249: What's next?

01-24-2009

PropertyInvesting.net team

PropertyInvesting.net team

There are no real concrete signs of recovery as yet. Probably the closest that came recently was from Rightmove.co.uk that reported the number of new properties on the market has actually gone down to 45,000 whilst the number of new buyer enquiries had shot up to 450,000 in December almost double the level of a year earlier. The skeptics will say that an enquiry is only an enquiry serious buyers with funding secured are a dying breed and the drop in new homes coming onto the market is a response to declining prices by people that are not forced to sell meanwhile repossessions are in creasing at a rapid rate, some 100% in a year.

creasing at a rapid rate, some 100% in a year.

Much will depend on how quickly banks seriously start lending and reduce deposits that are required. Indeed, we seem to be about half way or possibly a little further through a major correction in the market. Most people are predicting peak to trough falls of some 30% - some even thing it could be 50%. However, the set against a 280% increase over 10 years in many areas (e.g. London, southern England, University cities, nice country market towns and seaside towns) is still favourable when compared with the FT100 stock market that is lower now than it was in 1997, despite inflation averaging about 3% per annum.

There are some massive fundamental stimuli that have been put in place for a recovery:

- Interest rates have dropped from 5.75% to 1.5%

- Oil price have dropped from $147/bbl to $42/bbl

- Tax cuts announced in November

- Capital gains tax reduction from 40% to 18% from April 2008 onwards

Please do not under-estimate the economic impact that the above are likely to have. Everyone will see their borrowing costs drop people who keep their jobs will start to notice more money in their banks and if they start spending it which is quite likely consumer and business confidence could rise quickly say by mid 2009. Most people with variable mortgages should see payment drop from 7.5% to about 3.75% in the space of about 16 months. That's a halving of payments.

The Bank of England are no doubt monitoring any green-shoots of a recovery, and if they dont see any, which is the case up until now, they will start buying asset backed securities. They will continue bailing out banks - nationalizing them (unfortunately with tax payers money). If this does not work to put it bluntly they will start printing money. Yes they are trying to re-inflate the economy. They will do whatever they think it takes to avoid deflation, and mass unemployment. Years ago, the market dictated how deep a recession would be. It seems these days, governments want to control the economy more and are happy to nationalise to creat short term stability - unfortunately at the expense of long term borrowing and health balance sheets. This is rather false in that it props up poorly performing business entities - that said, it prevents a more widespread contagion and mass unemployment - in the short term at least.

The big threat will be the whole thing gets out of hand and inflation rapidly rears it's ugly head again. This is quite possible quite quickly. Particularly if oil prices start rising quickly again property investors need to wacth out for this eventuality. As previously advised, any oil price over $70/bbl is into danger territory and yes, no wander financial markets crashed shortly after oil rose to $147/bbl in July 2008.

We believe the next crisis around the corner will indeed be inflation and the boom-bust cycles (with oil price boom and busts) rather re-imminicent of what was experienced in the 1970s and early 1980s. Property assets are good to hold during inflationary periods because any money invested is leveraged up and as long as property makes a good yield and the investor can afford the interest payments - asset prices should at least broadly follow the inflating trend. Savings though and cash would decline in value as savings rates are low compared to the inflation.

So we rather expect a recovery to gain momentum from mid-end 2009 onwards but inflation to appear again quite rapidly - thence the Bank of England will pull the trigger on a big set of interest rate increases. The best hedges against inflation are gold and oil. Property is not bad eith er as long as the boom does not turn to bust. The strategy is if and when there is another boom you need to position to exit (or partially exit) as soon as you see inflation starting to hit, and before interest rates go shooting up. We regret this all sounds rather reactive but we are entering uncertain times and without some foresight, forethought and planning we property investors can get ourselves into a pickle.

er as long as the boom does not turn to bust. The strategy is if and when there is another boom you need to position to exit (or partially exit) as soon as you see inflation starting to hit, and before interest rates go shooting up. We regret this all sounds rather reactive but we are entering uncertain times and without some foresight, forethought and planning we property investors can get ourselves into a pickle.

So whats certain? Not much, but a few things in the

- London Olympics 2012 regeneration of

- East London Line rail extension 2010

- Eurostar fast commuter trains to Ebbsfleet, Folkestone, Ashford,

Hence our  London

London

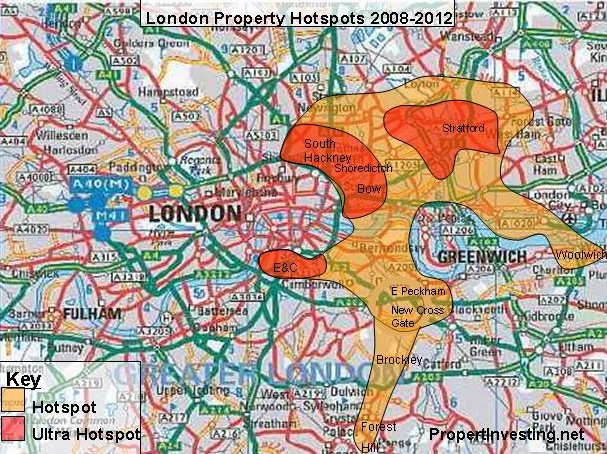

So in summary, we would only invest in

- Bow

- Shoreditch

- Limehouse

- Brockley

- Whitechapel

- New Cross Gate

- Forest Hill

- Woolwich

- South Hackney

- Haggerston

- Kings Cross

- Elephant & Castle - north Walworth

Location is key of course - nice Victorian property very close to new or existing tube, rail, offices and amenities are the preference. This will increase rental demand and asset value increases, particularly if the property is in a quite and relatively safe-low crime neighbourhood.

We hope this special report has helped you. In summary, what out for the end of the crash, then an inflating economy. Avoid manufacturing and public sector exposed towns, cities and country areas. Focus on infra-structure re-generation preferably in

More Special Reports:

For further property reports regarding oil prices and peak oil, please click on the following report:

191: Oil Price Update and Real Estate

187: Real Estate and the commodities super-cycle

186: Oil price starts to skyrocket as predicted - how to profit

180: Oil prices continue to skyrocket

172: Make serious money - best investment sectors

169: Oil supply crunch begins

protect yourself

168: Alarm bells ringing oil price shock now on the horizon

163: Making Serious Money as asset prices plateau resources and property

161: Resources winners and losers - ranked list for property investors

160: Find out the winners and losers in the biggest oil boom in history - about to happen...

159: Massive oil boom - the winners and losers - be prepared

158: Supply and demand scenarios - oil boom and the property investors insights

157: Impact of "Peak Oil" for Property Investment

151: Oil price $125 / bbl and rising

how to take advantage in property

150: Peak Oil shortly due to be reach unique insights for a property investor

148: Take advantage of the oil/gas/coal boom key insights