451: Dollar About To Crash As Recession Starts

11-11-2012

PropertyInvesting.net team

Obama Win: No surprize then that Obama was re-elected with a reasonable majority as we predicted. This was always likely to happen for a number of reasons:

· So many people are reliant on the state for benefits, food stamps, unemployment benefits and social hand-outs

· Increasing immigration the large and expanding Hispanic vote

· Obama is particularly popular with women (the Republican tend to be unpopular with women)

· Expanded public sector and government more likely to vote for big spending Democrats

Outside the USA, it seems Obama and the Democrats were far more popular than the Republicans.

Republican Disappointment: It must be a huge disappointment for Republicans to lose an election where the economy is such a plundering mess, the outlook so bleak and unemployment so high. They could not get their message or a good enough message across it seems. Anyway, we have a new Democratic government installed another four years of Obama.

So what does this mean for investors? Some obvious pointers:

· The Fed Chairman will continue his money printing ways for another four year term - interest rates might stay low for a while before getting out of control during the predicted crisis in 2013-2014

· Markets will continue to be grossly manipulated by big government interference.

· Wall Street bankers will continue to prosper for a while longer using the cheap printed money to speculate and driving up commodities prices.

· Gold and silver prices will go ballistic eventually as panic sets in.

· The bond market will pop, gold skyrocket when the crisis breaks out. Half of Americans pay no federal tax and 46 million use food stamps (up from 26 million in 2008). The tax receipts arent enough to pay the interest on the debts. The USA will eventually have to default and/or hyper-inflate, and people with savings in dollars will be destroyed.

Oil and Shale Gas Boom: The big positive over the last five years has been the oil and gas business. It started in 2004 with fraccing of shale gas deposits onshore in the USA. This technology created a boom in gas production after years of natural gas declines production started to increase in 2007. It surprized almost everyone. It sent gas prices shooting down from $12/mmbtu in 2007 to $2.5/mmbtu in 2010 because of the flood of cheap gas, one seventh of the cost. Then the same horizontal drilling and multiple fraccing technology has been used in oil shales deposits to extract oil and wet gas onshore in the USA opening up vast new economic oil reserve. North Dakota has seen the biggest oil boom of any state its oil production rose 35% last year alone. The USA reversed its oil production declines and now produces as much oil as it did in 1994. The USA produces more combined oil and gas as it did in 1991. A remarkable achievement considering the challenges of drilling offshore after the Macondo Gulf of Mexico disaster.

Target Energy Self Sufficiency: When one considers the coal, nuclear, gas, oil and renewable energy production, the USA now produces 83% of its energy needs. Its just about possible the USA could produce all of its energy needs by 2020 if the development of the oil shale across large areas of the USA is kept at its current growth rate. The boom started with the Bakken Oil Shale deposits mainly in North Dakota and NW Wyoming and also similar deposits in Texas and NW Louisiana the Eagle Ford etc.

These states are solid Republican areas that tend to support the oil-energy industries the historical areas where drilling has been the most intense and most of the energy employment has been created over the last 100 years. One of the big US issues has been the countrys gigantic oil imports totalling $350 Billion per annum at $100/bbl oil. But these are likely to drop now because:

-

The US economy is so weak, employment has stayed weak and manufacturing has suffered so much that oil consumption has been in decline for many years since 2006

-

High oil prices have stimulated a boom in oil shale drilling and fraccing driving up indigenous supplies.

Reliance On Others: So its partly good news more US oil and less reliance on imports from some unfriendly neighbours. Partly bad news the consumption is dropping because of the weak economy. If oil prices stay high and the economy crashes into a recession as we think this is very likely in 2013 2014, then the speed by which oil production rises and consumption falls could accelerate, making the USA economy independent even sooner than 2020.

Obama Likely Also To Win In 2016: This underlying trend is one reason why Obama might find it easier to retain power also after 2016. If unemployment rises, social welfare increases and oil production increases to help pay for these social programmes then the Democrats are likely to get re-elected in 2016 as well. The shear size of the public sector then, plus the womens vote and Hispanic vote make the likelihood of a Republican win in 2016 low we think. By then, the USA will have a different feel and flavour. The babyboomer might also be relying on the Democrats for hand-outs as well and many private enterprizes and entrepreneurs will have fled the USA to countries with greater opportunities.

So what does this mean for investors? We really dont think any meaningful spending reduction programmes will be agreed. The deficit is already too high, in a dire state and government spending is out of control. We think the deficit will continue to rise because almost none of the politicians have the guts or heart to tackle it. Money printing will pay for the deficit spending and bond purchases. The dollar will be depreciated. But other global na tions will be playing the same tricks, as they have since the 2008 crash. Its a race to the bottom as all major industrial nations are now money printing on a grand scale to prevent deflation (counteracting deleverage).

tions will be playing the same tricks, as they have since the 2008 crash. Its a race to the bottom as all major industrial nations are now money printing on a grand scale to prevent deflation (counteracting deleverage).

