449: The drugged patient is showing signs of life

10-18-2012

PropertyInvesting.net team

![]()

Improvement? Things have been pointing to a global economic improvement lately a rather warmer feeling coming from all directions as the global economy looks to be stabilizing and improving. But dont be sucked into, otherwise you will be hit by a sucker punch.

Mini-Boom: Lets explain. Firstly these indicators are not surprizing - we always anticipated a mini-boom by October strategically timed perfectly for President Obamas re-election campaign. Just enough to get the controlling incumbent back into power. Its been a brilliantly designed smoke and mirrors game. It should be just enough to get President Obama re-elected.

Seasonal Aspect: The other thing is - the economy always picks up in the northern hemisphere in October because people consuming more energy, food, travel and they are back at work being  productive. The numbers are just reflecting seasonal aspects. This pattern has become more pronounced in recent years because transient workers go home and spend long periods on holiday in the summer productivity slips and crises break out. People down tools and go on holiday and everyone produce less. Turbulence comes between May and September as the global elite that make decisions put their feet up on expensive boats in the Med, Florida and Caribbean. As the weather gets colder, the western economies improve.

productive. The numbers are just reflecting seasonal aspects. This pattern has become more pronounced in recent years because transient workers go home and spend long periods on holiday in the summer productivity slips and crises break out. People down tools and go on holiday and everyone produce less. Turbulence comes between May and September as the global elite that make decisions put their feet up on expensive boats in the Med, Florida and Caribbean. As the weather gets colder, the western economies improve.

Under-Employed: US unemployment is claimed to be 8%. But 33% of the population is in part time work or poorly paid work the type of work that is far under what they would normally do. Hence real under-employment is more like 38%. 33% of the US working population earn less than $20,000 a year not really enough to live on. The grey boundary between unemployed and under-employed gets greyer by the year.

Recession: US GDP is claimed to be rising at 1.6% and inflation at 2.5%. However, it is our strong belief that inflation is running at more like 6% and hence GDP growth is more like minus -1.9%. Why to government take out energy and housing costs from their inflation calculations? Yes, its a pretty severe recession. The US is in decline, not in growth. These numbers are all part of a ploy by government to give the illusion of growth. If they can claim low inflation, then GDP goes up. As peoples standards of living decline because this happens slowly through stealth the dumbed down populations become ever more reliant on big government and hand-outs and are then more likely to vote for their leaders. Big business stays out of the way because they can still make money in inflationary times or deflationary times.

Real Estate Bubble: The current new policy of using printed money to buy mortgage backed securities (e.g. bad mortgage debt) is an attempt to prop up the real estate market in fact create a mini real estate boom rising asset prices to make people feel better off so they borrow more money and spend more money. But this is exactly the same policy that created the US real estate bubble between 2002 and early 2007. The Fed has learnt no lessons. It is creating a mini bubble manipulating the real estate market with fiat printed money - and it will only end in tears. Indeed, we predict US real estate prices will move higher for a few more months adding to the eight moves so far being propped up by this new money, but they will head down again when the 2013-2014 crash happens.

