291: China

09-19-2009

PropertyInvesting.net team

PropertyInvesting.net team

China Investments

There are 1.5 billion people living in China. As the econom rapidly expands and matures, the wealthy middle classes will grow very fast - much of their income will be invested in property in their home countries.

Rising Incomes: Luxury properties in the big business centres such as Shanghai and Beijing will likely rise in value dramatically. Holiday home property will also shoot up in price. The price of sea-side resort property along the southern coastal provinces will likely rise dramatically - as income earned from the manufacturing in the southern Chinese coastal provinces finds its way into holiday homes along the coast and luxury  apartments in central Shanghai. If the GDP grows by 8-12% per annum, this percentage would probably translate into the lowest level of annual property price increases - house prices often rise at double the rate of GDP growth in areas with land shortages. There is no reason to believe asset prices in China will not rapidly catch up with Europe and the USA.

apartments in central Shanghai. If the GDP grows by 8-12% per annum, this percentage would probably translate into the lowest level of annual property price increases - house prices often rise at double the rate of GDP growth in areas with land shortages. There is no reason to believe asset prices in China will not rapidly catch up with Europe and the USA.

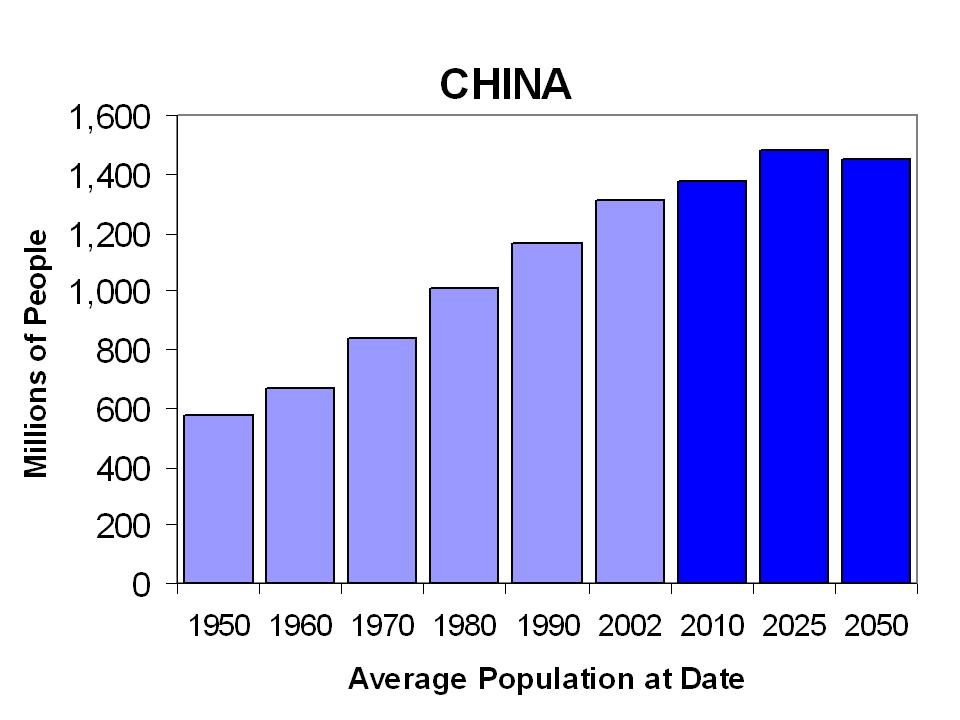

The demographics of China are robust for the next 25 years - the population will continue to increase slowly which will further drive GDP growth. However, because of the low current birth rate (from ~1985 to present), an aging population issue will become evident by 2025 - and is showing some early signs in the demographic make-up.

The sheer number of educated hard working, predominantly risk taking and technology-savvy workers will help incomes increase and asset prices grow - it's only just starting - in 20 years time it is difficult to imagine why prices in the most popular areas would not be similar to Europe's.

中國物業投資 Chinese Property Investment

Massive GDP Growth: For any doubters, recall that China's economy has grown between 9% and 12.5% every year for the last ten years - only broken by a 6 month period Q4 2008 to Q1 2009 when growth dipped to a low of 8%. It is now starting to motor back to 12% - currently 10%.