Falling Like A Pack Of Cards: Each debt ridden country is falling like a pack of cards the weakest fall the first. We had Greece, Ireland, now Spain, next it will be Italy, then the mother of them all the USA. At the moment, its quite ridiculous that the US is able to print money and sell Treasuries/Bonds offer them for yields of a meagre 1.6%. There is no way these investors will get their money back. They are under an illusion that the USA is a safe haven. Its not because the USA has no fiscal responsibility, spending reduction plan and prints money to expand social programmes and the size of the government. Its a very unstable situation. The only thing we can think of that might support this safe haven status is the military and petrodollar status more of this later.

Doubling Of Gold Again: Since Obama got into power in 2008, $3 Trillion has been printed and the gold prices have doubled from $850/ounce to $1700/ounce. The open ended QE3 and Operation Twist are pumping $90 Billion a month into the economy. Thats $1 Trillion a year. We therefore conservatively think that gold prices should double again on an expectation basis in the next 3 years e.g. to something like $3400/ounce. This is just to keep up with the money printing.

The US economy is in a pretty dire situation with a deficit of 8.5% of GDP, direct borrowing of $16 Trillion, GDP of $16 Trillion and unfunded liabilities (promises of social spending, healthcare and military) of $60 Trillion. The deficit is >$1.2 Trillion. It seems the Feds only strategy is to continue pumping money into the private banks to keep them afloat. The Fed can more or less do what it wants its a private bank helping its private banking chums in Wall Street to stay afloat and/or pay themselves large bonuses. These banking elite only seem to have one goal in life to cream as much money out of the system for themselves as possible in  the shortest space of time.

the shortest space of time.

One can just sit there and watch this happen, or position oneself with ones investment portfolio to make sure we are not caught out by what will happen in 2013 and 2014.

Dollar Criticality: So why is the USA so important to watch for investors? The world economy is now truly a global one. They used to say if the USA sneezed the world caught a cold. Its still true today. The USA is 25% of global GDP although only 5% of the global population. It consumes 30% of the worlds hydrocarbons. The Fed has been printing money and exporting its dollars because the dollar is still the reserve currency of the world. The world is flooded with them. They create bubbles all around the world. There are a few reasons for this reserve currency status:

· The dollar is the world petrocurrency almost all oil is bought and sold in dollars

· The USA has 250 military bases around the world acts as the policeman of the world to secure oil, trade routes and shipping this bolsters its kudos and ability to retain the dollar as the global reserve currency

But these facets are both under threat firstly some countries are starting to challenge the US dollar as the petrocurrency. An example is that Russia and China struck a bi-lateral deal recently to buy oil in their local currencies. This is something that really upsets the American administration because their economic prosperity is so dependent on the dollar being the worlds petrocurrency. Take this away and living standards would decline by 25% or more in part because money printing to pay for debt would have to stop.

Secondly, the USA can no longer afford to maintain 250 military bases around the world it costs a total of $1 Trillion a year or  7.5% of GDP. As long as the Fed can keep printing money to pay for the military, its probably just about sustainable, but its now getting very close to a tipping point. It only needs the USA to dip into a recession and the dollar to decline sharply to put severe pressure on the industrial-military complex that has been built up over the last 60 years since WWII.

7.5% of GDP. As long as the Fed can keep printing money to pay for the military, its probably just about sustainable, but its now getting very close to a tipping point. It only needs the USA to dip into a recession and the dollar to decline sharply to put severe pressure on the industrial-military complex that has been built up over the last 60 years since WWII.

These two facets to the US economy are probably its Achilles heel. It only takes a severe recession meaning the US looking increasingly unlikely to pay back its debts then pressure will build on the US as a global reserve currency. At this point international investors could desert the bond markets, meaning more money printing would crash the US dollar value then bond rates would rise sharply along with interest rates. The market would take over. No amount of Fed manipulation would help. Then private investors, individuals, state and government would feel the full force of higher interest rates then the economy would implode.

What we are saying is the days of the USA being able to print money, keep interest rates low and keep the dollar value high with bond yields low is coming to an end. This situation looks stable, but its highly unstable. It only needs a recession to tip the whole lot over and cause a vicious circle and economic meltdown like we have seen in Greece. But unlike smaller countries there is no-one big enough to bail the USA out. The only good news is the increasing oil production and declining oil consumption. But if oil prices drop and indigenous oil production also declines again because of this, this could create added pressures on top.

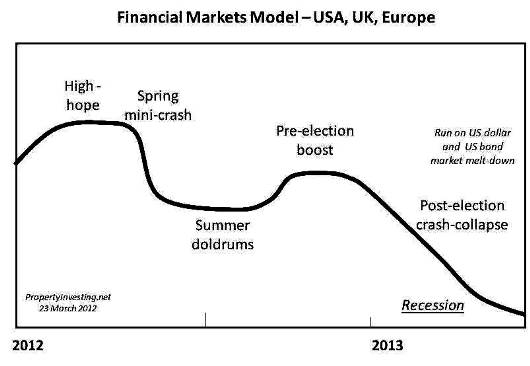

Economy Due For Recession: Lets consider 2012 before we discuss 2013. Even with massive government spending programmes, $90 Billion a month money printing, interest rates at zero % and pre-election boom with tax cuts, food stamps and hand-outs, unemployment stayed at 7.9% and the economy grew a meagre 2% (or declined -1% if you take into account the real inflation rates). With the current Administration in power, our view is it cannot get any better than it is today. Thats it. We have had the so called recovery. Its been five years since the last so called recession. Though in a way, the USA has been in a recession (or stagflation) ever since then.