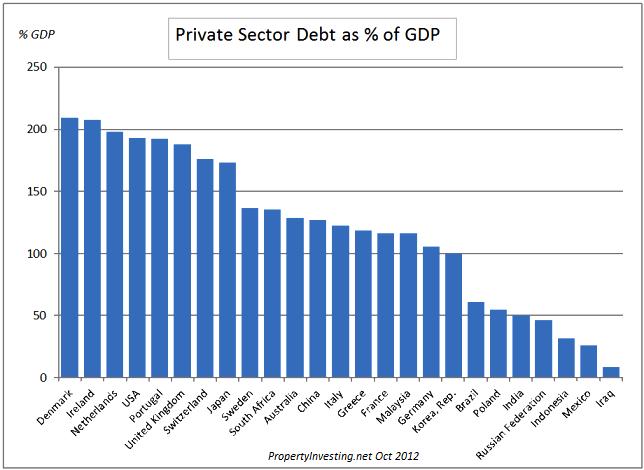

US Debt: The US private sector debt is a gigantic $42 Trillion. A healthy level is half this at $21 Trillion. Prices would need to drop by 50% adjusting for inflation. Now you can see that pumping $3 Trillion of money into the US economy as the Fed has done in the last 4 years will not have a large impact on this debt - propping it up, simply because it is so high. It will delay the day the actual deleveraging takes place. This implies stock prices and property prices will drop or inflation will rise sharply and catch up. We'll either have deflation or inflation until the deleveraging is complete. This deleveraging will also happen because the baby-boomers are starting to spend less and invest less. Real growth is slow and will remain slow for years in western developed nations such as the USA and UK. Well have to wait until 2022 for the echo-boomers to start driving things forward again.

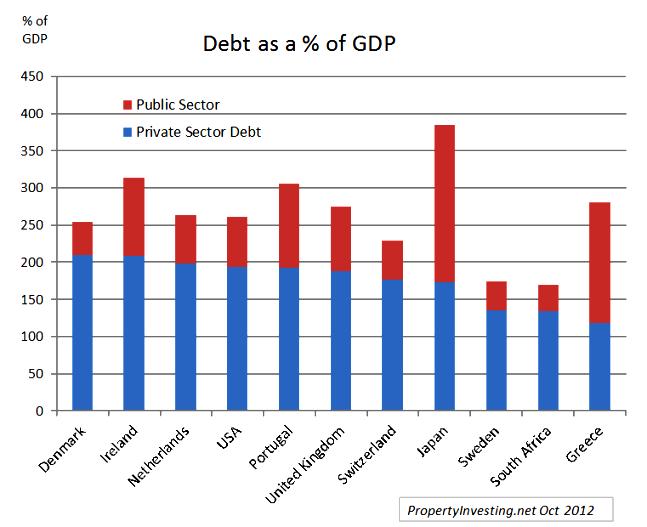

Japanese Crisis: When one looks at the combined private sector and public sector debts, their situation is grave. The 1990 stock market crash and real estate bubble that went pop was followed by years of deflation and government intervention to prop up failed banks - sound familiar? The trigger for this crash was the babyboomers that were born 1920-1930 retiring and spending less by the early 1990s. No amount of stimulus helped. People hoarded cash - interest rates at zero did not help. This has started to happen in the USA now - with affects also being felt in the UK. An extreme version of this is now being felt in Spain, Italy and Greece - all countries that had fertility rates of as low as 1 child per two adults by the year 2000.

Creating Bubbles: If one looks back over the last forty years, the babyboomer years of 1945 to 1963 - with mid-point 1956 had their peak spending when they were 45 to 50 years old - say 47 years old. So if you take 1956 and add 47 years, you get to 2004, then the spending drops. The boom years were up to  2000 - culminating in the high-tech bubble that burst March 2000. The Fed made a gigantic mistake by inflating a US real estate bubble in 2002 with ultra-low interest rates to try and kick-start the deleveraging economy. This caused borrowing on property to double from 2002 to 2007 in five years. Borrowing multiples rose from 3.5 in 2000 to as much as 9.5 time earnings by 2006. This was inflating a real estate bubble that should never have been inflated - and the USA has been suffering ever since. This private sector debt and bad loans are so huge that the Fed printed $3 Trillion to try and keep the show on the road. But it will lead to a crash almost certainly next year. The patient is weak and is about to have a heart-attack.

2000 - culminating in the high-tech bubble that burst March 2000. The Fed made a gigantic mistake by inflating a US real estate bubble in 2002 with ultra-low interest rates to try and kick-start the deleveraging economy. This caused borrowing on property to double from 2002 to 2007 in five years. Borrowing multiples rose from 3.5 in 2000 to as much as 9.5 time earnings by 2006. This was inflating a real estate bubble that should never have been inflated - and the USA has been suffering ever since. This private sector debt and bad loans are so huge that the Fed printed $3 Trillion to try and keep the show on the road. But it will lead to a crash almost certainly next year. The patient is weak and is about to have a heart-attack.