If you want convincing of China's long term potential, take a look at the projections on population growth and GDP - property prices in central city areas will likely reach London price levels in the next 15-20 years or earlier.

We have already done an analysis of the demographic trends that are important to follow. What we can now provide you is a chart showing the projected GDP for

What the chart shows is the tremendous increase in GDP in both

Population: China's Population growth and projection - population declines after 2025

Peak Oil: But what out for Peak Oil - after 2013 oil shortages are likely. China will need massive new oil production supplies and we frakly do not know where these will come from. The made dash for oil, gas, metals, coal and other resources has only just started. It's like building three USAs in 25 years - the amount of energy required is mind-boggling. Much will come from coal, renewables will play a larger part. Gas production in China will increase. Oil production has increased eery year for the last ten years - but not enough to prevent oil imports sky-rocketing, which help drive oil prices to $147/bbl in July 2008 coinciding (probably no coincidence) with the Beijing Olympics.

Global Population Trends as Context for China: The PropertyInvesting.net team have performed an analysis of global population trends. This unique analysis provides an insight into the highest impact population growth areas for property investors. This is important as GDP growth often mirrors population growth, and as cities and areas expanding in population, business growth increases, land shortages develop, housing demand increases and asset prices tend to follow. So for the Global Property Investor, these insights provide key pointers to where one should invest. Where demand is likely to be strongest - residential, commercial and land demand will rise and asset prices and rental prices should follow.

The Population Growth Impact chart below takes the population predicted in 2050 and multiplies it with the percentage population growth predicted from 2002 to 2050. This measure can be described as the proportional impact the population increase has within the global population pool. The key conclusions are:

·

·

If we take the Growth Index from a historical 1950 to 2050, this illustrates how massive the impact of the population explosion has been in India, Nigeria and Congo in particular.

Note the massive increase in population expected in India. China also adds a further 100 million - however, it's current population is gigantic. By 2025 China will start suffering from an aging population because of low birth rates fom 1990 to present.

Continued Growth: If we now predict which countries may be best to invest in property, one would normally choose the countries where the highest GDP growth is predicted. This is difficult to predict, but

Urbanisation: In urban areas with important business and commercial centres, real estate prices will likely skyrocket, particularly in central districts. Select coastal locations, in south coast resort areas, should also do very well as wealthy Chinese retire or purchase holiday homes. The Chinese prefer to retire close to their family this should support a widespread increase in prices, particularly in more heavily populated areas.

Projected GDP Growth what impact does this have on your investments? We have previously made the point that trends are particularly important when deciding where to invest in property. Capital values and rental income will often follow economic fundamentals. Ultimately, the more we produce and earn, the higher the capital property values are likely to be. Property values tend to mirror GDP with a strong overprint of supply and demand. The supply might be constrained by lack of land, lack of building. Demand might be stimulated by more people moving into the area and rapid economic growth.

Oil Price: Projected 3 yearly weighed moving average forecast oil price - assuming Peak Oil was July 2008 and bumpy (slighty declining) plateau to 2015 then drop-off - decline from then onward. This projection is then used to model oil import bill for Far East countries (below)

Net Import - Export surplus-deficit oil for Far East using oil price projection above (modelled back in Sept 2007)

China investment trends - socio-economic impacts

This extensive report covers how to use socio-economic trends to drive your investment decisions. The report includes a survey of major current socio-economic trends including:

- The impact of baby boomer power on the Chinese economy

- The impact of the global economy on property prices

- Will globalisation lead to an exodus of people from

- Will globalization reduce the cost of building in

- The opportunities for the buy-to-let market created by Chinese expansion

- The impact of supply and demand

- The impact of property investment funds

- The effects of the Nimby (not-in-my-back-yard) factor on supply in

- The Shift from Agriculture to City Centre,

- The impact of the Chinese planning process

- Predicting the next popular holiday resorts for property investment

- Will ex-communal resorts come back into fashion?

- Is

And finishes with:

- Summary of current socio-economic trends in

- Favourable investment areas in

- Crystal ball gazing - what about future Chinese and Asian trends?

