699: Mean Reverting Commodities Companies versus High Growth Technology Companies

07-18-2021

PropertyInvesting.net team![]()

This Special Report describes on update on the commodities business and touches on how this compares with technology companies.

Commodities Companies: Oil and gas producers, gold, copper and silver miners and bulk agriculture producers tend to rise and fall in value along with the price of the commodities they produce. Some people refer them to mean reverting value" or "commodity stocks. In the oil business it's referred to boom and bust cycles. When a boom occurs in a commodity price, the market normally responds with oil companies drilling more wells and investing in the oil infrastructure to boost production capacity. If this then overshoots demand, oil or gas prices start to rapidly decline in response. As more projects start up, costs rise as shortages of equipment and skilled people hit the industry. This eats into profits and reduces efficiency but the price can be so high that huge profits can still be made. But if ver y large profits are made, host governments often increase their taxation they take a large slice of the pie. So even in boom times, western oil producers often have high but disappointing profits. Add to this the OPEC cartel that sets production supply for the OPEC countries around 32 million bbls of the 97 million produced in the world, then its always difficult to predict whether prices will rise or drop. OPEC remains a legal cartel 0 about the only legal cartel in the world because output is set by the Oil Ministers of the respective countries that join OPEC - with support from Russia that is not formally joined up to OPEC. Because this commodities market is of course manipulated by OPEC - this makes prediction the oil price based on simple supply and demand dynamics even more difficult.

y large profits are made, host governments often increase their taxation they take a large slice of the pie. So even in boom times, western oil producers often have high but disappointing profits. Add to this the OPEC cartel that sets production supply for the OPEC countries around 32 million bbls of the 97 million produced in the world, then its always difficult to predict whether prices will rise or drop. OPEC remains a legal cartel 0 about the only legal cartel in the world because output is set by the Oil Ministers of the respective countries that join OPEC - with support from Russia that is not formally joined up to OPEC. Because this commodities market is of course manipulated by OPEC - this makes prediction the oil price based on simple supply and demand dynamics even more difficult.

In summary you need to be very knowledgeable and lucky to predict oil and energy prices - and hence determine whether an energy stock might be shifting up or down. One thing is for sure whenever there is monumental currency printing spree like we have seen with the fiat dollar in 2009-2012 and again March 2020 onwards we get oil prices skyrocketing. People park their printed currency in inflation hedges and there is a strong correlation between the degree of currency printing and oil prices the more they print the higher the oil prices will rise - before investment catches up, the end of the cycle happens, oversupply ensues and oil prices crash again. The big question now - with the environmental pressures increasing - whether there will be enough oil investment to prevent the oil prices skyrocketing in 2022 onwards - causing a big negative inflationary impact in global economies.

Commodities Less Important in 2021: Years ago the western energy companies like Exxon, Shell and Chevron plus the gold miners constituted a gigantic part of western stock market indexes peaking at around 25% in 1981. But over time they have drifted down and now reside around 5%. On e could say they are way undervalued but the other side of the argument is that oil and gas has fallen way out of favour because of environmental (climate change) concerns. ESG (environment, societal and governance) committees that have been set up in the last few years are putting pressure on Boards, decision makers and banks to pull the plug on all investment in the oil and gas businesses - any investment that stimulates CO2 emissions. This we believe in the reason that despite oil prices rising to 75/bbl there has been very little response in the number of drilled well and almost no exploration taking place anymore. Many large integrated oil companies have actually stopped any wildcat exploration - starting late 2020. Okay, a few short term development wells - fracced horizontal wells - will be drilled onshore in the USA but expensive offshore exploration wells have died a death. Very little sign of significant new developments planned in places like Africa and South America.

e could say they are way undervalued but the other side of the argument is that oil and gas has fallen way out of favour because of environmental (climate change) concerns. ESG (environment, societal and governance) committees that have been set up in the last few years are putting pressure on Boards, decision makers and banks to pull the plug on all investment in the oil and gas businesses - any investment that stimulates CO2 emissions. This we believe in the reason that despite oil prices rising to 75/bbl there has been very little response in the number of drilled well and almost no exploration taking place anymore. Many large integrated oil companies have actually stopped any wildcat exploration - starting late 2020. Okay, a few short term development wells - fracced horizontal wells - will be drilled onshore in the USA but expensive offshore exploration wells have died a death. Very little sign of significant new developments planned in places like Africa and South America.

Cycles: This leads us onto our prediction that there will be a major oil supply shortage in a few years time because activity has been so severely hit by a combination of COVID-19 disruption to operations, lack of investment from banks with ESG pressures and inability of oil and gas companies to raise new capital as the ESG movement instead is telling them or encouraging them to transition as rapidly as possible clean energy renewables like solar, wind and green hydrogen. The large national oil companies - the OPEC countries - will not be able to respond to fill the gap. As oil prices rise, consumers all around the world are likely to accelerate the switch to renewables - low carbon energy - particularly solar and wind power and electric cars.

For investors what we are saying is that despite our prediction of rapidly increasing oil and gas prices in the western world the response by western oil companies will be muted and it  might not lead to hugely increase profits as their oil production rates continue to drop and gas production where profits tend to be lower does not take up the slack.

might not lead to hugely increase profits as their oil production rates continue to drop and gas production where profits tend to be lower does not take up the slack.

