281: UK property update

08-15-2009

![]() PropertyInvesting.net team

PropertyInvesting.net team

Economies on the mend? News the economies of  uing to move higher, the massive reduction in borrowing costs (almost halving in a year) has stimulated the property market. Yes, banks are very tight with lending they are hoarding the cash raised from the government and borrowing should be more plentiful and at more competitive rates, but all the other stimuli seems to have been enough so far to stabilize the market and lead to some modest price increases in the more wealthy areas (London, southern England).

uing to move higher, the massive reduction in borrowing costs (almost halving in a year) has stimulated the property market. Yes, banks are very tight with lending they are hoarding the cash raised from the government and borrowing should be more plentiful and at more competitive rates, but all the other stimuli seems to have been enough so far to stabilize the market and lead to some modest price increases in the more wealthy areas (London, southern England).

Outlook: So what is the outlook. We believe it very much depends on oil prices. You might say to yourself, whats this got to do with it? To which we point you to the Special Reports on the subject we have prepared on the last five years for detailed analysis and comment.

- 251: Peak Everything !

- 246: Peak Oil - called July 2008 - massive switch needed despite $35/bbl oil

- 244: It's the oil price again - it caused the recession

- 243: Oil price crash sows seed for next massive oil spike

- 242: Oil, Cars & Property - what we'd do if we were UK Prime Minister

- 238: Oil, Cars & Real Estate - what we'd do if we were Pres. Obama

- 191: Oil Price Update and Real Estate

- 187: Real Estate and the commodities super-cycle

- 186: Oil price starts to skyrocket as predicted - how to profit

- 180: Oil prices continue to skyrocket

- 172: Make serious money - best investment sectors

- 169: Oil supply crunch begins protect yourself

- 168: Alarm bells ringing - oil price shock now on the horizon

- 163: Making Serious Money as asset prices plateau - resources and property

- 161: Resources winners and losers - ranked list for property investors

- 160: Find out the winners and losers in the biggest oil boom in history - about to happen...

- 159: Massive oil boom - the winners and losers - be prepared

- 158: Supply and demand scenarios - oil boom and the property investors insights

- 157: Impact of "Peak Oil" for Property Investment

- 151: Oil price $125 / bbl and rising how to take advantage in property

- 150: Peak Oil shortly due to be reach - unique insights for a property investor

- 148: Take advantage of the oil/gas/coal boom - key insights

But in summary

Oil price increase = inflation increase = interest rate increase = house price decline

The ideal conditions are when oil is plentiful, oil prices are low, then inflation (food, services, transportation, energy costs) is low, interest rates are therefore able to be set low, borrowing costs are low and thence people are able to borrow more money at lower rates to purchase a (restricted) quantity of property. Low oil prices in oil importing nations keeps oil import bills low, deficits low, and stimulates growth, GDP increase and asset (read property) prices.

$50 Oil: If oil drops back $50/bbl, this will stimulate the western economies and lead to lower interest rates, economic stability and rising house prices. The only concern would be if oil prices crashed to say $30/bbl this would imply a major prolonged recession or depression with deflation starting in many countries. Oil prices at $50-$70/bbl is probably best for

$50 Oil: If oil drops back $50/bbl, this will stimulate the western economies and lead to lower interest rates, economic stability and rising house prices. The only concern would be if oil prices crashed to say $30/bbl this would imply a major prolonged recession or depression with deflation starting in many countries. Oil prices at $50-$70/bbl is probably best for

$70 Oil: Oil has now risen back to $70/bbl at these levels we give it an amber danger signal. $70/bbl will start to stifle economic recovery likely to be felt late in 2009. But it probably wont have a significant or noticeable impact at such price levels.

$100 Oil: At $100/bbl we enter the danger area red warning by our team GDP g rowth would be suppressed, inflation would start to become a problem, interest rates would rise and within a year, property prices would start to decline again.

rowth would be suppressed, inflation would start to become a problem, interest rates would rise and within a year, property prices would start to decline again.

$150 Oil: At $150/bbl at such price levels, we would get what we had before an asset bubble likely bursting with stock prices and property prices starting to drop significantly and another period of recession in the western world kicking-in. Remember, at $150/bbl, the US oil import bill is about $0.75 Trillion in a year how can a country afford to see so much money leave the country? Thats a whopping $2,500 per person per annum. The

So in summary, for all property investors, do not think these current - in our view benign conditions will stay for long. As inflation starts kicking in early 2010, expect interest rates to start moving up possibly quite quickly. Yields will drop, property prices will then likely stagnate again or could drop IF oil prices rise above $100/bbl. Also ask yourself, do yo believe the current UK and US governments are able to control the inflationary mix that was started end 2008? And do they have a good control on factors such as oil prices and energy supply-demand? If you are skeptical, watch out and consider hedging with oil and gas investments.

