430: Edging Toward The 2013 Crash

06-09-2012

![]()

PropertyInvesting.net team

Background - Bear Market Super Cycle: It's now mid 2012 and we are more than 70% of the way through a cyclical bear market in the stock market. Remember the Dow Jones reached an all time high in March 2000 and is now about 50% of the way down in inflation adjusted terms from its high. The same is true for the FTSE100 its about half the value of March 2000. This trend will continue for another 4-5 years and when it ends, very few private individuals will be interested in the stock market. We certainly have not go there yet a good example is the ridiculous Facebook IPO that valued this company at $104 Billion it is still owned 51% and fully controlled by one person the 29 year old founder. This is the height of hype, euphoria and over-optimism that a company like this can be worth so much. Time will tell if we are right on this, but its another tech bubble in our view, 12 years after the last one. No doubting it's a great company, but not worth $104 Billion.

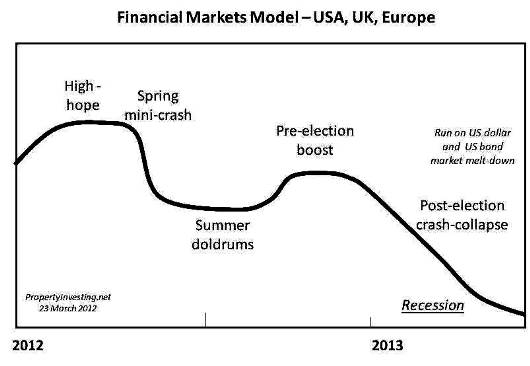

Mini-Summer Crash: The mini-stock market crash happened exactly as we predicted - see Special Report 417. But we expect some form of improvement in the stock market as QE3 starts mid year just in time to give President Obama a boost before the election - and planned to do so. It should prop the stock market back up for a while. But the real action will be in 2013. This is when laws have been passed in the USA that say public spending will be cut. Just be minded that trillions of dollars of printed money has hardly got the US economy moving up until now.

Chart Prepared in March 2012

Growth is slowing. Things will stumble onwards until early 2013 when these cuts start and then it will become very obvious that the US is back in recession. When the US markets get wind of this, then the stock market will crash, bond rates will skyrocket and the dollar will crash. Then global markets will be spooked and interest rates for the US will be forced higher at this point massive pressures will start to exert themselves on the US financial markets and an implosion will occur. Sometime between January and July 2013 we predict.

Europe: The current Eurozone problems have come at a convenient time for the US Administration. Money has transferred from Europe to the USA that is currently considered a relative safe haven. Europe has significant problems, and they don't look as if they are going to go away any time soon, but at least they are trying to do something about the high public sector spending - Spain in particular. Its deflected the attention well away from the USA's own debt problem and boosted inflows, driving down bond yields - and allowing the US to continue with low interest rates for now. If the Fed print some money mid-year it should boost the stock market just enough before the election to get President Obama re-elected. But after this, global markets will finally turn on the USA when it becomes very obvious the country is in recession and cannot pay back its debts long term.

Quiet 2012: For the time being, things are relatively quiet. This is as we expected. Of interest is the very thin trading in the Dow Jones the average person is almost absent from the US stock market and there is little interest people are awaiting for the next big move. They are hoping to ride another QE wave before the election - hanging around for this opportunity.

But after this next QE wave is exhausted the smart investors will get out of this cyclical bear market and run for the hills. When panic starts, gold and silver prices will go through the roof sometime early 2013.

For the individual investor, our guidance is to be well out of the stock market at this time, unless its in mining stocks or possible oil stocks. Mining stocks have been pounded down to very low values - they look a bargain. But overall, being in the stock market is really not worth the risk for most investors because we are waiting for the next big down-leg. Most likely shortly after the US election in November.

