Investors update

10-17-2009

![]() PropertyInvesting.net team

PropertyInvesting.net team

The good news last week was that CPI inflation dipped to 1.1% with Retail Price Inflation (excluding mortage payments) dropping from 1.4% to 1.3% - this despite oil prices rising from $37/bbl in Q4 2008 to $70/bbl in September 2009. Its hardly surprising in view of the -4.5% GDP recession in the last year. But we were concerned inflation might actually rise from 1.8% this month because of the record amount of money being printed and oil prices rising. So it looks like interest rates rising has been put off for a while. But do not be fooled. If the economy starts taking off, euphoria starts kicking in, interest rates stay at 0.5% and oil prices start to sky-rocket, inflation we believe will be just around the corner and interest rates will then start to rise and it could happen quickly. Its rather uncertain how quickly this could happen. One thing we do not believe is that interest rates will stay at 0.5% for one or two years as many analysts believ e. We think rates will start rising some time in 2010 its just a question of when. And oil prices rising will be the leading indicator.

e. We think rates will start rising some time in 2010 its just a question of when. And oil prices rising will be the leading indicator.

Despite the global (or at least western world) financial crisis,

Peak Oil Reminder

Regular visitors to the website will know our view on oil prices and Peak Oil. We believe Peak Oil was July 2008 for all liquids oil production at ~86.5 million bbls oil/day. For conventional crude oil production, the peak was probably before this at a rate of ~75 million bbls oil/day, in May 2005. We are now on a bumpy plateau. Our rather optimistic model - suggests this bumpy plateau at a rate lower than July 2008 will continue until about 2014 then start to drop fairly slowly at a rate of 2-3% per annum. Meanwhile demand in the developing world is rising and will start to sky-rocket shortly. Demand in the developed world will be static some countries will be rising slightly, others like the

Oil Exporter Use More, Produce Less and Export Even Less

What many people fail to realize is that many of the big oil exporters will become net oil importer soon.

culators and everyone else that is keen to make a good return will jump on this bandwagon when they see this happening regrettably and drive oil prices higher. To think this will not happen we believe is over optimistic and probably unrealistic.

culators and everyone else that is keen to make a good return will jump on this bandwagon when they see this happening regrettably and drive oil prices higher. To think this will not happen we believe is over optimistic and probably unrealistic.

Positioning Your Portfolio of Assets

To make the best returns, one needs to position a portfolio of assets to be in the right things in the right place at the right time. Then just watch the asset prices rise.

As previously described, in oil exporting nations, asset prices will rise. In oil importing nations, economies and asset prices will be hit hard as oil prices rise, inflation rises, interest rates and costs rise then property prices drop. So we advise following our ranked list of countries that are most positively exposed to high commodity prices. And avoid those most negatively exposed to high commodities prices.

Top of the list for us are

Bottom of the list are Greece, Italy and Spain these countries have an aging population, declining population, no oil, gas, coal or metals to speak of, are not well known for financial services or manufacturing and have high social and labour costs they are also set to further suffer from the high Euro value with declining exports and lack of competitiveness. That said, we love

US Deficit and Crisis

To hedge against the massive

The shift away from the US dollar being the key commodities trading currency is likely to occur we believe in the next ten years and as early as 2015 - as the threat of the currency switch to a basket including Yen, Euro and Middle Eastern currencies increases more pressure will be exerted on the US dollar value. We are highly skeptical that the new US Administration will be able to or is even interested in reducing the massive $1.3 Trillion per annum deficit through cost cutting. Instead, by printing money and creating inflation, the perceived value of the debt would reduce over time if it could be controlled and capped on an annual basis. This will ultimately lead to the dollar decline possible to half its current value in the next five years. By printing money, inflating the economy to reduce the real terms impact of the massive deficit, foreign investors will take flight and invest money in stronger currencies such as the Euro, Canadian dollar, Australian dollar, Yen and possibly even UK Sterling if a new government in June 2010 starts tackling the massive UK deficit (its even possible the existing government could start to reduce it, though this is less likely).