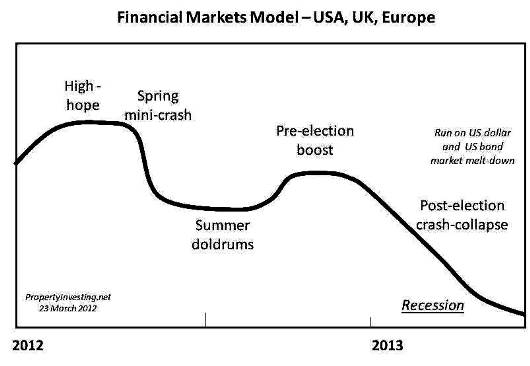

Bubbles: This particular bubble is rather different than the last ones - because its a stock market bubble, bond bubble and commodities bubble all in one - created by speculative cheap money from the Feds money printing activities. One, two or all three of these will pop shortly when the USA sinks into recession after the Nov 2012 US Election spending binge ends end 2012.

Dollar Drug: Yes, $45 Billion a month of printing (Twist) was not enough for the patient, so the Fed chose to add another $40 Billion a month open ended (QE3). The current symptoms of the patient after  a six weeks of doubling the dollar money drug infusion is the patient is starting to feel better. A bit giddy, but a little euphoria is coming back. But the patient who has been overdosing on dollars for years, it about to collapse with a heart attack - in 2013. The addiction to dollars is extreme. But this last dollar drug infusion wont make much difference to stimulate the patient any more. The patient is almost dead. It could create some spasms. But death is almost assured.

a six weeks of doubling the dollar money drug infusion is the patient is starting to feel better. A bit giddy, but a little euphoria is coming back. But the patient who has been overdosing on dollars for years, it about to collapse with a heart attack - in 2013. The addiction to dollars is extreme. But this last dollar drug infusion wont make much difference to stimulate the patient any more. The patient is almost dead. It could create some spasms. But death is almost assured.

$3 Trillion Binge: During President Obamas tenure, $3 Trillion has been printed to prop up the debt and mortgage markets but this has failed to get the economy moving and the claimed unemployment has stayed the same, but real under-employment has sky-rocketted. A key number is the people using food stamps its a massive 46 million people. Yes, 46 million people are so desperate they need stamps for food. In the Great Depression of the 1930s, far less people queued at soup kitchens. Today, the more humane less embarrassing method of feeding the poor is through food stamps. And the big supermarkets like it as well. Only 28 million people used food stamps in 2008 at the peak of the recession. Why do people think the US has grown when food stamp usage has almost doubled?

Trauma: The US economy is in really bad shape:

· The US direct debt is $16.2 Trillion

· The total US unfunded liabilities including Medicaid, Medicare and Military is $75 Trillion

· The annual US deficit is $1.25 Trillion

· US tax receipts are $1.75 Trillion

· US government spending is $3 Trillion

· Private sector debt is a colossal $42 Trillion

· 40% of government spending is borrowed money (only 60% if from tax receipts)

· The military-industrial complex is aging, expensive and can no longer be funded with gigantic borrowing

· Government money printing is pumping up stocks but in true inflation adjusted terms, there is no value creation the stock market has been in a bear market since March 2000

· The US relies on historic goodwill to use the dollar as the global reserves currency. Without this status, the dollar would decline by 33% in value and import prices would rocket 33%.

Double the Printing: The Fed has recently doubled the amount of money printing from $45 billion of US  Treasury bonds a month to $95 billion of US Treasury bonds and Mortgage Backed Securities. This means Operations Twist has now been joined with QE3 or QE infinity open ended. That means $1.1 Trillion is now printed each year to inflate and debased the currency. Considering the economy is only $15 Trillion in all transactions made, this is about 7.5% of GDP a gigantic amount of money. If this doesnt create a mini-boom and shot in the arm, we dont know what will. Thats like giving every person in the US $3333 cash a year. Or a family of four this means $13,333 a year in printed new cash. But of course, we know this does not go to the average person instead it goes to the banks when then speculate/invest with it.