Using Socio-Economic Trends to drive investment decisions

We are great believers in the value of monitoring and taking appropriate time to think about economic, social and marketing trends. They guide the way we should invest and help make for better investment decisions and improved investment performance for the longer term. Thorough analysis often leads to a more predictable, deterministic (or measurable) investment outcome.

Lets take an example of trends in new transport/communication impacting property prices. As a rule, I only invest in property in areas that are positively changing. This normally means that a new train station/road is being built close by or regeneration is ongoing. It remarkable how little the average person considers when they buy their homes they won't notice until they can actually see and use the newly built station which is when the prices start moving up dramatically. Demand arrives when infra-structure opens any demand before this is driven by investors speculating on what might happen.

Lets take an example of trends in new transport/communication impacting property prices. As a rule, I only invest in property in areas that are positively changing. This normally means that a new train station/road is being built close by or regeneration is ongoing. It remarkable how little the average person considers when they buy their homes they won't notice until they can actually see and use the newly built station which is when the prices start moving up dramatically. Demand arrives when infra-structure opens any demand before this is driven by investors speculating on what might happen.

The trick is to get in well before the station opens, before it can physically be seen even being built. An example is investing in property in a Chinese city even before the Olympic bid was won - then continuing until the new infra-structure is build. It is remarkable that no-one seems to notice intul the infra-structure actually arrives. Most property purchasers do not give it much thought. Investors certainly do, as do companies and developers. Most the market is not ultra-intelligent. Its quite easy to beat the average market with some good analysis and thought.

Baby-Boomer Power Impact on Economies and Change

One outcome of the Chinese and Asian demographic shift to an aging population will be a concentration of power and wealth with the retiring population. The voter turn-out amongst the low numbers of younger people will be very low compared to elderly hence the politicians are likely to pander to the baby boomer wishes to capture these votes.

One just needs to look at what happened in Japan since 1990 as an example of these dynamics Japans baby boomers started retiring in the late 1980s the Nikkei was at 38,000 and when the pensioners started pulling on their retirement funds, the Nikkei crashed to below 10,000, growth stopped, deflation set in and economic reform was very slow. Only now after 2003 did

One just needs to look at what happened in Japan since 1990 as an example of these dynamics Japans baby boomers started retiring in the late 1980s the Nikkei was at 38,000 and when the pensioners started pulling on their retirement funds, the Nikkei crashed to below 10,000, growth stopped, deflation set in and economic reform was very slow. Only now after 2003 did

Europe (

But

Global Economy Helps Property Prices

Globalisation of industry has lead to more companies operating efficiently across countries and regions. Outsourcing of services and a shift of manufacturing to new low cost and wage centres is a trend set to continue. As under-developed countries are able to apply and manage new technology to produce goods and services cheaper, this should lead to lowering of prices over time and keep a lid on inflation.

Globalisation of industry has lead to more companies operating efficiently across countries and regions. Outsourcing of services and a shift of manufacturing to new low cost and wage centres is a trend set to continue. As under-developed countries are able to apply and manage new technology to produce goods and services cheaper, this should lead to lowering of prices over time and keep a lid on inflation.

The internet is an example of a medium that cuts across country boundaries to provide goods and services cheaper. Developed countries will have to shift towards knowledge based high-end services (bio-technology, financial management, services) and will be maximising profits and economic potential from low cost mass manufacturing centres such as

Hence our prediction is for benign inflationary pressures, higher company profits, margins and productivity and low interest rates over the longer term both fixed and variable. We see Chinese interest rates rising to say 5% then coming back down as the economy slows. This should all support house prices as the new order will be that households and individuals will be allowed to borrow higher and higher multiples as capital becomes more plentiful and cheap, particularly for the stronger currencies.

One could argue this same globalisation could suppress house prices since people can buy abroad cheaper, particularly holiday homes. However, this ignores the fact that most Chinese citizens either have to or want to live in

Will Globalisation and Retirement Lead to an Exodus from

We do not believe there will be a mass exodus out of

We do not believe there will be a mass exodus out of

A large proportion of the wealth created by low cost labour in countries like

One could also argue that building could become cheaper in

One could also argue that building could become cheaper in

Hence we think the building companies operating on price/earnings ratios of about 6 look like good value. Demand should stay strong with supply constrained because of the slow planning process. New building practices slowly feeding through will likely improve profitability further, though we cannot see any material impact from the recent Housing initiatives. Technology will not take the place of housing. Building innovation is slow and is likely to remain so because of a conservative approach to lending by banks and traditional housing views of the customers.

