481: What Happened To Peak Oil - UK Inflation, Oil Prices and Property

07-19-2013

PropertyInvesting.net team![]()

Is

Peak Oil Dead? Interesting all the debate at the moment

about the end of the so call Peak Oil theory Peak Oil Is Dead and the like. Its

certainly true that total oil liquids production has been slowly rising as new

supplies have come on stream particularly from Canada (heavy oil) USA (oil

shale) in the last four years. What does this all mean? Does the world need to worry

about oil supplies anymore?

High

Oil Prices: Between 1980 and 2000 during the boom

years for western oil importing developed economies oil prices averaged

around $20/bbl. Then in 2000 the commodities bull run started and oil prices

climbed to $148/bbl in 2008 before collapsing during the financial crisis to

$60 and then rising back to a plateau of $100/bbl. Despite a ten fold increase

in oil prices, new supplies have only been growing at about 1.5% a year as the global

population and global GDP growth have averaged about 2% and 3%  respectively during the

last 15 years.

respectively during the

last 15 years.

Dollar

Printing: The US Fed recently pumped $3 Trillion into the global

economy they created inflation overseas whilst the dollar stayed reasonably

highly valued against most foreign currencies. This has added to costs and inflation all around the

globe the American have exported inflation, particularly to places like China. This has also help increase the

price of oil and the cost of oil extraction.

High

Oil Extraction Costs: The cost of oil extraction has skyrocketed

from about $6/bbl in 1999 to $70/bbl in 2013 for new oil developments. The key

aspect is that at oil prices levels of $100/bbl it makes large additional marginal resources

economic these can then be developed and transferred into producible and proven

reserves. Without high oil prices, supply would drop back sharply. These resources

are often unconventional heavy oil sands or oil from tight shale formations

or from deepwater offshore difficult to extract and highly energy intensity

resources.

Hydrocarbon Liquids a New Assortment: Total heavy oil sands production is now around 3 million barrels a day of the 90 million produced. On top of this, there is about 2.5 million barrels of oil from shale fracced horizontal wells. Then there is an additional 2 million barrels of natural gas liquids from shale gas fracced horizontal wells compared with ten years ago. Then there is another 2 million barrels of natural gas liquids from new big gas developments. On top of this, there is about 2 million barrels of biofuels from corn and sugar cane. If you take away all these new unconventional types of oil the conventional oil production has been in decline since 2002. So we are at Peak Conventional Oil, Peak Cheap Oil or Peak Easy Oil, but we not at Peak Oil thats all hydrocarbon liquids. It seems the global oil industry is able to keep pace at this time with demand as long as oil prices stay at about $100/bbl. If they slip, we would expect oil supplies to drop and development are cancelled and/or high cost oil producers are shut-in. But then, if oil prices rose to $150/bbl a new set of resources would be evaluated for development and activity levels would rise. This is like typical market-capital economics you increase the price then supply comes on stream. But the twist is like in gold and silver mining the prices have got to rise to make it economic to access these depleting resources. The easy oil has all but been produced. Recall in 1985, it cost Saudi Arabia 20 cents a barrel to produce their oil. But now it probably costs $5-$25/bbl - they are the low cost oil producer but even in Saudi Arabia because of higher maintenance costs, more wells, new water injection schemes, higher water cuts, oil processing costs and smaller new fields coming on stream.

OPEC

Oil: More non-OPEC oil is now being produced than

ever before from an increasing number of oil producing countries. But new

discoveries are small, incremental and large new basins are generally not being

opened up like Alaska and the North Sea in the 1970s-80s. Brazil's new oil reserves are deep, in deepwater at very high pressures - costing billions to develop. OPEC production this

month actually declined despite the increasing oil price almost certainly

because of political-social problems sweeping the Middle East-Levant-North Africa regions to name a few oil

producing countries affected: Syria, Nigeria, Libya, Egypt, Tunisia, Algeria

(one gas plant attack), Yemen and Iraq. Venezuela has major economic problems

and oil production that has halved since Chevaz gained power in 1999. Ecuador

is also languishing. The message is these production problems are not likely

to go away any time soon if anything, the instability is likely to worsen. So

we expect OPEC supplies to struggle. Meanwhile US and Canadian oil supplie s

will increase as more oil shale and oil sands deposits are developed. These two

forces might actually offset each other to a large extent.

s

will increase as more oil shale and oil sands deposits are developed. These two

forces might actually offset each other to a large extent.