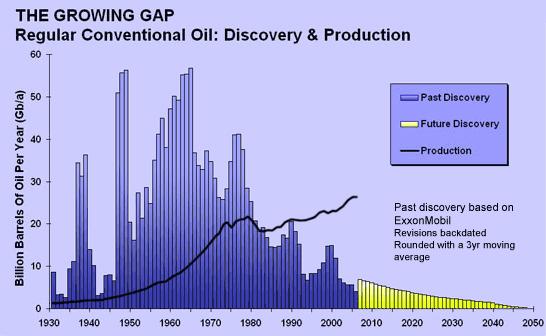

Which way oil prices then? So the big question is do we think oil prices will rise above $100/bbl in the next 18 months to cause this problem. Regrettably the answer is yes. The reason being that Peak Oil we believe was July 2008 and we are now on a bumpy plateau before worrying global production declines kicks in after 2015. Western oil demand has dropped significant, but

An end to low energy prices inflation to rear its ugly head:  We believe the end of low prices energy has arrived for good. Expect oil, gas, coal and metals prices to rise sharply as the economic recovery gains pace. But it will also temper any big GDP growth in oil commodities importing nations. The best performing property markets will be those expose to commodities. For

We believe the end of low prices energy has arrived for good. Expect oil, gas, coal and metals prices to rise sharply as the economic recovery gains pace. But it will also temper any big GDP growth in oil commodities importing nations. The best performing property markets will be those expose to commodities. For

What About So Called Demand Destruction? There seems to be this very western-centric view that oil demand will continue to decline because we have experienced some kind of wake-up call or mini-shock when oil price rose to $147/bbl. And we'll switch to other fuel sources so the issue will go away. We just don't buy this argument. There are some realistic reasons for this:

-

Chinese oil demand will skyrocket as the number of cars rised from the current 25 million to ca. 525 million by the year 2050 - yes, that's half a billion cars. Read our Special Report for more details if you are skeptical

-

Most of the world either does not know about or does not care about "Peak Oil" - it's not even on the radar screen. It's consider a rather intellectual and fringe argument - most people remain skeptical because talk of "Peak Oil" has been around for many years, and oil prices have spiked but then crashed. But we believe this time it is very different - because we have modelled it (see Special Reports listed above). Talk of "Peak Oil" amongst interested nd/or knowledgable people in western countries will NOT stop almost person on the planet from wanting to own and use a car (will it stop you using a car?). If you visit Africa, India, China, Vietnam, Brazil - you will find people wanting cars. They do not want to ride bicycles or walk.

-

Indeed, oil demand is dropping in some western countries, but this is nothing new. In fact, oil demand in Germany and Japan has been declining about 2% per annum for the last ten years. But so many countries have oil consumption that is rising sharply means the countries that use less oil will only make a small dent into over global oil demand.

-

The population of the world is exploding - many countries are only just starting to industrialise. The Middle East is a classic example - as the population rises by ca. 5% per annum, and people get air conditioning, drive to shops, visit ski slopes in Dubai and purchase consumer goods, oil demand is and will sky-rocket, leading ultimately to less oil exports (e.g. each visitor to the ski slope in Dubai uses 1 barrel of oil per visit, a gigantic quantity of energy for little gain). First and foremost, Middle East countries will need the oil for their own usage first, then consider exporting any remaining oil. They will not be burning coal, or using wind or solar - instead, they will burn oil and gas to generation electricity and power desalination plants. As an example, Iran will likely start importing oil after 2018 despite having the tenth largest oil reserves in the world. All the news about major oil finds in Brazil is also interesting - we calculate Brazil will never export any oil - they will still need to import oil as their massive country continues to industralise.

Top electric rail hedges: In the UK it's best to stick close to good high speed electric railway lines examples of such commuter towns with good fast electric links to

- Stratford-Ebbsfleet-Gravesend-Dartford-Ashford

- Woking

- Barking, Ilford, Romford

- Luton -

Death of the Budget Airlines to Obscure Regional Airports: A further warning is the days of low priced budget airline travel we believe are nearing an end. Many budget airlines used small regional airports with low landing taxes to ferry tourists in and out. As airline fuel prices skyrocket, these airline will probably either curtail many of these destinations and/or go under. In any case, even if the flights are retained, they will be costly and be exposed to increases in aviation taxes because of CO2 emissions concerns. Hence, we would be the last people to advise on purchasing countryside property close to one of these small airports with in-frequent flights. These areas have been opened up by low cost budget airline, but can equally be closed down by them as well a property investment risk you will have no control over. Add to this the realization of how much fuel is used to move a person say 300 miles by plane and its impact on CO2 emissions, we seriously question how many more years frequent airline travel can continue with Peak Oil now behind us. It was great fun while it lasted and all those weekend trips to Pau and Gdansk for £50 round trip were exciting, but the world will probably get real shortly and start to tax aviation fuel like they do normal car and truck fuel. As for the Seychelles and Maldives, whether the super-rich can keep these destinations active is a key question. Cape Town in South Africa is also exposed.

