514: Recession on the Horizon Property Investors Positioning

08-21-2014

PropertyInvesting.net team![]()

Time for a Recession: The last financial crisis was in 2008 and its been six years now since the last major deflation and deep recession. It took the UK until early 2013 to really start mounting a significant economic recovery from a very low base after Labour exhausted the state financial coffers and left the Tory party an almighty financial mess to sort out in mid-2010. But its now time for another global slowdown or recession there are many things pointing in that direction.

Wars Breaking Out: One of the most concerning aspects of the global economy is the rising tensions and wars breaking out in the Middle East and Africa. These conflicts such as Iraq/Syria, Israel/Gaza, Libya, Ukraine, Central African Republic seem to be getting more common and widespread with mounting tensions. There is a definite risk of general regional wars breaking out. Northern Africa also has many more conflicts compared to 15 years ago. Decades of arms supply to disparate groups have led to running battles and conflicts civil strife, extremism and terrorism. This is helping cause a global economic slowdown in Europe as business and investors start to react by becoming more defensive. There is definitely a risk of deflation in the Euro-zone as the best and biggest growth spurt has come to an end. France in particular is close to an economic crisis.

Wars Breaking Out: One of the most concerning aspects of the global economy is the rising tensions and wars breaking out in the Middle East and Africa. These conflicts such as Iraq/Syria, Israel/Gaza, Libya, Ukraine, Central African Republic seem to be getting more common and widespread with mounting tensions. There is a definite risk of general regional wars breaking out. Northern Africa also has many more conflicts compared to 15 years ago. Decades of arms supply to disparate groups have led to running battles and conflicts civil strife, extremism and terrorism. This is helping cause a global economic slowdown in Europe as business and investors start to react by becoming more defensive. There is definitely a risk of deflation in the Euro-zone as the best and biggest growth spurt has come to an end. France in particular is close to an economic crisis.

China Debt: In China, the gigantic debt mountain and property bubble are a real risk to global financial stability. The tensions in the South China Sea certainly dont help. One day, this gigantic bubble will pop and then gold prices will probably go ballistic.

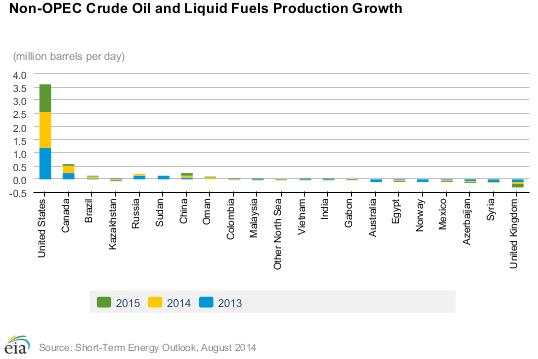

USA Oil Shale and Shale Gas: The USA has been saved by cheap gas and oil from the amazing technological developments of extracting gas and light oil from low permeability silts/shales/limestones using extended reach horizontal wells, and multiple hydraulic fraccing. Gas production has risen 35% since 2008 and another 3.5 million barrels of light oil a day has been put into the market by the USA since 2008.  These new petroleum supplies have prevented a gigantic oil price spike that would have happened after oil exporters slowed exports after the Arab Spring uprisings and ensuing wars and conflicts (e.g. Syria, Egypt, Tunisia, Libya, Yemen, Nigeria, Algeria to name a few). The 3 million barrels lost from conflicts has been replaced by 3.5 million barrels of shale oil from the USA. This new oil production has saved the dollar as the global reserve currency so far and reduced the US deficit along with providing massive new employment and investment opportunities in states like North Dakota and Texas. We cannot understate how important this has been for the US economy with the knock-on impact of tens of billions of dollars of oil investments throughout the nation bringing much need prosperity to some deprived rural areas.

These new petroleum supplies have prevented a gigantic oil price spike that would have happened after oil exporters slowed exports after the Arab Spring uprisings and ensuing wars and conflicts (e.g. Syria, Egypt, Tunisia, Libya, Yemen, Nigeria, Algeria to name a few). The 3 million barrels lost from conflicts has been replaced by 3.5 million barrels of shale oil from the USA. This new oil production has saved the dollar as the global reserve currency so far and reduced the US deficit along with providing massive new employment and investment opportunities in states like North Dakota and Texas. We cannot understate how important this has been for the US economy with the knock-on impact of tens of billions of dollars of oil investments throughout the nation bringing much need prosperity to some deprived rural areas.

UK Miserable Performance: US annual oil production growth has totalled 3.6 million bbl/day. Contrast this with the UK's miserable performance - having stopped fraccing in its tracks for the last 3 years and massively increasing North Sea taxes during a declining production period over the last 14 years - with three large hikes. The UK now produces 0.35 million bbls/day less than it did before the US oil shale boom occurred - this is the worst performing large oil producer in the world. This is a key reason why the UK deficit and borrowing continues to expand whilst the US deficit is declining rapidly. Both the Labour and Tory parties have hindered developments by raising taxes - "kill the goose that lay the golden egg" springs to mind.