Most money managers and investors in the US are currently quite optimistic and bullish about future prospects they genuinely believe the economy is growing in a sustainable fashion and are looking forward to QE3. This is the time to get out of the way its the end of this cycle. The Dow has doubled since its low in early 2009 - an amazing achievement considering the fundamentals - mostly through printed money stimulation. But its very likely to go into reversal. Just consider the underlying fundamentals:

US Endemic Problems: Essentially, we believe the USA has the following endemic problems that show no sign of being rectified:

· $15.5 Trillion debt that is too large 100% of GDP

· $1.62 Trillion annual deficit

· Government spending that is $1 Trillion higher than tax receipts

· Over-regulation by a central government that is far too large - and getting proportionally larger

· Rising taxes too high for private investment

· Expanding public sector totally unsustainable

· Long term unemployment and under-employment

· Education loans bubble and liability loans that are unlikely to be repaid back

· The US debt is projected to increase to $22 Trillion by 2020 but this is based on an assumption that GDP growth will be 4% above inflation (we think this is impossible - for example, unlikely the 1990s when bold new innovations like the internet, PCs, cell phones improved productivity, we see no such new technology on the horizon end 2011)

· Annual deficit that is too large 10% of GDP

· No debt or spending reduction plans a meagre deferred $30 Billion automatic spending cut per annum is just a drop in the ocean (1/20th of the annual cost of US crude oil)

· Too many guns in case of civil disorder the downside is bleak

· A socialist government that has part nationalised banks banks are bankrupt and only able to continue because of Fed interest rates set at 0.5% whilst banks lend at 5%

· The US borrows 40% of its spending requirements for every $1 Billion is spends, it borrow $400 mln

· A 6% interest rate on $15 Trillion would mean all tax receipts would be used to make annual debt repayments

· Medicare bills are far too large - $7000/person/per annum

· Military spending is far too high - $1500/person/per annum

· Oil import costs are far too high - $1500/person/per annum

· Education spending that has doubled in ten years out of control

· Gigantic exposure to a $85 Trillion bond market that will eventually collapse causing interest rates to sky-rocket

· Not enough productivity growth to stimulate real GDP growth and repay debts

· Underlying inflation that is not being properly measured inflation is probably already 8-10% whilst official figure show ~3.5%

· Private US industry has about $2 Trillion sitting on the sidelines (Apple has ~$60 Billion alone) confidence is so low that these companies choose not to invest the cash in the USA

· A government and Fed run by politicians and academics are propping up failed banks leaders are in denial

Dollar Global Reserve Currency: The only thing keeping the whole show on the road is the historic reputation of the US dollar as the global reserve currency when this wanes with every bout of printed money coinciding with China's rise in economic power there will become a tipping point when international investors no longer seek the dollar as a so called safe haven at this point the US bond market bubble will collapse

If you took away the US dollar as the global reserve currency, the standard of living of the average American would crash by at least 25% - because they would no longer be able to print money, get away with this, and keep inflation in check. Instead, interest rates would sky-rocket and inflation would take off.

There are a few things that keep the dollar as the reserves currency at this time. Firstly the Eurozone weakness helps push cash flows into the dollar. Secondly the US military might and support for oil producing governments means people still trade oil in dollars. Thirdly the Chinese have pegged their currency to the dollar for now to allow cheap exports into the USA. But just imagine a scenario where over time:

-

The US military might is eroded and global presence diminishing in part because they cannot afford this military effort any longer

-

Oil producing nations no longer care about the US military a change of regime or leadership could cause this

-

The Chinese float their currency as they switch to an internal consumer lead economy in a similar way that the USA did in the 1950s onwards. The Chinese economy becomes so large and efficient that it challenges the US economy and currency as the global reserve currency then people switch to the Chinese currency instead.

Slow Loss Of Status: All these three things are happening slowly at this time. What would accelerate the process would be international investors realisation that there is not way the US can ever pay back its debts and they desert the bond markets because of this driving up interest rates. This in our view is very close to happening. It only takes the US bond markets to implode to destabilize  the whole economic engine of the USA and drive the country into recession.

the whole economic engine of the USA and drive the country into recession.

