427: This is Peak Oil - the undulating oil plateau - rising costs - western economic decline

05-17-2012

![]()

Consumption Continues to Outstrip Supply leading to high oil prices, worsening the Euro debt crises and Arab uprisings this will ultimately lead to some form of economic crash in 2013 as oil, silver and gold prices going ballistic.

High Oil Prices Lead To Crises: It lead to the US, China and Europe printing money after the financial crash that then sent food, inflation and energy prices skyrocketing by 2010 leading to the Arab Spring uprising in 2011. Oil prices sky-rocketed again due to supply constraints and the excessive printed money in 2011 along with the Libyan civil war. This put huge strain on indebted developed western nations with high oil import costs like Spain, Greece, Italy, Portugal and Ireland. These countries have been bailed out numerous times, but it only seems a question of time before the Euro-zone splits. In our view, we might be the only ones saying this, all of this economic mess has its route cause on Peak Oil or at least the lack of cheap low cost oil. Never again will we see cheap oil. This will p ut huge strains on countries that have no significant indigenous oil production like:

ut huge strains on countries that have no significant indigenous oil production like:

· Greece

· Italy

· France

· Portugal

· Spain

· Belgium

Powerhouses: Some of the better organised manufacturing power-houses like Germany, Austria, South Korea and Switzerland have little or no oil production, but they have technology, manufacturing, are well educated, hard working and industrious. They should be partly shielded from the ravages of Peak Oil. But the weak will get weaker and countries like Greece that prospered from cheap oil, low cost flights, cheap Euro finance and Euro subsidies to expand a bloated public sector will suffer hugely in coming years as oil prices remain high.

Fundamentals: When we hear people pronouncing Peak Oil is dead that there is plenty of oil they are missing some key points:

· Low cost oil in the Middle East cost $35/bbl to extract rather than $1/bbl it did 10 years ago these soaring costs will keep oil prices close to or more than $100/bbl henceforth

· Oil Sands costs the marginal economic price of a new barrel to allow supply to meet demand has skyrocketed to about $90/bbl

· Demand destruction has kicked in again the second time since mid 2008 a four year economic cycle when the global economy slows down and western nations enter recession again

· As demand drops, supply appears to be plentiful, but this masks a frantic effort to keep production rates high in all countries taking advantage of high oil prices. But you can see that the high oil prices have not lead to a significant increase in supply. Its the classic Peak Oil undulating plateau we have been predicting since 2007.

· The developed nations have 5 billion people they all want to drive cars there will continue to be a scramble for oil to build cities and create consumer economies in China, India, the Middle East and Far East plus Latin America. This oil will have to come at the expense of the weaker western developed oil importing nations like Greece, Spain and Italy.

No Global Oil Production Crash: What we do not think will happen and never did is that there will be a huge global oil production crash any time soon. We will not go off a Peak Oil cliff. Instead, the combined might of all oil producing countries pumping at maximum rate is more or less meeting demand. As the supply-demand situation tightens, then oil prices will rise and trigger economic slowdowns in China and India, with the USA stagnating and most of Europe going to recession. Most developed economies and oil exporting economies will continue to grow the OPEC exports will see their revenues rise of course at the expense of OECD countries with high oil imports and little manufacturing like Portugal, Spain and Greece.

Constraint to Western Growth: If there was a sharp drop in oil production, it would be caused by either a supply side disruption or demand destruction from very high oil prices and/or a major recession. One can see that global growth has to be constrained because no cheap oil is left. The days of steady 3% GDP growth in western developed nations is over gone dead it cannot happen without cheap oil the driver for such growth (unless there was a massive shift to cheap gas).

It all follows the classic super-cycle of a commodities bull run with supply constraints, inflation and more printed money every time the economy slows down this then feeds into high oil prices as a hedge against inflation and as a key raw material that all countries need.

So how does this all affect the property investor and what is the outlook?