Eventually More Money Printing: For the property investor, what is likely to happen is a slump in 2015 as deflation starts again. But this time, the central banks of the UK, USA and Europe will turn to the only lever they seem to have which is printing currency to prop up the financial system again. The waves of currency always end up manifesting themselves in higher property prices. After an initial correction property prices will inflate again. Their real value may not increase but they will increase in price in currency terms as a proportion to the amount of debt and/or printed currency in circulation.

Exported Dollars Causing Inflation: The giant amounts of printed dollars and pounds that were exported all around the world in 2008-2012 have been returning to global centres like London and New York for a few years now. If a correction takes place in 2015, the Central Banks will be quick to try and reverse this by printing more currency and allowing low priced debt-mortgages through the back door. They will do everything they can do using their global computer financial screens to prevent a fully fledged financial crash by printing currency.

Super Rich Elite: For smart investors and the super-rich, they will again use this printed zero cost currency to buy real estate because it is a physical asset that is an excellent hedge against inflation and currency printing. Currency printing tends to transfer wealth from the poor to the rich because food and fuel prices rise along with property prices. Since the rich have assets that inflate and the poor dont but have to buy fuel and food then they get disproportionately hit by currency printing. This is why the Wall Street Bankers love currency printing it gives them floods of zero cost currency to speculate/invest with and its far easier to make high returns when it cost nothing to borrow the currency. Any socialist like Paul Krugeman that encourages money printing is actually hindering the very people they claim to want to help by driving up food, fuel and rental prices for the poor whilst giving zero cost money for rich speculators to make high returns.

Super Rich Elite: For smart investors and the super-rich, they will again use this printed zero cost currency to buy real estate because it is a physical asset that is an excellent hedge against inflation and currency printing. Currency printing tends to transfer wealth from the poor to the rich because food and fuel prices rise along with property prices. Since the rich have assets that inflate and the poor dont but have to buy fuel and food then they get disproportionately hit by currency printing. This is why the Wall Street Bankers love currency printing it gives them floods of zero cost currency to speculate/invest with and its far easier to make high returns when it cost nothing to borrow the currency. Any socialist like Paul Krugeman that encourages money printing is actually hindering the very people they claim to want to help by driving up food, fuel and rental prices for the poor whilst giving zero cost money for rich speculators to make high returns.

Inflation All The Way: The impact of this new currency printing binge, likely starting in 2015, is higher gold and silver prices along with fine art and property, plus oil. This then feeds through to food prices and fuel prices then riots break out then civils wars/strife. We saw the cycle from the crash of 2008 to the present time, and we are likely to see it repeated once more starting in 2015. Its logical to think we are now at the end of a seven year cycle that started with a huge deflation the financial crash of 2008 and was then re-inflated with the trillions of dollars of currency printing creating the current financial bubble. This is likely to pop in the next 12 months and a new cycle will begin. Just like last time, as the world realises another recession is due to commence, the financial markets will crash then a renewed bout of currency printing with zero interest rates will commence.

Housing Recovery To Halt Under Labour: In the UK there is the start of a broad based housing recovery going on throughout the UK after early strong gains in London the so called ripple effect. However, Labour are likely to win power in May 2015 and this will almost certainly put property prices into reverse if Labour implement their anti-business and anti-wealth policies. The mansion tax will be implemented, then other property taxes and regulations, plus further regulations targeting Landlords and Londoners. The net effect will be lower property prices in London and rising rental costs as buy-to-let investors are dissuaded from doing business and Labour fail to build any more properties. Why do we think Labour will not build? Because there is no way they will have any public sector finances available to do so because the economy will be contracting and tax receipts will drop as taxes rise just like in France when the socialist got into power in 2012. Hence the rental market will tighten as mortgages become more difficult to access house prices will drop and rental demand rise - particularly lower end rentals. If the Tories either manage to achieve a Coalition or win a straight majority both scenarios we believe to be unlikely property prices would continue to rise only if the global economy did not tank.

Housing Recovery To Halt Under Labour: In the UK there is the start of a broad based housing recovery going on throughout the UK after early strong gains in London the so called ripple effect. However, Labour are likely to win power in May 2015 and this will almost certainly put property prices into reverse if Labour implement their anti-business and anti-wealth policies. The mansion tax will be implemented, then other property taxes and regulations, plus further regulations targeting Landlords and Londoners. The net effect will be lower property prices in London and rising rental costs as buy-to-let investors are dissuaded from doing business and Labour fail to build any more properties. Why do we think Labour will not build? Because there is no way they will have any public sector finances available to do so because the economy will be contracting and tax receipts will drop as taxes rise just like in France when the socialist got into power in 2012. Hence the rental market will tighten as mortgages become more difficult to access house prices will drop and rental demand rise - particularly lower end rentals. If the Tories either manage to achieve a Coalition or win a straight majority both scenarios we believe to be unlikely property prices would continue to rise only if the global economy did not tank.