Demand

Rise: But oil demand from the US is certainly on the rise

inventories are dropping, and European oil demand could pick up later in the

year if the economy starts to improve. China looks like their economy is

slowing dramatically but their oil demand will probably continue to rise as

industrialisation continues. Overall, we see a tightening of oil supplies and

increasing oil demand which will send oil prices higher again. This will give

the illusion of global growth but it will soon translate into higher

inflation and economic problems sometime in the next six months. As fuel and

food prices rise again, expect more riots in all countries particularly hot

developing nations that import oil and have no oil subsidies.

Skyrocketing

Oil Price: This brings us to the UK economy that is now very

exposed to increasing oil prices. Since Mark Carney became Governor of the Bank

of England, Sterling has crashed 7% against the dollar. This means oil prices

are 7% higher. Then the oil price has risen 13% in this short period of time

thats a 20% increase in oil prices in

Sterling terms in 4 weeks. Now it does not take a rocket scientist to predict

that this will feed rapidly through to UK inflation in the next few months.

Inflation will zoom up past 3% and head over 4% by year end thats our

prediction. Then the BoE will be writing letters to the Chancellor and blaming

it on a temporary external influences it cannot control and claim because of

this its all okay.

Oil

Imports Rise: Its particularly sad because the UK now

imports 50% of its oil needs and 65% of its gas needs and oil and gas

production crashed 19% in 2011 immediately after the Chancellor put up North Sea

oil taxes this killed off investment in the UK sector of the North Sea. It

then crashed a further 12% in 2012 a year later. This means the oil import bill

is far larger after this  33% production loss and this affects the balance of

payments deficits and sustainable debt levels. And this will only get worse as

the decline continues.

33% production loss and this affects the balance of

payments deficits and sustainable debt levels. And this will only get worse as

the decline continues.

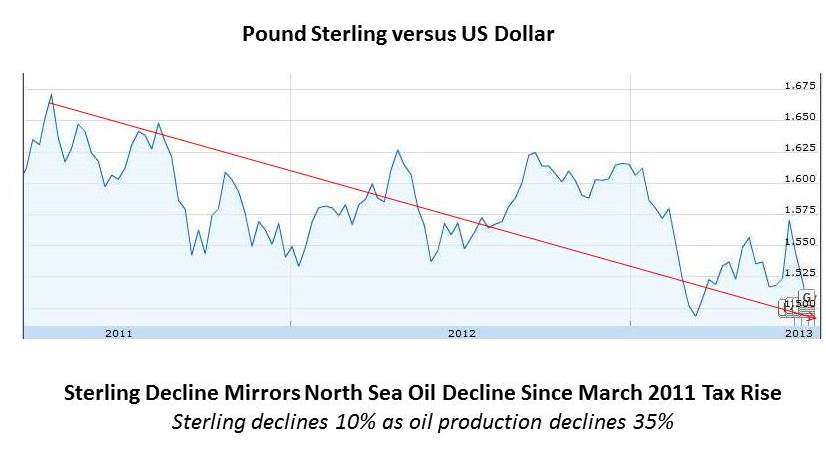

Sterling Slide: The UK Sterling used to be considered a petrocurrency in the 1980s and 1990s this has more or less ended now. Because of this, Sterling has declined and will continue its decline along with North Sea Oil. And because of this, oil prices in dollars rises. So we have a double whammy from lower North Sea oil production. Because the North Sea oil and gas production is bunched in with manufacturing when you hear about our manufacturing decline a large part of this is the decline in the value of the gas and oil being extracted from the North Sea. It seems no-one in the UK is really interested in this the oil and gas production crash and decline in tax revenues from the numerous Treasury tax increases over the years burdening oil and gas producers the largest companies all left a long time ago for higher returns in other countries with better fiscal terms.