Impact of Asian Business Expansion

The expansion of the Asian trading block will attract hundreds of thousands of cross border workers to Asian countries and generate massive new demand for accommodation. .

The expansion of the Asian trading block will attract hundreds of thousands of cross border workers to Asian countries and generate massive new demand for accommodation. .

As country borders become more open for migrating workforces, the lower cost labour will gravidtate to where the work is. This might mean that

These cross borders skills sharing will likely lead to improved rates of return for investments and

What Impact will Housing Initiatives have on property prices and investment?

Chinese Housing Initiatives which drive the large scale housing developments in

However, because of the control of Chinese in the house building and permitting process, severe housing shortages are not likely to develop. The Government will want to keep the population at ease by providing access to housing and hence massive home building programmes will continue. Suburbs will spring up and a new middle class will develop these successful business and public sector workers will want good quality family homes within commuting distance of central city locations. Workers living in apartments will aspire to own small houses. Small home owners will aspire to live in larger detached houses with gardens. The normal property dynamics that occur in other parts of the world will not be much different in

A rise in protests from displaced people might slow home building process in future years, but for now, strong control by local and regional government supplemented by state level control should provide a platform for massive house building growth, rising supply to fuel the massive increase in demand.

What Impact could Property Investment Funds (PIFs) have on property prices and investment?

If the Chinese government introduce tax efficient US style Real Estate Investment Trusts (REIT), this could help fuel the building boom. These have proved popular in other countries around the world private companies turn themselves into tax efficient trusts and dividends are distributed to investors with tax breaks. The important thing is how the REIT policy is described and enacted to make sure the correct gearing, share ownership rules and dividend payment rules are attractive for private firms. These PIFs are often popular with retirement funds because their investment risk is rather lower than stock market investment. Also, many pension funds have a larger weighting of property in their portfolios now compared with 10 years ago.

So what about the much talked about nimby (not in my back yard) effect? This is a phrase coined in the UK and USA - listening to John Porritt, the CEO of Friends of the Earth based in the UK, this factor  only likely to increase. Mr Porritt said that the environment will always become more important to people over time. In a given period, it will either stay on a plateau or increase it will never decrease.

only likely to increase. Mr Porritt said that the environment will always become more important to people over time. In a given period, it will either stay on a plateau or increase it will never decrease.

This is what we see with nimbyism. People get genuinely angry with development in their community or immediate area or sphere of interest. Countries face massive housing shortages on the one hand with increasing populations and nimbyism on the other. Nimbyism leads to supply decrease if demand stays the same, then prices will move up. These factors could of course make it increasingly difficult for first time buyers and key workers in

One unknown factor is how much help first time buyers get from their parents. Their parents are likely to have large amounts of equity tied up in property in future years releasing some would be enough for a deposit for a first time buyer. If this equity release and gifts to offspring occurs systematically, it would support the lower end of the markets and improve ability for housing chains to occur. It may also decrease elderly people inheritance tax liabilities by helping their offspring buy property.

The planning process is current fast. But it could slow, become more bureaucratic and cumbersome as the Chinese economy matures. The reasons for difficulty getting plans through are numerous. Number one is  probably Nimbyism of locals and communities. There may only be a small minority of the population, or even one or two very vocal opponents, but this can either stall or kill any developments, sometimes for very good reason.

probably Nimbyism of locals and communities. There may only be a small minority of the population, or even one or two very vocal opponents, but this can either stall or kill any developments, sometimes for very good reason.

Related to this, it is often not politically acceptable from a local stand-point to agree to new developments planners and councilors do not wish to upset their stakeholders the general public or the most vocal public in the local area. These public citizens after all vote in their councilors, so their power is not to be underestimated. These protests also constrain development and to a lesser extent probably reduce local economic growth.