to advise on purchasing countryside property close to one of these small airports with in-frequent flights. These areas have been opened up by low cost budget airline, but can equally be closed down by them as well a property investment risk you will have no control over. Add to this the realization of how much fuel is used to move a person say 300 miles by plane and its impact on CO2 emissions, we seriously question how many more years frequent airline travel can continue with Peak Oil now behind us. It was great fun while it lasted and all those weekend trips to Pau and Gdansk for £50 round trip were exciting, but the world will probably get real shortly and start to tax aviation fuel like they do normal car and truck fuel. As for the Seychelles and Maldives, whether the super-rich can keep these destinations active is a key question. Cape Town in South Africa is also exposed.

If you do select to purchase holiday property abroad, better off to research areas with outstanding high-speed electric rail lines close by - close to high paid jobs and industry. Examples include

- Massive infrastructure development in the next ten years

- Olympics

- City of

development

development- Thames Gateway developments

- Eurostar-High Speed One

- Crossrail

- Dockland Light Railway Expansion

- South Bank regeneration (Nice Elms US Embassy)

- Croydon regeneration

- Ebbsfleeet station-Gravesend

- Barking-Romford-Ilford regeneration

- Eurostar links to Paris, Brussels, Cologne, Lille

- Olympics

- As oil prices rise, there will be net inflows of wealth

- Green technology and trading centres

- Less reliance on public sector jobs than the rest of the

- Good electric rail and tube infra-structure for post Peak Oil era

- Expanding population by a further ca. 0.8 million by 2015

- Financial service global centre

- Tax haven for international wealthy

- Tories will likely be in power by mid 2010 historically, this party tends to stimulate business and cut back on public sector expenditure and lower taxes this is likely to benefit

- Best city to invest in as a hedge against high oil prices in the

- Decline in £

- Stock market crash has given another boost to property as a safe heaven

- Higher income tax at 50% (up from 40% by 4th April 2010) for many Londoners will likely lead to high net worth individuals investing in property that saw a drop from 40% to 18% in capital gains tax April 2008.

- Lower taxes if the Tories win the next election would likely give a boost to property prices in London particularly if finances can be sorted out in ca. 3 years time

UK

UK

- Manchester-Salford

- Bradford-Saltaire

- Nottingham and

- Newcastle-Gateshead

- Halifax

But its more difficult to see with high oil prices cities that are more reliant on manufacturing and public sector jobs outperforming

only surmise that the dash to create jobs during the recession has stimulated a flurry of approvals - in part to keep economic momentum going. Jobs are what are required in hard time. When you look at the shear size, scope and quantity of the regeneration projects outlined above, we hope you can understand why we keep on about investing in

only surmise that the dash to create jobs during the recession has stimulated a flurry of approvals - in part to keep economic momentum going. Jobs are what are required in hard time. When you look at the shear size, scope and quantity of the regeneration projects outlined above, we hope you can understand why we keep on about investing in

We hope you have found this Special Report interesting. If you have any comments, please contact us on enquiries@propertyinvesting.net

Peak Oil - World Oil Production Consumption

Gas Pump Prices - are likely to rise in 2010 onwards. But in the UK, because petrol tax is currently 75%of a tankful, if oil price double or rise by 100%, a tankful will (only!) go up by 33%. Whether you can describe this as good news is open to debate!

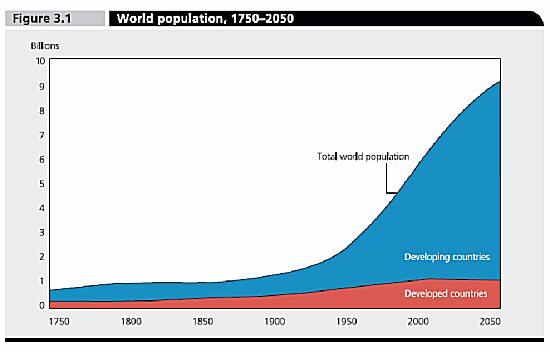

World Population: Anyone that thinks oil demand will not rise moving forwards with so many young people in te world wanting cars is, in our opinion, rather unrealistic. Expect oil demand in developed countries to drop slightly, with oil demand in developing countries sky-rocketting after 2010. Price, we believe, will move higher - before they act as the key constraint to demand - at some price higher than $150/bbl.

Oil Bills: Look at these massive oil import bills for the different regions. The Middle East earns a gigantic net $1 Trillion a year at $150/bbl. Much of this is pulled from Japan, USA and China along with western Europe (except Norway, Russia and Canada).