The shift away from the US dollar being the key commodities trading currency is likely to occur we believe in the next ten years and as early as 2015 - as the threat of the currency switch to a basket including Yen, Euro and Middle Eastern currencies increases more pressure will be exerted on the US dollar value. We are highly skeptical that the new US Administration will be able to or is even interested in reducing the massive $1.3 Trillion per annum deficit through cost cutting. Instead, by printing money and creating inflation, the perceived value of the debt would reduce over time if it could be controlled and capped on an annual basis. This will ultimately lead to the dollar decline possible to half its current value in the next five years. By printing money, inflating the economy to reduce the real terms impact of the massive deficit, foreign investors will take flight and invest money in stronger currencies such as the Euro, Canadian dollar, Australian dollar, Yen and possibly even UK Sterling if a new government in June 2010 starts tackling the massive UK deficit (its even possible the existing government could start to reduce it, though this is less likely).

Just to put this

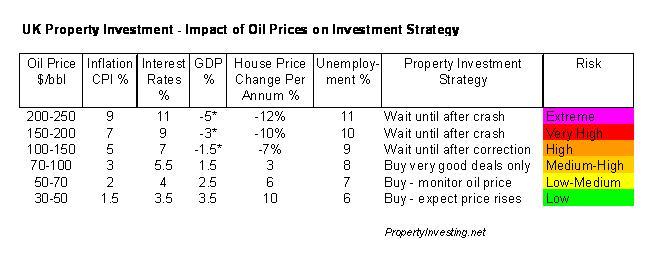

High Oil Price = High Inflation = High Interest Rates = House Prices Dropping

-and low GDP growth and high unemployment-

However, expect the following currencies to increase in value as commodities price rise:

- Australian Dollar

- Norwegian Kronar

- Canadian Dollar

- Russian Ruble

Trends

Here is a simple summary of the trends we describe:

- US dollar declines

- Oil and metal prices rise

- Inflation Rises

- Yen and Euro increase

- Property prices in all major western oil importing nations decline or stagnate

- Property prices in all major oil exporting nations increase

- Interest rates rise

- Correction when oil prices rise above $150/bbl, recession and prices drop to new higher baseline of $70/bbl.

Peak Oil - World Oil Production Consumption

This is only our view and a scenario we call our base we all have our own opinions and we can acknowledge if you think differently. We have tried to be objective, realistic and helpful in our analysis for

- Decline oil production not enough oil to meet demand (OPEC production will not be able to keep up or make up the gap of lowering Non-OPEC oil production)

- Increasing inflation

- A run on the dollar

- Oil prices rising as a hedge against the declining dollar (this has started)

- Most likely another financial crash in western economies after oil prices top $150/bbl again

Anyone that thinks the

Anyone that thinks oil prices will not rise as the dollar continues to decline? Likely answer - no.

So the scene is set for another commodities bull market as

Again, anyone think the Chinese will hold back? Likely answer no.

If you are skeptical about how much oil

It all points in one direction. Be careful and shrewd with your investing.

Is there anywhere left that looks like a low risk high growth area? Well

Country Ranking

What we have prepared are two tables. The first table is a Pure Peak Oil Profits table that ranks each country on:

-

amount of oil exports (green) or oil imports (red)

-

amount of gas exports (green) or gas imports (red)

-

demomgraphs moderately expanding population (green) or declining population (red)

-

stability - a summation of political, country risk, security and threat of war - green is stable, red is unstable

The rating is intuitive and qualitative - using our experience and judgement. You may not agree with all of the criteria ratings - however, we believe its a fairly measure of the countries that will do well from Peak Oil and those that will suffer the most fron Peak Oil. No surprise that Norway and Canada come top. These two countries have huge oil and gas deposits, growing but relatively small populations (or oil revenue per person) and are very politically stable with excellent security. Expect their currencies and property prices to rise as oil prices rise.