Socialist Depression: As one can see with a likely Labour government along with a likely global recession now must be about the worst possible time to buy property in the UK for a first time buyer or property investor looking for high returns. The party is probably over after prices rose 20% in London in the last year and 10% the year before. Admittedly they have hardly moved in many parts of Britain but this is not about to change because business has not been performing particularly well despite lower unemployment. The public sector is also still in decline because the country simply cannot afford to keep half the population working on public services with depressingly low tax returns and weak private sector growth not being able to support this.

with a likely global recession now must be about the worst possible time to buy property in the UK for a first time buyer or property investor looking for high returns. The party is probably over after prices rose 20% in London in the last year and 10% the year before. Admittedly they have hardly moved in many parts of Britain but this is not about to change because business has not been performing particularly well despite lower unemployment. The public sector is also still in decline because the country simply cannot afford to keep half the population working on public services with depressingly low tax returns and weak private sector growth not being able to support this.

Renovation Low Risk Strategy: The safest form of property investment at the moment is renovation, extension and upgrade of existing property then sale of those units during this period when the sale market is reasonable strong. Examples are:

· Basement conversions in London houses valued at over £400,000 (each basement cost £100,000 hence it does not make economic sense unless the house is in a medium-high price bracket).

· Loft conversions if property value is >£250,000

· Kitchen upgrades and extensions

· Decoration

· Conversion of large rambling houses to multiple flats

· Adding of car port, off-street parking or garage in homes in busy expensive areas

· Demolishing a small house on a large plot and rebuilding with many homes on same plot

· Building of a house in part of a large garden or piece of portioned garden

Wage Growth: Its no surprize that wage growth is almost non-existent. The reasons are:

· More inward migration of people into the UK willing to work for less

· More difficulties for the unemployed wanting to stay on the dole meaning the unemployed are strongly encouraged to pick up any work - that is also low paid

· Politicians put pressure on companies to reduce large bonuses and high wages for higher earners like bankers

· The public sector has pressure on wage increases after cuts in public spending

· Competition from overseas workers and good availability of people willing to work part time or for low wages keeps a lid on wage inflation

· Older people and semi-retired are coming into the labour market to drive wages lower

· Many people are becoming self-employed and willing to work for low fees since their taxes are lower because of self-employed worker tax treatment compared with employees

· Most areas of employment have no skills shortage employers are happy to staff up as long as wages stay low

Its difficult to see wage pressures building in the medium term everyone seems to have gotten used to struggling by without much of a wage increase as the standard of living continues to decline for all but the super-rich. As oil prices drop and Sterling stays strong, this will combine to lead to lower prices in the next six months that will help prevent interest rates rise, albeit Sterling has dropped 7% against the dollar in the last six weeks which will put a bit of short term pressure on inflation. However, if Labour gets in, thinks will rapidly flip in the other direction. Wages will rise, Sterling will drop sharply by at least 20%, inflation will rise, interest rates will rise and a recession would then begin.

B uilding Recovery Would End Under Labour: Its most likely levels of home building starts will start to drop in the next few months as business uncertainty increases as the General Election gets closer. The property market could easily start to tank if Labour win power - home builders will be reluctant to take the risk of starting properties that they may not be able to sell particularly if lending becomes more difficult as would happen if Labour win power. Under a Labour government, financial markets would turn, lending would become more expensive, mortgages more difficult to secure and hence property prices would drop as confidence dropped this happened after the socialists got into power in France, and Ed Miliband and Ed Balls if anything are further left than Hollande and his cohorts and the UK has a worse financial deficit than France.

uilding Recovery Would End Under Labour: Its most likely levels of home building starts will start to drop in the next few months as business uncertainty increases as the General Election gets closer. The property market could easily start to tank if Labour win power - home builders will be reluctant to take the risk of starting properties that they may not be able to sell particularly if lending becomes more difficult as would happen if Labour win power. Under a Labour government, financial markets would turn, lending would become more expensive, mortgages more difficult to secure and hence property prices would drop as confidence dropped this happened after the socialists got into power in France, and Ed Miliband and Ed Balls if anything are further left than Hollande and his cohorts and the UK has a worse financial deficit than France.

Risks On Horizon: The above risks should be borne in mind for property investors, hence it would probably be rather foolish to invest in long term capital intensive projects at this time with so many uncertainties regarding the property market in the next 12 months.

We hope this Special Report is helpful to frame the overarching socio-economic environment as a backdrop to the property market, and how things could develop in the next year or so. If you have any queries or comments, please contact us on enquiries@propertyinvesting.net