384: Super Cycle - 60% Through Stock Bear - Inflation All The Way From Now

07-02-2011

PropertyInvesting.net team![]()

We think you'll find this model very interesting!

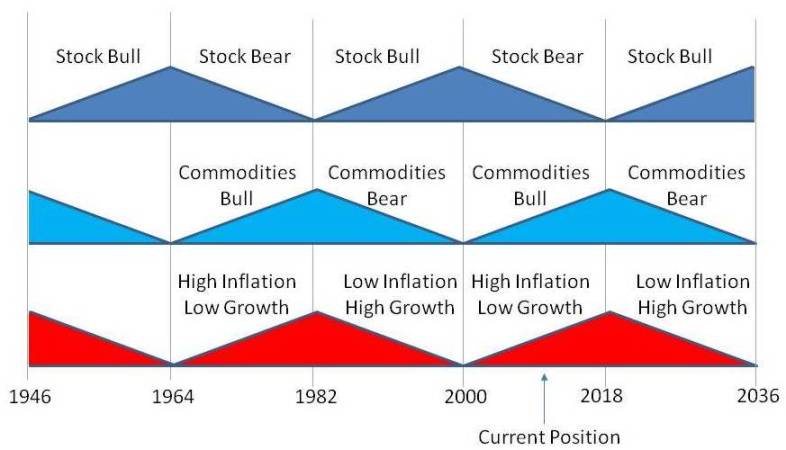

Super-Cycle: We believe western economies are about 60% of the way through an 17.5 year bear stock market. This began in March 2000. The crash of 2008 was part of this overall down cycle the final 40% leg of this bear market will lead to significantly higher inflation along with a commodities bull run through to about early 2018. As inflation rises, western living standards will be eroded, interest rates will rise, the stock market will drift laterally or down and probably ending in early 2018 at a lower level than in 2011, but inflation adjusted this level will be down some 40% from todays levels. We also expect a mini-stock market crash in the next 6-12 months down by about 25%, but this will just be a correction in an overall lacklustre bear market leading to a low somewhere 2018. Well expand on this in our next Newsletter mid July because it is critical to describe this analysis in depth as context to property investment and other asset purchases. Investors often shift out of the stock market into property and commodities (oil, gold, coal, metals, food) as a hedge against inflation. And in our view, for the next 7 years, it will be inflation all the way corresponding to disappointing GDP growth in western developed nations. So called stagflation before the end of the bear market in 2018.

InterPlay Between Inflation, Stock Market Values, Commodities and Debt: Looking back through western developed economic history, there are large scale cycles that last about 18 years. The start of a stock bull run normally commences after about 18 years of sideways moving stock market after a prolonged period of inflation, stagnation and high commodities prices. The investor psychology is one of complete lack of trust, enthusiasm and interest by that stage in the stock market. Average P/E ratios have dropped to 10. The bull run begins after a commodities price crash - growth is fuelled by low energy, metal and food prices. More disposable income is  available for consumer spending. Interest rates are low, and company profits are rising. Tax rates are dropping and government debts are reducing as tax receipts rise and oil import bills reduce.

available for consumer spending. Interest rates are low, and company profits are rising. Tax rates are dropping and government debts are reducing as tax receipts rise and oil import bills reduce.

Commodities Bull: People shift from cash and commodities to risk, stocks and shares - and follow the stock market higher. Energy prices remain low as plentiful energy and lack of energy speculation keeps commodities prices down. People prefer to invest in stocks and shares - retail shares do particularly well.

Euphoria: This 18 year cycle ends with euthoria, people saying things are completely different this time and P/E ratio rise over 30. This happened in March 2000. The stock market then crashes. Interest rates drop, and there is a relief rally. But the money from stocks and shares is shifted into commodities - and oil prices start rising. But this ends with another crash some years later (example mid 2008) - the 18 year bear market has begun. Mid way through this cycle, governments normally get desperate and start printing money. This then starts speculation in commodities and they rapidly rebound and are driven higher. This then feeds through even more to inflation, which supresses stock market values as people have less money to spend and companies profits are put under pressure. Lower average GDP growth begins, government debts rapdily rise and investor pile into the commodities bull run. This in turn drives inflation higher, governments have to then start putting up interest rates - this has a disasterous affect as governments cannot afford the interest rates charges, and banks refuse to lend to each other. The only way out is for the governments to keep trying to inflate their way out of trouble - printing money - but this then leads to reduced disposable income, higher unemployment, higher inflation, and lower GDP growth with miserable tax receipt despite tax rises.