Global Supply Struggle Even At $100/bbl. Well, we dont really see much change moving forward as far as new oil supplies coming on-stream and demand. Yes, there will be much hype about Bakken Oil Shale production from North Dakota but this is not going to significantly affect the supply picture. US oil imports will decline, but this will be more to do with demand destruction and high oil prices than high indigenous oil production not a good sign for the economy, rather the reverse albeit the increasing US oil production will of course help. But this is hardly surprising since everyone is drilling like crazy onshore because oil prices have been around $100/bbl for years now this has of course encouraged some excellent technological improvements and increasing reserves and flow rate that will help the USA in the future.

Giant Gas: Giant new gas finds have been made offshore Mozambique and Tanzania but the world really need more oil, not gas. If the world could rapidly convert as much oil consumption to gas as possible this would help the Peak Oil situation remarkably, but we dont see much sign of this shift from oil to gas not rapidly anyway. Almost all cars and trucks around the world burn gasoline (petrol) and diesel. Even if everyone has to change, it would take 25 years to convert the whole vehicle fleets most vehicles last ten years at least.

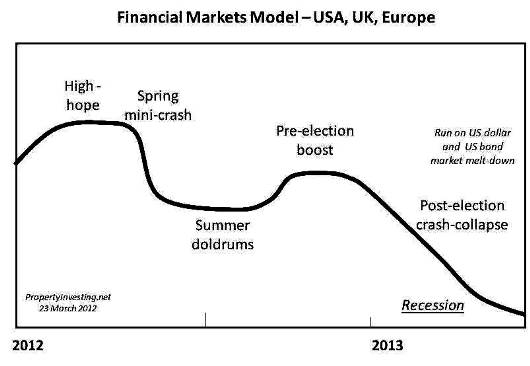

Iraq-Iran: As Iraq stabilizes over the coming years its oil production will continue to rise. Its now at 3.2 mln bbls/day as much as Iran. It will eventually rise probably to about 5 mln bbls/day by 2015. Meanwhile Irans oil production will drop probably to 2.5 mln bbl/day as sanctions kick-in. The Iranian nuclear issue has certainly not gone away its a festering that will likely explode some time just after the US Election in Nov 2012 once Obama has been re-elected. It will probably coincide we a major economic downturn in the USA in 2013. In a way, we see so many negative things all coming together in 2013 and high oil prices, high gold and silver prices and political and economic turmoil plus some wars. Something will surely happen between the USA, Iran and Israel in early 2013 and the turmoil will not be pretty. We could be mistaken on this, but really we think the USA is waiting until after the election to help their friends in Israel with solving this issue but what it will lead to is very high unstable spiking oil prices as markets get spooked by oil supply concerns similar to what happened in 1980. The most experienced investors will get rich from oil, silver and gold at this time the question is do you want to follow suit?

Early Stage of Peak Oil: So what we are living through but no-one is describing this is the early stages of Peak Oil as stressed build up around the world. Resource constraints. This is slowing economic activity, leading to riots, governments failing in the Arab countries with dwindling oil production (Yemen, Egypt, Syria) and European government changing in Greece, Italy, Spain and France notice all oil importing nations. The only re-elected person is Putin where Russia incidentally exports 8 mln bbls/day of oil and a similar in gas equivalent each day we dont think this is a coincidence.

Shift to Socialism: There will be a tendency for debt laden countries to swing to the left not wanting to face up to the severe crises in denial hankering for the prosperous past that is drifting away as high oil price cause high inflation, eroding living standards whilst the poor get poorer, food prices rise, wages stagnate and energy prices rise. As things get far worse as public sector expand, the risk is a lurch to the far right like Germany encountered in 1933 after the Weimer hyper-inflationary period caused a crisis.

So we expect more of the same moving into 2013 but just getting worse regrettably.

Focus on Physical: One of the only ways to prosper from this bleak economic outlook is to focus investments in:

· Oil, mining, commodities rich countries (stable) like Australia, Canada, Norway

· Only hold currency in safe haven currencies - like Australia, Canada, Norway

· Invest in oil, mining, commodities, hard physical assets

· Invest in gold and silver

Oil Towns: Invest in property as a hedge against inflation in areas positively exposed to Peak Oil crisis like Texas, North Dakota, NW Wyoming, London, Calgary, Perth, Houston, Sydney, Geneva, Monaco, Oslo, Aberdeen, Moscow, St Petersburg, Rio-Brazil

For the entrepreneur that likes to explore that next hot spots for property, consider following the new oil and gas discoveries around the world so consider East Africa, western sea-board of South America as examples. But beware of the pitfalls of investing in countries where corruption and legal practices are suspect.