However, if an area is particularly attractive, hideous developments can actually damage tourism and reduce the quality of life for residence living in the area. For areas that are less attractive and have higher unemployment, less reliance on tourism, and areas that have degenerated, barriers to development are far lower.

An example is what has been possible in the coastal area of

So if you want to build a new house, youll find it a whole lot easier where the Local Plan caters for new housing and sustainable development. Youll probably be wasting your time in an established historic small villages or town with constraints on development, unless you find a good brownfield site.

More is being done to develop brownfield sites in existing cities and towns in

Shanghai

Shanghai

As land becomes scarcer, more properties will be demolished and re-built as bigger homes particularly those on large plots with good views in private locations.

We also think the planning process will slow down and land will become more difficult to acquire for building purposes - so homebuilders will be able to keep prices high because of high demand and some degree of drip-feeding supply, or some would say step-by-step supply. Part of the reason why drip-feeding of supply takes place is related to financing. It seems the capital markets have not forgotten about the boom-bust cycles of Europe,

Funding is not easy to come by for large capital-intensive developments that require much of the infra-structure costs committed up front and very expense planning processes. To be on the safe side financially, and also because of acute shortages of skilled building labour, developers have to build in a step-by-step fashion.

Shift from Agriculture to City Centre,

There is likely to be a general trend away from agricultural village living in small houses to city centre flats and holiday homes in seaside areas. This will follow the trend of the baby boomers retiring. A massive increase will take place of demand for suburban houses and smart apartment for the new Middle Classes.  The increase in the numbers of your average company suburban small working families will lead to increasing demand for suburban houses. Remote village property will be the losers prices will rise, but not nearly as quickly as city property.

The increase in the numbers of your average company suburban small working families will lead to increasing demand for suburban houses. Remote village property will be the losers prices will rise, but not nearly as quickly as city property.

A trend over the last twenty years has been the increasing number of middle class families that aspire to live in a trendy city houses and apartments. These new wealthy city dwellers will want luxury, spacious property in central locations, in the best areas for schools, services and leisure activities.

As land becomes less economic to farm and the farms that remain become more mechanised and intensive, farms will be merging some old farms will eventually be bought for purely residential purposes, particularly those close to cities. It is mainly the city dwellers who have made enough money that are buying these properties this trend is likely to continue and the value of such farms, close to cities will rise. The land value will also rise with it.

One investment model is to buy a farmhouse only, then negotiate the purchase of some land around it thereby considerably increasing the overall value of the property. Before exchange of such property, an option can be bought from a farmer for such a purchase, thereby reducing the risk that the land cannot be acquired prior to the commitment to purchase the property.

We would envisage that farms with a reasonable amount of land (say 3-7 acres), particularly with countryside or sea views and close to cities, will be able to command an ever increasing premium, as retiring city dwellers chose to move to quiet locations, where they can enjoy recreation, walks etc.

Chinese

Properties with sea-views should be targeted. The bottom line is, there are not many properties in the China with sea views many of the 300 million or so baby boomers will want these views, so the prices are more likely than not to go up for such property, especially as it is so difficult to obtain planning permission for new properties with sea views land is scarce, nimbyism is omnipresent and people dont seem to like the coastal views or character altered.

Ex-Communal

Traditional Chinese seaside resorts have been generally on the decline since the mid 1990s when mass communal tourism ended. However, these same locations are likely to transform themselves as the 300 million Middle Class Chinese desire a holiday home in an area they used to visit in their childhood. Thee resorts will be re-developed into private resorts with some top class entertainments and leisure activities (e.g. golf, walking, sunbathing).

Traditional Chinese seaside resorts have been generally on the decline since the mid 1990s when mass communal tourism ended. However, these same locations are likely to transform themselves as the 300 million Middle Class Chinese desire a holiday home in an area they used to visit in their childhood. Thee resorts will be re-developed into private resorts with some top class entertainments and leisure activities (e.g. golf, walking, sunbathing).