Our central prediction is that this process will start in earnest in early 2013 triggered by the reduction in government spending after the US election. When the stock market crashes, a few months later it will be obvious the US is in recession. Then people will calculate that tax revenues will drop and there is absolutely no way the US will ever be able to pay back its debts. Then interest rates will sky-rocket. The Fed will be forced to print huge quantities of money again, but this will cause the dollar to decline further, increase import costs, increase inflation and then the prices of gold will sky-rocket, along with it oil. If the US economy then gets a severe recession, global panic would set in and everyone will dash to a new safe haven. The only real safe havens left will be:

Gold, possibly silver

Norway, Canada, Australia, Switzerland

London only if the financial meltdown does not harm this city too much

The countries that would proportionally suffer the worst fall out will be:

Greece, Spain, Portugal, Ireland, Italy along with the USA

UK Situation: The UK could benefit because the government is at least independent, trying to tackle the budget deficit and re-balance the public and private sectors. It could get dragged down with the rest, but it could also be considered a safe haven we are not sure its rather on the edge and could go either way. The thing is, markets will decide which are risky and price this in and those countries that look like not paying back their debts will see interest rates sky-rocket and their economies will suffer because of this with high unemployment and low investment.

The underlying cause of all this economic decline is:

· Years of too much public sector spending that has swamped the private sector with regulation, cost and taken some of the best people out of the employment sectors

· Years of countries spending beyond their means raking up massive debts

· Governments in times of recession trying to spend their way out of trouble making matters worse

· Cost of employment going too high with jobs and manufacturing moving to lower cost centres in South Asia and Asia

· An entitlement culture where individuals look to the state to provide everything stifling innovation, hard work and enterprise

· Aging populations with many countries having declining populations and/or proportionally older populations

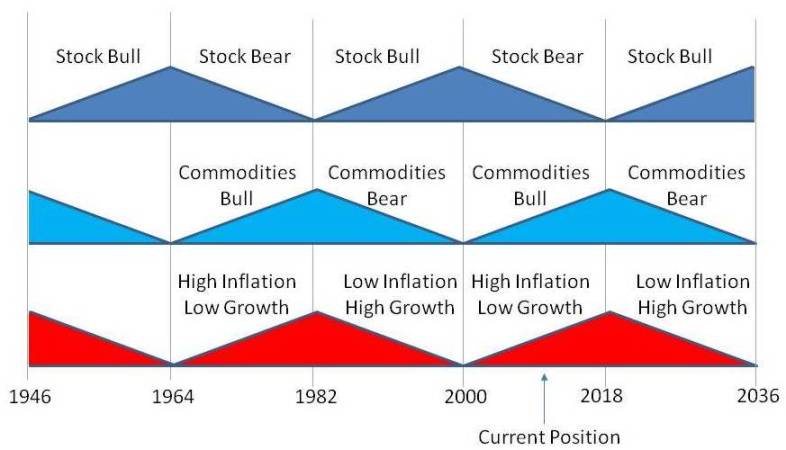

Time for a Recession: It has been 4 years since the last major recession, high commodities prices have stifled economic growth in most western countries and we are about to embark on the next cyclic downturn in 2013 this will be five years. Throughout the period from 1960 onwards, its been quite normal to have a recession every five years. The only reason there was no recession from 1992 to 2008 was because of low oil prices, low inflation, increasing borrowing and outsourcing to China that kept a lid on inflation. Hence this cheap money stimulated the western economies. As oil prices rose in 2005, this never ending growth is no longer possible in oil importing nations as the affects of Peak Oil hit the economies oil supply is constrained versus demand and these high oil prices act as a further tax on business and governments. For the optimists in the US that still believe we are beginning to see a recovery, let's get real, it's been almost five years since the last recession. If there was to have been a recovery we would have seen it strongly by now with zero 5 interest rates and Trillions of dollars of printed money trying to stimulate the economy. Most of this money seems to have been spent on non-productive jobs and regulations. The productivity gains of the period 1980 to 2000 have disappeared.

hit the economies oil supply is constrained versus demand and these high oil prices act as a further tax on business and governments. For the optimists in the US that still believe we are beginning to see a recovery, let's get real, it's been almost five years since the last recession. If there was to have been a recovery we would have seen it strongly by now with zero 5 interest rates and Trillions of dollars of printed money trying to stimulate the economy. Most of this money seems to have been spent on non-productive jobs and regulations. The productivity gains of the period 1980 to 2000 have disappeared.