Treasury bonds a month to $95 billion of US Treasury bonds and Mortgage Backed Securities. This means Operations Twist has now been joined with QE3 or QE infinity open ended. That means $1.1 Trillion is now printed each year to inflate and debased the currency. Considering the economy is only $15 Trillion in all transactions made, this is about 7.5% of GDP a gigantic amount of money. If this doesnt create a mini-boom and shot in the arm, we dont know what will. Thats like giving every person in the US $3333 cash a year. Or a family of four this means $13,333 a year in printed new cash. But of course, we know this does not go to the average person instead it goes to the banks when then speculate/invest with it.

Inflation: There are many people that seem to believe this money printing will not lead to inflation. Let us make one thing totally clear. By definition this IS inflation. Printing money is inflation - period. What we think a symptom should and will be is rising prices across the board. But some prices will rise far faster than other. The fastest growing prices are likely to be:

· Food

· Fuel (oil)

· Super-rich property (high end)

· Farmland (good quality, non-drought)

· Gold and silver

Poorer and Super-Rich: The very people this money printing is reported to be helping will actually be nobbled by it. The poor will get poorer because they proportionally spend the most money on food and  fuel. The rich will undoubtedly get richer because upper end real estate prices will rise, stocks markets could rise a bit, and oil, gold and silver prices will sky-rocket. These are assets owned by the super-rich. Hence this Keynesian Socialist money printing policy will drive debt levels higher, inflation higher, the poor into food stamps and the super-rich into a commodities related speculative high return frenzy. Its an accident waiting to happen. But the smart rich people can see it coming. So they are and will position themselves to take advantage of the government regulations and policies that drive this cheap money speculative commodities frenzy.

fuel. The rich will undoubtedly get richer because upper end real estate prices will rise, stocks markets could rise a bit, and oil, gold and silver prices will sky-rocket. These are assets owned by the super-rich. Hence this Keynesian Socialist money printing policy will drive debt levels higher, inflation higher, the poor into food stamps and the super-rich into a commodities related speculative high return frenzy. Its an accident waiting to happen. But the smart rich people can see it coming. So they are and will position themselves to take advantage of the government regulations and policies that drive this cheap money speculative commodities frenzy.

Food Stamps: Since President Obama came to power 4 years ago, despite $3 Trillion of money printing and socialist policies designed to help the poor, the number of people using food stamps has sky-rocketted from 28 million to 46 million people. Yes, thats the population of England on food stamps in the USA. Considering there are only 350 million people, many under the age of 16, thats a large proportion of people on food stamps. This is during a period of so called growth - frankly, its a miserable statistic that does not bode well for 2013 when the real slump occurs.

Positioning: So as we have been advising for well over a year now, you should be positioning for a crash in 2013. This is the end of a bubble a boom a growth period in western developed nations not the start. It was a sort of phantom 5 year growth period that never was before the next down-leg. The stock market is now looking like a mild bubble in the USA and UK. It should crash when a recession becomes clear again. Whenever the Fed starts printing, other countries start keeping up with the declining dollar. It becomes a game. Its a race to the bottom. An unofficial currency war. Unless Ben Bernanke is fired money printing in the world will continue at a grand pace and inflation will hit new highs in 2013 more or less at the time of a crash.

Market Distortion: The Fed has kept interest rates at close to zero per cent, and is buying about 75%  of its own bonds or debt offerings. It is able to do this because the dollar is relatively strong because its viewed up until now as a safe haven and it is the global reserve currency of the world. The low inflation, low interest rates, unattractive alternative investments and stable dollar make bonds attractive - hence bond rates are also low. However, this benign situation is very unstable. It only needs the Fed to raise interest rates because of inflation or a decline in the dollar for there to be a run away from bonds - a bond market crash. This could happen with another US downgrade or a confidence crisis in the US economy - e.g. a recession and/or problems with the early 2013 fiscal cliff. We think the risks of the whole bond market becoming extremely unstable in 2013 is high. It just needs a recession - and revised forecasts demonstrating the USA's inability to pay back it's debts. This $65 Trillion wall of bond money would hit the market and cause massive inflation as the dollar declined and import costs rose. This switch away from US bonds would cause chaos - we think its likely to happen in 2013-2014. Even the biggest US bond bull of them all Bill Gross is shifting into gold.