People have always desired to be at the sea for a mixture of fun, nostalgia and thrills. People have had good fun in their childhood at the seaside and it reminds people of their childhood and family. We predict the resurgence of interest in these resorts in the next 20 years as baby boomers retire, and wish to live at the sea-side in

In these resorts where improved communications to major employment centres and facilities occur, regeneration and improvements should drive up prices, particularly in property with sea/coastal views. We do not believe most Chinese citizens will want to move to Thailand and other Asian countries permanently they may have a holiday home there, but their desire to be close to their families and friends will keep them in China and the best place will be along the south coast of China, with good communications to Shanghai and the populated Guangdong Province (close to heir family, ex-business, airports, services).

We are quite positive about all

- Jobs - employment it healthy and is likely to stay so with the city being a financial centre, technology, education, transport links and proximity to mainland Japan and other markets

- Demographics another 5 million people are forecast to live in the area by 2020 a massive increase which should sustain demand

- Intra-structure new airports, Olympics, infra-structure developments, rail improvements and massive private sector investments and businesses moving in also strong growth in the public sector services such as hospitals, universities, and government jobs

The most significant risks is probably overheating of the economy or high energy prices and a subsequent bust environment, but we believe the government will control the financial services sectors risks are therefore relatively low.

To further develop the argument for the importance of trends, the other reason why we believe in the longer-term investment potential of property in

To further develop the argument for the importance of trends, the other reason why we believe in the longer-term investment potential of property in

- Lower unemployment and higher employment levels

- Low interest rates and low inflation cheap borrowing

- Massive manufacturing expansion, exports and foreign trade surplus

- Asian economic convergence leading to sustained lower future interest rates

- Massive pool of 1300 million people provides a huge workforce to keep costs down and keep

- Chinese people strongly aspire to own their own property this should continue

- Property taxes are not too high this should continue as the government would lose too many Middle Class votes if they raised property taxes significantly

- There are more and more single person households (or small numbers of people per home) caused by an aging population, more divorce, more individualistic behaviours e.g. young unmarried couples often keep two properties for security in case they split up

- It seems people are becoming more selfish wanting to maintain their own independence and financial security property is one form of asset that supports this behaviour

- Easier and more competitive financing available to the average person and high debit to earnings multiples accepted as the norm by banks

- Economic attraction of purchase over rental

- Chinese desire to own a property for status reasons homes (often more than one) have become the most desired status symbol for all age groups in

- Shortage of land, both

- More problematic supply side of building new properties, especially low priced properties, in part due to the Nimby effect (not in my back yard) and in part by stricter planning regulations in future years

- People like to live close to work, and city living has gained in popularity recently more amenities, café culture, arts, networks, social aspects, lower or stable crime rates, diverse cosmopolitan environment.

The key risks that would work against property prices rising are higher unemployment, high oil/gas prices, higher interest rates, and poor affordability leading to the average person preferring to rent property instead. We believe in the medium term we still have a long way to go and that

The key risks that would work against property prices rising are higher unemployment, high oil/gas prices, higher interest rates, and poor affordability leading to the average person preferring to rent property instead. We believe in the medium term we still have a long way to go and that

We have found reading books there is very little concrete investment advice about where specifically to look for property opportunities it seems people either want to charge for this type of service, are not willing to share it or it just does not exist. We have a different strategy we like to share investment advice on property we see nothing to lose from this.

Some of the Most Favourable Investment Areas

We will give you the areas we most favour at the moment for 5-10 year investment horizon central

We also like in the medium to longer-term south coast resorts particularly flats and houses with sea or harbour views these are the future retirement homes of the baby-boomers.

We also like interior low cost cities like Xian which will benefit from the internet and high-tech business development over the next 20 years.

All the above are micro-to-macro socio-economic trends, which can be used to justify (or not) investment in medium sized very central 1-2 double bedroom apartments in

Possible Future Socio-Economic Scenarios and Trends

We would advise it is good practice to take an activ e interest in trends - you may find these helpful to consider with regard to how your lifestyle could develop or be impacted in the future. We would like to flag these so you can consider them when planning your lifestyle, investments, and retirement.

e interest in trends - you may find these helpful to consider with regard to how your lifestyle could develop or be impacted in the future. We would like to flag these so you can consider them when planning your lifestyle, investments, and retirement.