Financial Crash: The 2008 financial crash was exactly that a financial crash in the private sector. The big mistake was for governments to step in and take over poorly performing banks using tax payers money to bail them out. The US also bailed out or nationalised the auto industry, Freddie Mac and Fannie Mae along with JP Morgan, AIG and other banks. This meant the private sector debt was transferred as sovereign debt (or tax payers public debt). This massive mistaken means all the governments are now holing the debt and they cannot pay it off because their tax receipts are not high enough. The increased regulation and increased taxes has stifled the private sector even further and reduced tax receipts even further. This vicious circle means governments know they cannot pay off their debts ever the only option is to try and print money or deflate their currencies to make the debt more manageable. The UK is quietly doing this this is why prices have risen 5% per annum, wages 3.5%, disposable incomes have decline by 2% per annum and taxes have risen whilst GDP growth has been barely 1.5%. The Bank of England and Coalition must wander how they have managed to achieve this with more public opposition one can only think the public must realise what a mess the Labour government caused and are going along with this austerity plan in the form or inflation and decline in living standards the good news is that as long as there is not another recession in the UK real disposable incomes are projected to increase in 2013 as taxes decrease and inflation subsides somewhat we will see.

![]() Iran: Looming out there is the ever present Iranian nuclear issue. It's unlikely anything but posturing will happen before the US Election in Nov 2012. But after this, in early 2013 this could come to the fore again. Wars have a habit of correlating with times of economic hardship - its quite possible regrettably then whole issue will flare up by Jan 2013. The chance of an amicable negotiation mid 2012 has to be small.

Iran: Looming out there is the ever present Iranian nuclear issue. It's unlikely anything but posturing will happen before the US Election in Nov 2012. But after this, in early 2013 this could come to the fore again. Wars have a habit of correlating with times of economic hardship - its quite possible regrettably then whole issue will flare up by Jan 2013. The chance of an amicable negotiation mid 2012 has to be small.

Property Investing: For property investors, much rests on whether we should expect inflation or deflation. Some independent experts still believe a massive deflationary period will occur from early 2013 onwards. We agree there should be a crash which will be deflationary, but we think that governments will do everything in their powers to prevent prices dropping to negative and wages dropping they will just print more money and  prop the whole lot up again. Ultimately we thing that inflation will run out of control as inefficiencies build up and commodities prices rise sharply. We cannot be certain about this, but we think capacity constraints in energy particularly oil and mining along with agriculture, will lead to higher prices and inflation globally. The reason this is so important is that property does well during inflationary periods, particularly if the interest rates dont sky-rocket. Many wealthy people buy property as a hedge against inflation. If you buy property with cash, then as prices rise, your property will rise with it. If you have debt on the property, then real value of the debt will be eroded. This is a key reason why most very wealthy people have a large property portfolio and exposure to property. The worst scenarios for property is long term deflation as was experienced in Japan and if this was to be repeated in the USA and UK then it would be time to get out of property right now. Although we think there will be a financial crash in the western world in 2013, and property prices would likely suffer, we thing the ensuing inflation will be good for property prices. Furthermore, if people liquidate their stock market holdings into cash they often then buy property with this cash and inflation the property prices. This happened in the period 2000 to 2002, as the stock market bubble ended then started the real estate bubble in both the UK and the USA.

prop the whole lot up again. Ultimately we thing that inflation will run out of control as inefficiencies build up and commodities prices rise sharply. We cannot be certain about this, but we think capacity constraints in energy particularly oil and mining along with agriculture, will lead to higher prices and inflation globally. The reason this is so important is that property does well during inflationary periods, particularly if the interest rates dont sky-rocket. Many wealthy people buy property as a hedge against inflation. If you buy property with cash, then as prices rise, your property will rise with it. If you have debt on the property, then real value of the debt will be eroded. This is a key reason why most very wealthy people have a large property portfolio and exposure to property. The worst scenarios for property is long term deflation as was experienced in Japan and if this was to be repeated in the USA and UK then it would be time to get out of property right now. Although we think there will be a financial crash in the western world in 2013, and property prices would likely suffer, we thing the ensuing inflation will be good for property prices. Furthermore, if people liquidate their stock market holdings into cash they often then buy property with this cash and inflation the property prices. This happened in the period 2000 to 2002, as the stock market bubble ended then started the real estate bubble in both the UK and the USA.