|

|

Oil |

Gas |

Demographics |

Stability |

Overall |

|

Norway |

10 |

10 |

8 |

10 |

38 |

|

Canada |

10 |

8 |

8 |

10 |

36 |

|

Brunei |

10 |

10 |

8 |

8 |

36 |

|

Australia |

6 |

10 |

8 |

10 |

34 |

|

UAE/Dubai |

10 |

8 |

7 |

6 |

31 |

|

Algeria |

8 |

10 |

8 |

5 |

31 |

|

UK |

7 |

7 |

7 |

9 |

30 |

|

Russia |

10 |

10 |

3 |

6 |

29 |

|

Saudi Arabia |

10 |

8 |

7 |

4 |

29 |

|

Brazil |

7 |

7 |

7 |

7 |

28 |

|

USA |

2 |

9 |

7 |

9 |

27 |

|

China |

5 |

6 |

7 |

5 |

23 |

|

India |

4 |

4 |

8 |

4 |

20 |

|

Korea |

0 |

0 |

7 |

7 |

14 |

|

South Africa |

0 |

2 |

7 |

3 |

12 |

|

Portugal |

0 |

0 |

4 |

8 |

12 |

|

Japan |

0 |

0 |

3 |

8 |

11 |

|

Spain |

0 |

0 |

3 |

8 |

11 |

|

Italy |

0 |

0 |

3 |

8 |

11 |

|

Greece |

0 |

0 |

3 |

8 |

11 |

Legend

Big opportunity - positive

Opportunity - positive

Neutral - hedged

Threat - negative

Severe threat - very negative

|

Oil |

Gas |

Coal |

Metals |

Finance |

Manufa-cturing |

Agricul-ture |

Know-ledge |

Demo-graphics |

Stability |

Overall | |

|

Canada |

10 |

8 |

9 |

9 |

9 |

5 |

8 |

10 |

8 |

10 |

86 |

|

Australia |

6 |

10 |

10 |

10 |

9 |

5 |

8 |

10 |

8 |

10 |

86 |

|

USA |

2 |

9 |

10 |

8 |

10 |

5 |

10 |

10 |

7 |

9 |

80 |

|

China |

5 |

6 |

10 |

8 |

8 |

10 |

7 |

8 |

7 |

5 |

74 |

|

Brazil |

7 |

7 |

7 |

9 |

7 |

7 |

9 |

7 |

7 |

7 |

74 |

|

Russia |

10 |

10 |

9 |

8 |

7 |

5 |

6 |

7 |

3 |

6 |

71 |

|

Norway |

10 |

10 |

0 |

0 |

7 |

5 |

4 |

9 |

8 |

10 |

63 |

|

UK |

7 |

7 |

1 |

1 |

10 |

4 |

7 |

9 |

7 |

9 |

62 |

|

India |

4 |

4 |

9 |

5 |

7 |

7 |

4 |

8 |

8 |

4 |

60 |

|

Brunei |

10 |

10 |

0 |

0 |

6 |

2 |

4 |

7 |

8 |

8 |

55 |

|

UAE/Dubai |

10 |

8 |

0 |

0 |

8 |

5 |

1 |

8 |

7 |

6 |

53 |

|

South Africa |

0 |

2 |

10 |

10 |

3 |

5 |

6 |

5 |

7 |

3 |

51 |

|

Japan |

0 |

0 |

4 |

2 |

8 |

10 |

5 |

10 |

3 |

8 |

50 |

|

Algeria |

8 |

10 |

2 |

2 |

4 |

3 |

2 |

4 |

8 |

5 |

48 |

|

Saudi Arabia |

10 |

8 |

0 |

0 |

7 |

3 |

1 |

6 |

7 |

4 |

46 |

|

Korea |

0 |

0 |

4 |

0 |

7 |

10 |

3 |

8 |

7 |

7 |

46 |

|

Spain |

0 |

0 |

0 |

1 |

8 |

4 |

8 |

8 |

3 |

8 |

40 |

|

Italy |

0 |

0 |

0 |

1 |

7 |

3 |

7 |

8 |

3 |

8 |

37 |

|

Greece |

0 |

0 |

0 |

1 |

6 |

4 |

6 |

7 |

3 |

8 |

35 |

|

Portugal |

0 |

0 |

0 |

1 |

5 |

4 |

7 |

6 |

4 |

8 |

35 |

Peak Oil

| Peak Oil Susceptibility Index | ||

| - impact of high hydrocarbon prices - | ||

| Country | Hydrocarbons Production Surplus Tons Oil Equi/ Person/ Year | |