Now looking forwards into 2013 what we see is:

· The end of election boom spending

· The end of tax cuts start of tax increases

· Spending cuts

· Continued high oil prices

· Inflation rearing its ugly head with continued money printing on a grand scale

· Middle East instability and the Iran-Israel issue unresolved

Crash March 2013: By around March 2013, things will start to look particularly bleak as the Northern Hemisphere reduces GDP coming out of the winter months. You need to be well out of the stock market by then since its likely to drop 20% from now until mid-2013.

The only assets that will rise in price are:

· Gold

· Silver

· Artwork

Almost everything else will drop. Even oil prices could drop or gyrate wildly depending on what is happening in the Middle East.

The US is exporting inflation all around the world. They are leading the money printing. Other nations follow their example and print long side the USA to try and keep a pace with the depreciating dollar currency. The result is increasing food, commodities and energy-fuel prices. This particularly hits the poor since they spend such a high proportion of their income on food and fuel.

Great Desert Urban Societies: Pressures are building around the world. About 60 years ago, the Middle East was a vast desert with huge oil reserves, wealthy royal families and small desert town s. Populations in the desert nations have skyrocketed. Cairo was 1 million people in 1960. It is now 20 million people one of the largest cities in the world but in a desert. Oil production has remained fairly flat in the Middle East. Oil consumption has skyrocketed, Urbanisation and water usage has skyrocketed. We now have a situation where energy intensive cities and towns have been build all around desert areas that are totally unsustainable in the long term. As oil exports drop and oil usage continues to rise, along with these desert populations pressures and tensions will rise further and wars will break out. It is no coincidence that problems started in the Middle East after food and fuel prices sky-rocketted in 2008, then there was the economic crash, followed by more food inflation in 2011. Oil exports in Egypt, Tunisia, Yemen and Syria dried up meaning less money for social programmes then riots started and oligarchic regimes were overthrown. The disparity between the large oil/gas exporters such as Saudi, Qatar, UAE and Kuwait will likely rise and desert nations that import oil will go downhill into urban food and water poverty. Its hard enough eking out an existence forging around for food in lush climates like France, but in deserts its just not possible. You need clean water, food and shelter from the heat and sun all very energy intensive. A great desert urban society has been built and regrettably its foundations look very shaky.

s. Populations in the desert nations have skyrocketed. Cairo was 1 million people in 1960. It is now 20 million people one of the largest cities in the world but in a desert. Oil production has remained fairly flat in the Middle East. Oil consumption has skyrocketed, Urbanisation and water usage has skyrocketed. We now have a situation where energy intensive cities and towns have been build all around desert areas that are totally unsustainable in the long term. As oil exports drop and oil usage continues to rise, along with these desert populations pressures and tensions will rise further and wars will break out. It is no coincidence that problems started in the Middle East after food and fuel prices sky-rocketted in 2008, then there was the economic crash, followed by more food inflation in 2011. Oil exports in Egypt, Tunisia, Yemen and Syria dried up meaning less money for social programmes then riots started and oligarchic regimes were overthrown. The disparity between the large oil/gas exporters such as Saudi, Qatar, UAE and Kuwait will likely rise and desert nations that import oil will go downhill into urban food and water poverty. Its hard enough eking out an existence forging around for food in lush climates like France, but in deserts its just not possible. You need clean water, food and shelter from the heat and sun all very energy intensive. A great desert urban society has been built and regrettably its foundations look very shaky.

During the unstable period from 2013 onwards, it will be tough to find attractive countries to invest in. Resources rich countries with exports of oil, gas and minerals will do particularly well if their security and safety is good especially those with high standards of transparency, accounting and legal standards. The nations that have their currency backed by gold, minerals and oil/gas reserves will see their currencies strengthen and inflation stay subdued whilst GDP growth will be higher than average. These strong economies and currencies will see living standards rise and property prices along with them. Be careful with Australian property though since its looking like a bubble has formed that could pop if commodities prices drop sharply. Canada is another country where property prices look a bit toppy.

Countries on the Accent

· Norway oil/gas exports, natural resources, transparency, security, safety

· Australia oil/gas/coal/mineral exports, natural resources, transparency, security, safety

· Columbia - oil exports, improving security, crime levels and safety, booming economy

· Switzerland safe haven, gold reserves, tax haven, wealthy investors

· Canada oil/gas exports, minerals, transparency, safety, security

· China manufacturing growth, economic growth, exports

· Myanmar improving transparency, economy, start of boom

· Vietnam improvements after boom-bust, now back on the up exports, dynamic

· Sweden finance minister know how to control economy, smart people, transparent.