Possible Switch To Property: The Trillions of dollars of stimulus have clearly so far not gone into the real estate market they have gone into the stock market and commodities plus bonds as a so called safe haven. But when this bubble pops, there is a chance this money will flood into property as a s afe haven at least its a physical tangible asset that can be used for something and cannot be confiscated. You can use property to live in always handy and required

afe haven at least its a physical tangible asset that can be used for something and cannot be confiscated. You can use property to live in always handy and required

Gold and Silver: Any gold prices less than $1550/Troy ounce is in our view very good value. Any silver prices less than $28.50/Troy ounce is in our view very good value. We actually expect to see gold and silver prices to sky-rocket from them platforms in the next six months - it will take a while, but when it starts - it could move very fast. Gold, silver and mining stocks have all been beaten down - some big players want to shake out the small players. Central banks are buying gold at $1550/Troy ounce giving support at this level. We don't thing we'll ever see these types of prices again frankly. Silver in particularly is - we believe - the bargain of the century.

Conclusion: In summary, expect further turbulence in the stock markets through 2012 with QE3 by mid 2012 President Obama will win the election promising four more years of socialism. Then in 2013 the crash will happen its only 7-12 months away now. Then we should see deflation for a while then rampant inflation abot a year or two later as central banks start the printing presses in a vein attempt to get economies moving but this time, unemployment will rise sharply and with it inflation and gold prices will skyrocket. At this point, it will look like 1980 all over again severe recession, high oil prices, war in the Middle East and skyrocketing gold prices as people panic. It will take years to recover. But at the depth of the despair sometime between mid 2013 and 2017 will be the time to buy cheap assets again - cheap stocks. For now, for us anyway, its gold, silver, oil and property investment nothing else. And if you own any Facebook shares sell them fast!

European Championships Predictive Model

Just for a bit of light relief, the PropertyInvesting.net team got together and prepared this qualitative model to try and predict who would win the European Championship. Observatio ns of past winners have been that the countries with the best performing economies at that time are more likely to win. This might have to do with the national psyche at the time, confidence and self esteem.

ns of past winners have been that the countries with the best performing economies at that time are more likely to win. This might have to do with the national psyche at the time, confidence and self esteem.

To show how we have calculated it - firstly we rate the country's relative economic performance. 1 one is desire financial disaster and degradation. 10 is steady growth, stable and lowering unemployment. In Europe, we rate Germany the best economic performance at this time. Greece has the worst.

Then we take the quality of the team. 10 is the best. 1 is the worst. We then simply multiply one with the other (or add one with the other).

You can see Germany comes out top. Greece bottom. Netherlands second some way behind. Interestingly, England sneaks into third position. although the quality of the side is only 7, economically the country is doing better than most at this time.

We prepared this before the competition started. We will review after the competition is finished. The model would suggest that although Spain and Italy have excellent quality sides, they should under-perform on this occasion.

Previous winners Greece, Spain and Denmark both won when their economies were boom ing - based on this prediction, these countries will bomb out.

ing - based on this prediction, these countries will bomb out.

Okay, we are more likely to be wrong than right, and we certainly would not advise you bet money on this model - we are not - we prefer to invest instead (don't believe in risky "bets" against bookies where the odds are stacked against you).

Waynes Hair And His Performance: Only other comment is our theory that Wayne Rooney plays best when he has a full head of hair. When he was 18 - lots of hair, he was sensational. He slowly went down hill until he got his hair transplant mid 2011. He then had a super period before it started going wrong - falling out again. He's had a bit of a style job in the last few days, so hopefully if we qualify he will play a bit better. But our prediction is, he will start a slow decent downwards henceforth as his hair falls out further culminating in retirement when he is finally bald. He's tried to delay the inevitable, but time it catching up. We say shave it at this point, but alas, he shows every sign of an undignified decline with his first transplant by age 24.

Anyway, let's see what happens!

Economic

Quality

Muliplier

Total

Germany

9

10

90

19

Netherlands

7

8

56

15

England

7

7

49

14

Sweden

9

5

45

14

France

5

8

40

13

Russia

7

5

35

12

Denmark

7

5

35

12

Italy

3

10

30

13

Poland

6

4

24

10

Czech

6

4

24

10

Portugal

3

8

24

11

Spain

2

10

20

12

Croatia

6

3

18

9

Ukraine

6

3

18

9

Rep of Ireland

2

3

6

5

Greece

1

4

4

5

Ukraine and Poland home advantage not taken into consideration