of its own bonds or debt offerings. It is able to do this because the dollar is relatively strong because its viewed up until now as a safe haven and it is the global reserve currency of the world. The low inflation, low interest rates, unattractive alternative investments and stable dollar make bonds attractive - hence bond rates are also low. However, this benign situation is very unstable. It only needs the Fed to raise interest rates because of inflation or a decline in the dollar for there to be a run away from bonds - a bond market crash. This could happen with another US downgrade or a confidence crisis in the US economy - e.g. a recession and/or problems with the early 2013 fiscal cliff. We think the risks of the whole bond market becoming extremely unstable in 2013 is high. It just needs a recession - and revised forecasts demonstrating the USA's inability to pay back it's debts. This $65 Trillion wall of bond money would hit the market and cause massive inflation as the dollar declined and import costs rose. This switch away from US bonds would cause chaos - we think its likely to happen in 2013-2014. Even the biggest US bond bull of them all Bill Gross is shifting into gold.

Printing Is Pivotal: We have been writing about money printing in the USA for a while now and frankly it is such a pivotal and important aspect of global and national economics that its worth serious analysis. These dollars go to every corner of the earth and cause bubbles and distortions in the market. The Fed is running the world economy with its actions and money printing policy probably to help the private global elite. They work in concert with Wall Street. You may have noticed how Wall Street bankers never c omplain about President Obama. The reason in our minds is clear. They like the money printing and know it heads into their bank accounts most of it never even gets to the middle classes never mind the poor. The cheap money is used first and foremost to place risky bets and speculate or invest to try and win high returns. That is what bankers are paid to do. Use cheap money, lend it out at a high rate and invest to make high returns. If you give $3 Trillion to Wall Street bankers what else can you expect? If Helicopter Ben has given a lump sum to each family they would have got $40,000 each (or $20,000 for each tax payer). It would have wiped most personal debt away outright.

omplain about President Obama. The reason in our minds is clear. They like the money printing and know it heads into their bank accounts most of it never even gets to the middle classes never mind the poor. The cheap money is used first and foremost to place risky bets and speculate or invest to try and win high returns. That is what bankers are paid to do. Use cheap money, lend it out at a high rate and invest to make high returns. If you give $3 Trillion to Wall Street bankers what else can you expect? If Helicopter Ben has given a lump sum to each family they would have got $40,000 each (or $20,000 for each tax payer). It would have wiped most personal debt away outright.

Instead most of it has been lost by bankers over the last 3 years though these banker keep awarding themselves record bonuses regardless of performance.

Savers Destroyed: Just to put this into perspective, the Fed issues cash at 0.5% rate. This is then lent out to private individuals at 5% (4.5% per annum profit). It is lent to businesses at 7% (6.5% profit per annum). It is lent out for credit card holders at 15% (14.5% per annum profit). Meanwhile savers get 0.5%. Inflation is claimed to be 2.5% - but it is really 6+%. Savers lose 5.5% a year. This also goes to the bankers. They use this money to lend to people at 5-15% rates. Can you see now how the odds are stacked against savers and the poor, and made easy for bankers investing in high return commodities and lending to the people and small businesses? It is the same in the UK and USA there is barely any difference. This model just operates on a smaller scale. The UK has about seven times smaller economy but the ratios are very similar and monetary policy is also very similar (zero rates, money printing, bankers lending at high rates, negative savings rates).