- the 18 year bear market has begun. Mid way through this cycle, governments normally get desperate and start printing money. This then starts speculation in commodities and they rapidly rebound and are driven higher. This then feeds through even more to inflation, which supresses stock market values as people have less money to spend and companies profits are put under pressure. Lower average GDP growth begins, government debts rapdily rise and investor pile into the commodities bull run. This in turn drives inflation higher, governments have to then start putting up interest rates - this has a disasterous affect as governments cannot afford the interest rates charges, and banks refuse to lend to each other. The only way out is for the governments to keep trying to inflate their way out of trouble - printing money - but this then leads to reduced disposable income, higher unemployment, higher inflation, and lower GDP growth with miserable tax receipt despite tax rises.

Depressed Market: Eventually, stock markets decline further, and governments or companies and banks default. The economy goes into a meltdown as governments can no longer afford to "save" any bank or country. Investors lose billions. Stocks are trading at P/E ratios of 10 and the bear market ends. The bull market commences when taxes are reduces, government spending has been slashes, size of goverment reduced, oil prices have crashed and the conditions are right for private enterprise to grow again.

Bear Until 2018: The bear market started in 2000, and we thin k it will end in 2018. Up until then, inflation will rise sharply. We forecast the FTSE100, Dow Jones and Nasdaq to crash by 25% from current levels sometime in the next six months. This is consistent with the mid cycle 2008 crash of 50%, with a second smaller crash of 25% a few years later. After the second crash, the stock markets should drift sideways, but in inflation adjusted terms - assuming inflation of about 6-8%, the stock market would loose a further 50% in real terms from now until 2018 - the end of the bear market.

k it will end in 2018. Up until then, inflation will rise sharply. We forecast the FTSE100, Dow Jones and Nasdaq to crash by 25% from current levels sometime in the next six months. This is consistent with the mid cycle 2008 crash of 50%, with a second smaller crash of 25% a few years later. After the second crash, the stock markets should drift sideways, but in inflation adjusted terms - assuming inflation of about 6-8%, the stock market would loose a further 50% in real terms from now until 2018 - the end of the bear market.

Supply and Demand: As developing nations continue to grow at 4-12% GDP per annum, this will suppress growth in the OECD developed nations like USA and western Europe. The financial shock of 2008 causes an 18 month delay in commodities investment that is now starting to feed through to supply shortages in oil and mining. We expect a number of waves to develop in commodities with corrections in between following inflation upwards - until a final blow-off occurs some time between 2014 and 2018 then some form of financial meltdown, commodities crash and ultra-low stock market valuations will signal peak pessimism and the start of the next stock market bull run. At these low stock market valuations, P/E ratios should be aorund 10.

.gif)

- Deleveraging is required through printing of money - as exchange rates decline, inflation through higher imported goods prices feeds through

- Printed money is used by speculators to buy commodities as a hedge against inflation (or the printed money)

- Government compete to print there way out of debt - drive down living standards by stealth as inflatione exceed wage settlements

- Government have a misguided view that deflation might take hold - this is highly unlikely because the mid cycle crash in 2008 for instance was a deleveraging of risk/debt after a bubble formed from too many years of too low interest rates

- Investment in private companies reduces as everyone knows the bear market will be prolonged - this leads to supply constraints on commodities that further drive oil, gas, coal, food and metals prices higher.

Action For Investors: So the thing to do is to:

- exit stocks and shares except for commodities companies (particularly avoid retail companies in western developed nations) - until the end of the bear market sometime around 2018

- buy gold, silver, oil, gas, coal, shale gas, metals, food, land, water

- invest in developing nations like India, China, Brazil and Vietnam

- shift investment in developed countries to those with many commodities - like Norway, Canada and Australia (also with safe stable currencies)

- invest in high end properties in cities that rich people buy - this is because the richest people are selling stocks and shares, and buying any asset that will be a good hedge against inflation - up until 2018. Property is a well know excellent hedge against inflation - particularly if prime property in places like central London (generally cash buyers). Even if property prices are a little short of inflation, the overall debt during high inflationary times decreases rapidly and hence the proportional equity increases, as long as the loan is fairly small and there is no concern paying loan rates that might rise rapidly for period.

- invest in high quality technology companies that are expert at energy conservation and low cost renewable energy

Nutshell: This is it in a nutshell. For the next 7 years, this will be the way forward. This is what we will be doing.

- London property (as central as possible)

- Smaller oil and shale gas stock market picks

- Looks for ways to get into Canada, China, India, Norway - and considering safe havens like Switzerland

Next 7 Years: It's going to be a very rough down period with high inflation starting very shortly. Watch out, see the interest rates start to skyrocket by end 2011 and don't be surprised if you see more printed money flying around - heading into commodities and thence feeding through further into oil prices again. It's a clear:

- commodities bull market

- stock bear market

- inflationary period, with

- higher interest rates coming...

We don't think we'll be wrong in this central prediction.