Agriculture and Farmland: In the next ten years, there is likely to be a huge improvement in the fortunes of farming and farmers. The average age of a farmer in the USA, Australia and the UK is 58 a few years from retirement. The average age of a farmer in Japan is 66. At this rate, there will be no farmers left soon. Any youngest that can learn farming and get hold of so cheap land owned or rented could make serious money. In the 1990s it was trendy to be a financier-banker. In 2000 it was trendy to be a high-tech dot-com nerd. By 2020 it will be trendy to be a farmer. Yes, these are the people that will become prosperous as the bankers lose their jobs. Food prices will rise, agricultural products shortages will become pronounced as 7-8 billion people need feeding and energy prices rise. If you are young and like the out-door life, farming is something worth considering or any profession around farming whether this is selling tractors, seed, fertilizer, agricultural research. Farmland prices will rise strongly as money printing accelerates and wealthy investors view land as a key part of their physical portfolio. There will be a shift away from paper currency-debt to farmland and farming both giant agri-business and small scale local family farming.

Gold Silver Correction Opportunity: Anyone following the correction in the gold price from $1750 to $1550 and silver from $33 to $27.5 will we wandering whether the end of the gold-silver bull run has arrived. But we just see this as a correction on the way up and an excellent opportuni ty to buy low probably for the last time. It takes some nerve to buy now but in the silver and gold markets, the smaller investors are often shaken out at stages like this leaving the big players in the market who subsequently make a killing when the bull trend picks up again. We urge all small investors to hang in there if you can dont let the chicken little in you take hold. No-one can be certain, we cannot be certain either, but we just think governments will have to print even more money now and this will kick gold and silver prices even higher in the longer run. This is likely to happen in 2013 but for now we expect the correction to continue as hedge funds are forced to sell their prized gold and silver to cover their other investment positions. The US government will likely be quietly shorting the gold and silver market to try and beat it back down again to make the dollar look good in comparison. But eventually may be in 2013 these efforts will fail as peoples attention shifts from the broken Euro to the US dollar and their gigantic $15.2 Trillion debt and $75 Trillion unfunded liabilities that have no way of ever being paid back. The wall of printed money will one day hit the streets similar to what is happening in Greece, and people will then panic and try and get into physical assets like you have never seen before all at the same time. This will be the gold and silver bubble that eventually develops at which time it will be time to get out. But we are far away from this probably half way there. Not until silver is well over $100/ounce and gold is up around $4000-$6000/ounce should one seriously consider bailing out into another asset class. So the message is hold your nerve. Expect to see silver drop to say $25/ounce soon and gold to say $1400/ounce. But then they will bounce back.

ty to buy low probably for the last time. It takes some nerve to buy now but in the silver and gold markets, the smaller investors are often shaken out at stages like this leaving the big players in the market who subsequently make a killing when the bull trend picks up again. We urge all small investors to hang in there if you can dont let the chicken little in you take hold. No-one can be certain, we cannot be certain either, but we just think governments will have to print even more money now and this will kick gold and silver prices even higher in the longer run. This is likely to happen in 2013 but for now we expect the correction to continue as hedge funds are forced to sell their prized gold and silver to cover their other investment positions. The US government will likely be quietly shorting the gold and silver market to try and beat it back down again to make the dollar look good in comparison. But eventually may be in 2013 these efforts will fail as peoples attention shifts from the broken Euro to the US dollar and their gigantic $15.2 Trillion debt and $75 Trillion unfunded liabilities that have no way of ever being paid back. The wall of printed money will one day hit the streets similar to what is happening in Greece, and people will then panic and try and get into physical assets like you have never seen before all at the same time. This will be the gold and silver bubble that eventually develops at which time it will be time to get out. But we are far away from this probably half way there. Not until silver is well over $100/ounce and gold is up around $4000-$6000/ounce should one seriously consider bailing out into another asset class. So the message is hold your nerve. Expect to see silver drop to say $25/ounce soon and gold to say $1400/ounce. But then they will bounce back.