Decline

in Oil Bad For Economy: Hope you can see that less oil

increases the deficit, increases borrowing, decreases the value of Sterling and

increases inflation. To prevent Sterling declining further and to control

inflation and interest rates may need to rise by year end so watch out. Of

course, if interest rates rose, then any economy recovery would be snuffed out

before it got going. This is the situation we are now in. It looks like

stagflation thats inflation at 4+%, wage inflation at 1.5% and rising

interest rates by year end if oil prices keep rising and Sterling keeps declining

on current trends.

This would then effect GDP growth that would be miserable might even turn negative again. Then property prices would be affected.

Feel Good Factors: What we are seeing is some

positive indicators feeding through the sunny weather is certainly helping

with the feel good factor and people are starting to spend money they have not

got again. But just as things look as if they might start getting back to

normal, our prediction is we will be hit by higher inflation and the economy

will then struggle.

We just have to hope and

pray bond yields dont start rising sharply because if this happens then

the public and private sector debt payments would skyrocket then a financial

collapse could start.

Work

Cut Out: Mark Carney

will really have his work cut out by year end trying to stabilize things. We

hope we are wrong and bond yields drop like they have been doing for the last

few weeks. But we fear the combination of:

·

Sterling weakness

·

Higher oil prices in dollar terms

·

Inflationary pressures

·

Weak wage growth

Will lead to stagflation

and more economic hardship with property prices levelling off and even

declining in some areas by year end.

Bond

Yield, Oil Price and Inflation Key Indicators: So keep an eye on oil prices and bond yields. Click

here save this link so you can check one in a while.

1. If

Sterling is stable, bond yields stay low and oil prices dont rise above

$105/bbl the property prices should continue to rise in London and provincial

areas

2. If

Sterling declines, bond yields rise sharply and oil prices rise well above

$105/bbl then property prices should level off and likely drop in London and

provincial areas

What will help stabilize

property prices in both scenarios is the government help to buy programme,

particularly when this is extended in Jan 2014 to used properties the last

thing the UK needs is a house price crash simply because so much private sector

equity and debt is held in property in the UK half the population would be

economically wiped out if the was a house price crash. Just as property prices

start to slow, this could create a boost to keep them from dropping.

Property

Prices: House prices have been rising slightly above inflation

in many areas of London (though not all) and below inflation in the rest of the country. What we have seen is an improvement in house prices but this is off

the back of a 25% drop after 2008. They have really only stabilized. Those

people wishing for prices to drop probably have not considered the economic

ramifications for the UK. When you look

at UK house prices as a whole, its only 25% of homes that are seeing any appreciable

price rises, and may be 5-10% of those home at levels above general inflation.

country. What we have seen is an improvement in house prices but this is off

the back of a 25% drop after 2008. They have really only stabilized. Those

people wishing for prices to drop probably have not considered the economic

ramifications for the UK. When you look

at UK house prices as a whole, its only 25% of homes that are seeing any appreciable

price rises, and may be 5-10% of those home at levels above general inflation.

In summary we have:

Inflation at 2.9%

(although its probably double this in un-manipulated real inflationary figures)

House prices rising at:

·

Northern Ireland 0%

·

NE England and Wales 1%

·

NW England, Yorkshire and Midlands 2%

·

East and Southern England 3%

·

London 5% (with Fulham at 13%, Battersea at

11% and Kensington at 10%)

Overall UK house price

inflation is about 4% - only 1% above the claimed inflation level. Thats hardly

a boom in prices or soaring prices as some articles suggest.

Ripple

Effect: If the economy stays stable with oil prices under

control, expect the ripple effect to spread from West London slowly to other

London areas then further out from London to provincial areas in a similar

way to what happened way back in 1987 then in 1997.

High

Oil Prices Will Kill Recovery and House Price Increases: But if oil prices rise to $120/bbl all bets

are off. Expect property prices to come under severe pressure with a high

chance of the bond market bubble popping.

Crude

Model: In crude terms non pun intended if oil prices

rise, inflation rises, interest rates need to rise then house prices drop. If

oil prices stay low, this boost economic growth in oil importing developed

nations, keeps inflation under control, leads to lower interest rates and

higher house prices. High oil prices are bad for property, as are high interest

rates and inflation getting out of control in a serious way along with a

currency crash.

We hope this Special Report has given you some good pointers to the way that oil prices, oil supply-demand then effect inflation and then property prices.