Please consider them as possibilities rather than most likely to occur they are both opportunities and/or threats (risks). The purpose of listing them is so you can at least consider them for planning purposes, so they dont hit you in the face one day! The possible future trends below also contain more detail on the current trends outlined above. And no, we do not have a crystal ball all the same, here goes:

- New regulations enacted that puts retirement age at 70 by 2015

- Massive water shortages in many parts of

- Massive gas and oil shortages in

- State pension reduced to 75% of current value affordable levels to maintain stable Government deficit levels

- One last stock market bull run ends in 2008 when stock market crashes for good (Dow at 7000, FTSE at 3500 and never recovers) no public capital equity markets needed any more as industries become non capital intensive. The aging European and

- Serious pension crisis in countries with low population growth as the baby boomers retire and live longer and health care costs escalate life expectancy of 90 in developed countries by 2050.

- Environmental standards go up further and stricter legislation introduced to conserve energy and the environment

- Hydrogen economy kicks-off in

Large tracts of land in the Europe and USA given over to environmental groups to let go naturally wild as farmers retire, farm land prices drop and over supply intensifies (caused by biotechnological advances)

Large tracts of land in the Europe and USA given over to environmental groups to let go naturally wild as farmers retire, farm land prices drop and over supply intensifies (caused by biotechnological advances) - Building land prices go up further as planners and environmental group continue to complain about development in green-field areas all remaining brownfield sites are used up - people start demolishing old buildings to build new more intensive housing in good locations

- Best people bail out of large companies into private equity funded companies, making publicly traded capital equity markets almost redundant by 2020

- House prices in retirement centres (on coasts) double (again) in China, Europe and USA, as environmental constraints stifle further building an example of a most prestigious status symbol becomes a two-double bedroom luxury flat looking over a marina, beach or bay in southern China and a central Shanghai penthouse apartment

- Super-rich individuals charitable foundations become all the rage with celebrities vying to be seen to do the most e.g. organising high profile prestigious events

- Retirement homes on golf courses become even more popular throughout Asian and command premium prices as the grey tigers retire

- Mobile telephones with built in video-cameras allow people to communicate live over the internet / teleconferencing using their phones

- Internet shopping becomes established only the largest and most glamorous shopping malls stay popular for social aspects of shopping massive increase in retail internet spending.

Despite new technology, the norm by 2015 is still the 9-5 job working for either the public sector or companies however, more flexible hours are offered, and more occasional work done from home as people get used to workers using quiet time at home to do certain focused tasks (with face-to-face meetings in the office, and video/teleconference calls over the internet supplementing these when possible)

Despite new technology, the norm by 2015 is still the 9-5 job working for either the public sector or companies however, more flexible hours are offered, and more occasional work done from home as people get used to workers using quiet time at home to do certain focused tasks (with face-to-face meetings in the office, and video/teleconference calls over the internet supplementing these when possible) - People commute from

- Work-life balance becomes more important to people and tensions build with companies who view this as a threat many more people down-shift to lower paid jobs with better work-life balance. Many can afford to do this because of acquired property wealth. High stress, high working hours, high wage jobs start to be considered old fashioned - younger people aspire for less corporate type jobs with more flexible hours and working conditions. The best talent goes it alone and join private investment equity companies, where they can more readily dictate their own terms and working conditions.

- More outsourced will occur from Europe and

- Chinese language course in English will boom as business becomes more international

- Divide between the haves and have nots gets bigger

- Regulations by the governments of developed countries will dictate that 50% of all vehicles by 2020 will be powered by alternative fuel sources (e.g. hydrogen, electricity, battery)

All Chinese and

All Chinese and - Open cast coal mines in

- Low cost air travel to regional airports makes it increasingly popular to take long-weekend breaks from China to HK, Thailand, Singapore, Macau and Malaysia - whole industries develop around offering air travel customers value propositions (e.g. property, car rental, leisure, financial services, retirement services).

- There will be a doubling of air travel and vehicles from current levels in

- Business and jobs are increasingly located close to regional and international airports, since worker need access as employees do more Asian and global business and leisure related travel.

- Employees increasingly regard themselves as individuals rather than collective institutional groups negotiating individual deals and working conditions. The best elderly employees urged to stay on as a shortage of experienced / knowledgeable workers in certain industries takes hold as more talented individuals retire early retirement is a thing of the past since people wish to stay mentally active even if they are financially secure.