| Kuwait | 39.73 | |

| Brunei | 39.63 | |

| Norway | 38.64 | |

| UAE | 24.76 | |

| Turkmenistan | 20.91 | |

| Saudi Arabia | 17.95 | |

| Libya | 17.79 | |

| Kazakhstan | 15.66 | |

| Oman | 10.86 | |

| Australia | 7.35 | |

| Trinidad & Tob | 6.98 | |

| Venezuela | 5.05 | |

| Bahrain | 4.98 | |

| Azerbaijan | 4.96 | |

| Qatar | 4.55 | |

| Algeria | 4.18 | |

| Canada | 4.11 | |

| Russia | 3.77 | |

| Iraq | 3.67 | |

| Angola | 3.22 | |

| Iran | 1.92 | |

| Colombia | 1.40 | |

| Syria | 1.25 | |

| Vietnam | 1.17 | |

| Nigeria | 1.07 | |

| Malaysia | 0.99 | |

| Ecuador | 0.97 | |

| Mexico | 0.80 | |

| South Africa | 0.69 | |

| Equatorial Guinea | 0.68 | |

| Bolivia | 0.56 | |

| Indonesia | 0.55 | |

| Denmark | 0.46 | |

| Argentina | 0.46 | |

| Yemen | 0.42 | |

| Egypt | 0.24 | |

| Sudan | 0.18 | |

| Rep. of Congo | 0.15 | |

| Myanmar | 0.13 | |

| Turkey | -0.01 | |

| Bangladesh | -0.03 | |

| India | -0.11 | |

| Brazil | -0.12 | |

| China | -0.13 | |

| Pakistan | -0.14 | |

| Romania | -0.29 | |

| New Zealand | -0.57 | |

| Poland | -0.60 | |

| Czech Republic | -0.60 | |

| Thailand | -0.71 | |

| United Kingdom | -0.80 | |

| Greece | -0.98 | |

| France | -1.15 | |

| Ukraine | -1.58 | |

| Netherlands | -2.24 | |

| USA | -2.39 | |

| Germany | -2.67 | |

| Italy | -2.71 | |

| Spain | -2.87 | |

| South Korea | -3.95 | |

| Japan | -7.81 | |

| Legend | ||

| Positive impact | Economic Benefit | |

| Neutral impact | ||

| Negative impact | ||

| Strongly -ve impact | ||

| V.worrying impact | Economic crisis | |

Happy investing

Appendix

Rio Olympics 2016

Rio won the 2016 Olympic bid on 2nd October 2009. We enclose a few photographs illustrating this major achievement for Brazil and South America.

Rio Olympics 2016

Rio Olympics 2016

Rio Olympics 2016 Brazil

Rio Olympics - Pele and Mr Lula

Rio Olympics 2016 - Barack Obama hopes were dashed for Chicago's bid

Adriana Lima - Bazilian supermodel - happy

World Famous Rio Carnival in April each year - a stunning show of costumes, arts and cultural experiences that draws people from the world over.

Graziele Massafera

Rio Carnival Men

Brazil Carnival Rio

Samba

Brazil festival carnival man

Men Carnival Rio

Viviane Rio

Veronica star

Quiteria Chagas

Raissa de Oliveira

Thatiana Pagung

NATALIA GUIMARAES by Dubiellla

Angela Bismark

Rio Carnival

Carnival Rio Men - preparing for Samba

Queen Carnival Rio

Rio Carnival

Rio Carnival

Rio Carnival night daner

Brazil Carnival Rio de Janeiro 2009

Adriane Galisteu

Viviane Araujo

Samba Stadium

Rio Angela Bismarck

Brazilian Samba Dancers

.jpg)

Karna Valresimleri

Dancer Rio

Rio samba dance

Rio Carnival

Viviane Araujo

Grand Rio