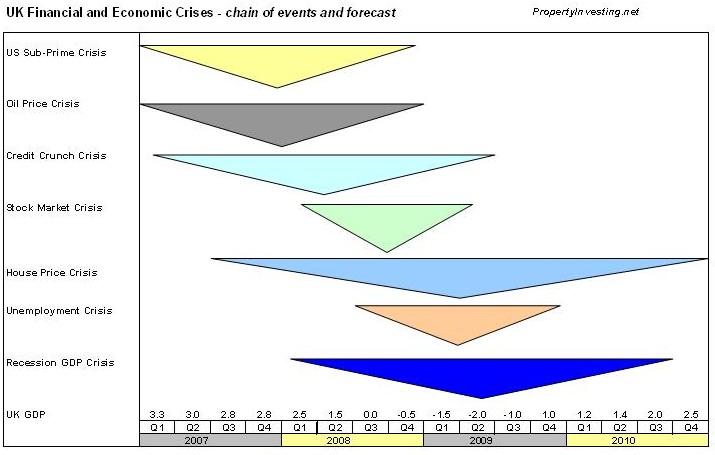

237: Inflation and interest rate forecasts - it's those oil prices again...

11-16-2008

PropertyInvesting.net team

We provide our latest forecasts on

We provide our latest forecasts on

- Oil prices have fallen very sharply from $147/bbl to $57/bbl.

- Shipping costs have crashed by more than 90% in some areas.

- Wheat prices have halved.

- Most stock markets are 35% down on early 2008 levels.

- Metals prices have shot down to about 50-60% of peak early 2008 levels.

If this does not feed into far lower inflation figures we will eat our hats!

We now expect

We now expect

In a few months time, the early November 2008 1.5% UK interest rate drop should start feeding through but we expect the bank to follow inflation down since its central target is to keep inflation at 2% or slightly below. If inflation gets to just above zero %, then the bank has a mandate to drop interest rates to zero without writing any letter of explanation to the Treasury. It is obliged to keep CPI inflation at ca. 2%. So do not be surprised to see mortgage rates come crashing down.

A typical variable rate tracker was about 7.8% early 2008. Rates have now dropped 2.25% - so the new variable rate should be about 5.5% to 6%. As interest rates drop to about 2%, then these variable rates should be about 2.25% above this level at 4.25%. So there is every possibility mortgage rates will drop to half the payment levels of early 2008 by around April 2009. The main fly in the ointment will be whether banks aggressively drop their rates competitively and dont cream off large tranches to pay back against poor debit conditions.

Its all doom and gloom at the moment the big question is, will new tax stimuli and far lower interest rates kick start the economies around the world then help support house prices. The expectation is that this should be good enough, but no-one really know whether it will work. So in summary, the

- Lower inflation

- Lower oil prices

- Lower interest rates

- Lower pound Sterling making exports more competitive

- Lower import costs

- Lower wage demands

- Slight rise in unemployment leading to efficiency improvements

Property prices will then be supported by the lack of building and mopping up of unsold stock. The massive lack of investment in residential building in the 2008 to 2009 period should sow the seeds for a housing supply crunch in 2010 to 2012 period, as the population continues to grow, no building takes place, more homes are needed and then the economy comes out of recession.

Property prices will then be supported by the lack of building and mopping up of unsold stock. The massive lack of investment in residential building in the 2008 to 2009 period should sow the seeds for a housing supply crunch in 2010 to 2012 period, as the population continues to grow, no building takes place, more homes are needed and then the economy comes out of recession.

In

But as we have warned before, watch out for the oil price. The current level of $57/bbl we believe is very low. It may stay down here for some time, but eventually it will rise again. We have already probably reached Peak Oil its just being masked by the demand destruction we have seen in the last six months. When oil prices rise again, the whole cycle will start to repeat itself. Oil is controlling the world economics. We believe it was the prime reason for the credit crunch for instance, in the USA, 5% of GDP was being spent on overseas oil imports at $125/bbl thats like a 5% tax or 5% royalty of the GDP/economy. No economy can reasonably handle this - as described in our special reports.

Is it any surprise the biggest oil importers as a proportion of GDP are now in a recession:

This is no coincidence we modeled this earlier this year. What we all learnt was that far from being able to handle the higher oil prices, it was merely being masked by the continued inflating economies, until the  banks finally showed us their books and there was no money left! It had all be spent on oil a massive transfer of wealth from western oil importing nation, to the oil exporting nations mainly in the Middle East, Russia, Norway, Venezuela and Canada. Now they have the cash dont expect them to come and help the hard pressed western economies theyll be too worried about the oil price crash and balancing their books in $60/bbl oil (rather than the $20/bbl they used in year 2000).

banks finally showed us their books and there was no money left! It had all be spent on oil a massive transfer of wealth from western oil importing nation, to the oil exporting nations mainly in the Middle East, Russia, Norway, Venezuela and Canada. Now they have the cash dont expect them to come and help the hard pressed western economies theyll be too worried about the oil price crash and balancing their books in $60/bbl oil (rather than the $20/bbl they used in year 2000).

In summary for property investors with oil prices at $60/bbl expect property prices to start rising after 12 more months. But if oil prices rise above $100/bbl expect property prices to stay in the doldrums or fall further. Property is driven by oil prices to put it bluntly.

Any doubting Thomas need only look back on the history of oil prices going skyrocketing in 1971, 1981 and 1991 oil prices peaked and caused recessions in the

Any doubting Thomas need only look back on the history of oil prices going skyrocketing in 1971, 1981 and 1991 oil prices peaked and caused recessions in the

But be careful. As the oil prices have crashed to $57/bbl most OPEC countries have based their budgets on $60/bbl oil. The social spending will continue to keep the populations happy. What will stop is investment in new supply. Meanwhile the banks are pulling the plug on western oil company field investments because of the credit crunch and uncertainty in oil prices so this sow the seeds for the next supply crunch and rapidly (out of control) increase in oil prices some time in the next few years.

Recent Special Reports on Oil Prices and Property

191: Oil Price Update and Real Estate

187: Real Estate and the commodities super-cycle

186: Oil price starts to skyrocket as predicted - how to profit

180: Oil prices continue to skyrocket

172: Make serious money - best investment sectors

169: Oil supply crunch begins

protect yourself

168: Alarm bells ringing oil price shock now on the horizon

163: Making Serious Money as asset prices plateau resources and property

161: Resources winners and losers - ranked list for property investors

160: Find out the winners and losers in the biggest oil boom in history - about to happen...

159: Massive oil boom - the winners and losers - be prepared

158: Supply and demand scenarios - oil boom and the property investors insights

157: Impact of "Peak Oil" for Property Investment

151: Oil price $125 / bbl and rising

how to take advantage in property

150: Peak Oil shortly due to be reach unique insights for a property investor

148: Take advantage of the oil/gas/coal boom key insights

crashing back to $57/bbl (Nov 13 2008). We think they will go back to the $100-$125/bbl level again, but because of the recession - this will likely now take a few years.

crashing back to $57/bbl (Nov 13 2008). We think they will go back to the $100-$125/bbl level again, but because of the recession - this will likely now take a few years.

So our advice is catch the potentially last big wave of property price rises n the UK and USA from end 2009 onward but get out in major oil importing economies if oil prices starts rising dramatically again it will only lead to inflation, interest rate rises, and the asset price bubbles bursting! And all the retiring baby-boomers will be running for the hills the first ones out will be the smart ones. After that its over to

If you have any comments on this special report, please contact us on enquiries@popertyinvesting.net