Oil Price: If there is any good news around, its the increase in US oil production and gas production from drilling onshore oil shale and shale gas deposits - mainly in North Dakota, Texas and Louisiana. The US new produces 83% of its total energy needs though it still imports oil to the cost of $350 billion a year. If only the US could wean itself off this last 13% of energy - the 8 million barrels/day of imported crude oil it would be totally energy independent. These new supplies, along with those from Iraq and Canada have led to a fairly well supplied oil market. It will remain turbulent though. The cost of extracting these marginal barrels of oil from shale, oil sands and deepwater is about $80/bbls - so oil is not likely to drop much below $90/bbl for any extended period. The price upside is large if a war breaks out. Overall we expect it to remain erratic, generally range bound between $115/bbl and $90/bbl with a slightly rising trend partly caused by money printing. But dont be surprized to see a spike to $200/bbl for a few weeks or a drop to $70/bbl for a month or so if war or financial crisis hits the markets. Any oil price above $125/bbl leads to recession in western oil importing nations (e.g. Greece, Italy, Spain, Ireland, Portugal). Any oil price below $80/bbl would imply a financial crisis and recession. Range bound equals stagflation in these countries. Overall, the end of cheap oil and excessive money printing means its difficult for western developed nations to get themselves out of recession and have any sustainable growth - especially with the aging populations.

Babyboomers: The USA and UK still seem to think that the economy will improve and start looking like it did in 2002. But this is not going to happen. The reason as we have been writing about for the last eight  years is the babyboomers, particularly in the USA. When people reach 50 years old, their spending habits change dramatically. They start saving far more and spending far less. Their kids fly. They hunker down. They look forward to retirement. So no amount of money printing and low rates will shift the economy into the high consumer spending period of before simply because these babyboomers dont buy stuff any more. No new big cars. No expensive family holidays and ski trips. No shopping for five people at Tesco or Walmart. They downsize their homes. They cut down on fuel, electricity, heating, water, sewage, garbage everything. They save and slow consumption.

years is the babyboomers, particularly in the USA. When people reach 50 years old, their spending habits change dramatically. They start saving far more and spending far less. Their kids fly. They hunker down. They look forward to retirement. So no amount of money printing and low rates will shift the economy into the high consumer spending period of before simply because these babyboomers dont buy stuff any more. No new big cars. No expensive family holidays and ski trips. No shopping for five people at Tesco or Walmart. They downsize their homes. They cut down on fuel, electricity, heating, water, sewage, garbage everything. They save and slow consumption.

Declining Consumption: What we have been seeing since 2000 is the slowing of consumption because of the aging western populations particularly in the USA. US oil consumption has dropped 20% since peaking in 2006. Its been in decline for years in Germany. Ditto the UK. People travel less and save more. The money printing on a grand scale is trying to get people to spend. But they wont. It never happened in Japan in the 1990s and it wont happen in the USA 20 years later. Look at Italy a declining and aging population see the spending dropping, oil consumption dropping and economic activity has been stagnant for years now. Any wander with so many retired people and so few young families. A birth rate of 1.2 in 2002 and low immigration is stored up a huge problem for Italy in the next ten years. Not enough young people and too many old people.

Gold and Silver: This brings us onto gold and silver. Gold is perfect when panic sets in. Silver is not good when panic sets in its better with high inflation, growth and booming manufacturing. Gold can skyrocket with inflation or deflation. Silver will skyrocket with inflation. Gold has lost a little of its lustre in the last few weeks as it appears things have stabilized. But we think this is just temporary. Its taking another breather.

Gold and Silver: This brings us onto gold and silver. Gold is perfect when panic sets in. Silver is not good when panic sets in its better with high inflation, growth and booming manufacturing. Gold can skyrocket with inflation or deflation. Silver will skyrocket with inflation. Gold has lost a little of its lustre in the last few weeks as it appears things have stabilized. But we think this is just temporary. Its taking another breather.

When the proverbial **** hits the fan in 2013 gold will skyrocket. Silver will likely follow suit.

No Bubble Yet: For all those people that think gold is in a bubble we say you are wrong, wrong, wrong. To explain:

· The cost of extracting gold has skyrocketed to $800-1000/ounce to launch a new project it might cost $1200/ounce including exploration, hence the floor for gold must be around $1200/ounce

· Mining stocks are depressed, these beaten down companies are finding it difficult to raise finance for new projects because of high risks and hence production is very unlikely to increase. Despite an eight fold increase in gold price, production has barely increased.