- Road transport mileage grows by 300% in China by 2020 leading to far more congestion tolls on key motorways introduced to discourage use by private motorists new motorway building at very low levels due to nimby behaviours, further exacerbates the problem. More investment in fast trains, but this is not enough to significantly reduce congestion. People start to travel overnight or in off peak periods more increase in budget hotels along key routes. Big price premium for property with car parking space or a garage in central city locations.

- All docklands are developed along the

- Some form of fat tax introduced on junk food in

- Environmental legislation gets far stricter

- Increasing interest in charities as wealthy individuals become increasingly competitive to be seen to give to charitable causes this gives status and prestige and mitigates guilt on behalf of wealthy individuals.

- Global oil and gas production outside OPEC shows serious signs of decline by 2010 - increasing reliance on OPEC and Russian imported oil and gas to secure supply and power.

- India/Bangalore becomes the aspired centre of software excellence European and US companies outsource all back-off and IT services to the Indian subcontinent and challenges China for IT-services global dominance hrough 2025

- Oil prices remain high (at least $75/bbl) as OPEC cartel maintains control of price and the US finds it is in their self interest to keep prices high to safeguard domestic oil production/supply as well as helping keep Middle East revenues high to maintain regional stability non oil producing countries feel the brunt as this has the effect of knocking 0.5% off their growth rate.

- Regional airports double in capacity by 2015 requiring upgrades of road infrastructure and providing many new jobs.

- Old docklands areas are redeveloped into thriving export centres and luxury housing complexes.

- Media hype and horror increases on TV as media becomes even more intrusive and live graphic images are beamed into our living rooms of bombs, violence and unrest, creating impression that the world is going down hill in order to capture more viewers, improve ratings and increase advertising revenues.

The key question you should ask yourself in relation to these trends is - how can I maximise my value from these trends, both financially and lifestyle? The key way to gain financially from these trends is to invest money where you can see positive changes occurring.

We hope you have found this Special Report helpful. One can also refer below to come images of China. Please do not hesitate to contact us on enquiries@propertyinvesting.net if you have any comments. Please feel free to forward this particular article to any friends-family-colleagues.

中國物業投資 Chinese Property Investment

Lady host at China car show

China car company BYD - rapid expansion into electric cars

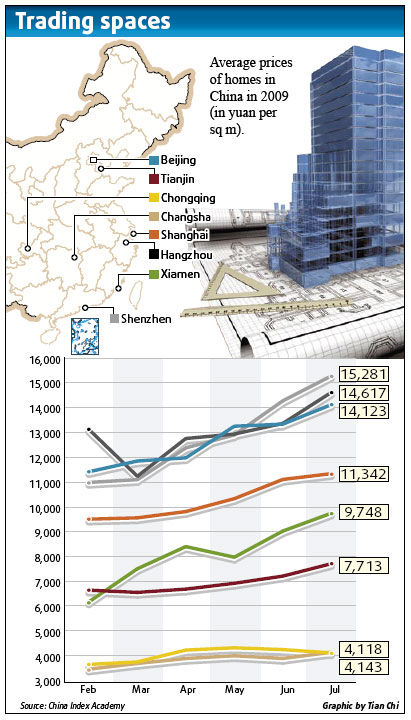

Chinese property boom - price keep rising

China super rich - Cartier store - prestige and status - love of gold, luxury

Chinese male models - fashion is a massive growth business in China

China Models - modelling Haosha under garments on catwalk

Zhou Xun - famous actress

Zhou Xun

Li Bing Bing in Forbidden Kingdom

Song Hye Kyo

Song Hye Kyo

Song Hye Kyo

Qi Pao - Chinese body painting is very popular with beautiful designs

Shanghai Auto Expo Car Show - hostess

Chinese Man - Daniel Wu - successful business person

Chinese body art - beautiful designs

Takeshi Kaneshiro - model

Bing Bing

Bing Bing Lee

Bing Bing - filming dagger scene

China Olympics - Day 1 Beach Volleyball

Chinese businessman