· Miners strikes, nationalisation, high taxes, higher energy costs and unrest are lowering gold production particularly in South Africa

· The quality of gold ore is declining with no new large finds its a dirty business with high costs and no new large projects slated

· Annual gold production is adding about 1.5% to world reserves each year however, the amount per person is dropping because the global population and GDP is rising faster than 1.5% per annum

· Because of high underlying supply costs and moderate demand, zero euphoria and dumbed down mining stock prices, its difficult to see any evidence the gold price in dollar terms is in a bubble

Gold as a percentage of fund managers asset allocation in running at about 0.8% - a tiny proportion. If this rose to 8%, one would expect a ten-fold increase in price. Even if during a panic fund managers switched and the 0.8% conservatively rose to 2.5%, this would still imply a fourfold increase in gold price to $7000/ounce.

Gold as a percentage of fund managers asset allocation in running at about 0.8% - a tiny proportion. If this rose to 8%, one would expect a ten-fold increase in price. Even if during a panic fund managers switched and the 0.8% conservatively rose to 2.5%, this would still imply a fourfold increase in gold price to $7000/ounce.

Only 1% of the worlds investors own any gold. This is also a tiny fraction. Only when 5-10% of investors own gold will there be any sort of bubble forming. With the current fiat currency system where 100% of investors own currency, the only real money is physical gold. When the general population realises this, gold and silver prices will skyrocket just like they did in the last panic early 1980 33 years ago.

It looks most likely panic will set in just after the US Elections early 2013 when:

· US spending cuts kick in

· US tax increases kick in

· US election spending declines

· Money printing accelerates

· US interest rates start rising

· Inflation starts rising

· A US recession begins

· War breaks out in the Middle East

· Oil prices temporarily skyrocket before crashing

Deluded: Central banks are quietly buying gold as much as they can before the crisis. Wall Street bankers either know the crisis is close ready to bail out and head for the hills or are deluded or in denial. Their job is to sell financial products and its not easy to tell people to bail out of dollar financial products and currency if you are a Wall Street banker.

Panic and Crisis: So use the current mini-boom as an opportunity to get out of government bonds, treasuries and get into gold, silver and oil. Bonds will crash, gold will sky-rocket. But be prepared for an  oil price spike and be prepared to get out quickly as well. As for gold, as panic spreads in 2013 gold will simply go skyrocketing upwards to places dreams are made of for owners of the physical gold. Throughout history, gold has been the only asset that has held its true value - for hundreds of years. A gold coin bought a top quality suit in 1700 and it still does today. But the US dollar is only worth 3% of its 1920 value in real terms purchasing power. As low interest rates, high inflation, negative rates and panic set in in 2013 with gold mining supply problems gold is set to skyrocket in dollar terms as the dollar declines and fiat currencies degenerate into close to worthless paper instruments. Debts will be deflated away at a faster pace before a likely big re-set takes place sometime in the next 5-10 years.

oil price spike and be prepared to get out quickly as well. As for gold, as panic spreads in 2013 gold will simply go skyrocketing upwards to places dreams are made of for owners of the physical gold. Throughout history, gold has been the only asset that has held its true value - for hundreds of years. A gold coin bought a top quality suit in 1700 and it still does today. But the US dollar is only worth 3% of its 1920 value in real terms purchasing power. As low interest rates, high inflation, negative rates and panic set in in 2013 with gold mining supply problems gold is set to skyrocket in dollar terms as the dollar declines and fiat currencies degenerate into close to worthless paper instruments. Debts will be deflated away at a faster pace before a likely big re-set takes place sometime in the next 5-10 years.

So enjoy the calm before the storm. The drug induced euphoria is about to turn into cold turkey. The patient is now on permanent life support drug infusion - open ended - comatose. Doctors prognosis is grim with death projected in 2013.

We hope this guidance has been helpful. If you have any comments or questions, please contact us on enquiries@propertyinvesting.net