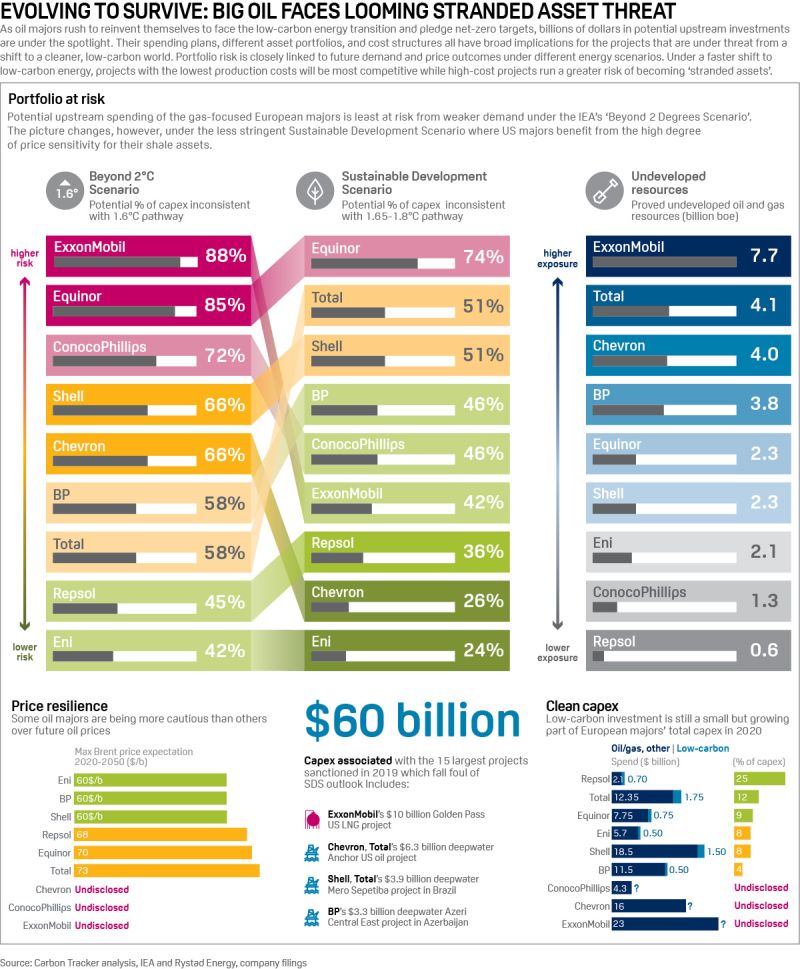

Oil Companies: A few examples of energy companies with a strong focussed presence in oil production that might do better than most are Chevron and Occidental these might be good value although the CO2 emissions will be increasingly highlighted. And because they are rather smaller than Exxon and Shell there might be less ESG pressures on these two companies to rapidly transition to renewables that tends to have far lower returns. But longer term, we believe investment in small and medium sized oil companies will become ever more problematical because so few investment banks and institutional investors will want to put funds into oil companies because of the environmental concerns and ESG pressures. The young bankers these days probably dont want, or might not want, to get involved in investing in what many believe to be dirty industries. These smaller oil companies might eventually become private bought by private equity houses that allow themselves to invest in oil exploration and production. The larger oil companies are actually energy companies integrated and many are shifting into renewables and embracing the so called energy transition. Overall the energy companies have been declining in their share of the overall stock market - market capitalisation for decades now and we believe this is likely to continue. This listing below shows - according to "Carbon Tracker" which companies are the most at risk of stranded assets.

Gold and Silver: Now lets switch to gold and silver producers. A similar story takes place in this industry. It's difficult to predict gold prices. They tend to drop when interest rates rise because savers get a more decent rate for their idle cash. But when the currency printers are going at full blast and interest rates are very low gold prices tend to rise sharply. But despite the gigantic currency printing and ultra-low interest rates gold prices have only risen from £1350/ounce to $1800/ounce pretty meagre considering the circumstances. The other times gold often rises is when there is a massive deflationary panic period but gold actually dropped in March 2020 at the height of the COVID-19 panic presumably people were forced or elected to liquidate assets in desperation and gold was one of them, along with Bitcoin.

Digital Gold vs Gold: Most gold miners have mining processing costs of $800-1100/ounce so with gold at $1800/ounce returns are good and activity has stepped up. Gold production should rise, but as it does if demand does not increase prices could actually drop. The other angle to gold these days is that many people believe that Bitcoin is eating away at golds overall $10 Trillion market value as a "digital safe haven" store of wealth. People call Bitcoin digital gold. This investment angle is not likely to go away most likely it will get more significant. The upside is investing in high quality gold miners that prosper when gold prices rise or rocket one day. But investors have been waiting for years to seek out high returns in the gold mining business most small gold miners destroy value. The largest have large mar ket caps already and might rise faster than the gold price but they have not given stellar returns like many of the high tech companies like Amazon, Tesla, Facebook, Twitter, Google or Apple. The largest gold miners have a tenth of the market cap compared to these giant players and frankly people would laugh if you ever suggested a gold miner could get to $1 Trillion value like most of these 6 companies have.

ket caps already and might rise faster than the gold price but they have not given stellar returns like many of the high tech companies like Amazon, Tesla, Facebook, Twitter, Google or Apple. The largest gold miners have a tenth of the market cap compared to these giant players and frankly people would laugh if you ever suggested a gold miner could get to $1 Trillion value like most of these 6 companies have.

In Summary gold prices are likely to rise as currency printing continues and fiat debasement continues with it as a hedge against serious inflation. But just for example on 13 July 2021 the Fed advised inflation was 5.4% - another shocking month, but the gold price did not budge from $1810/ounce.

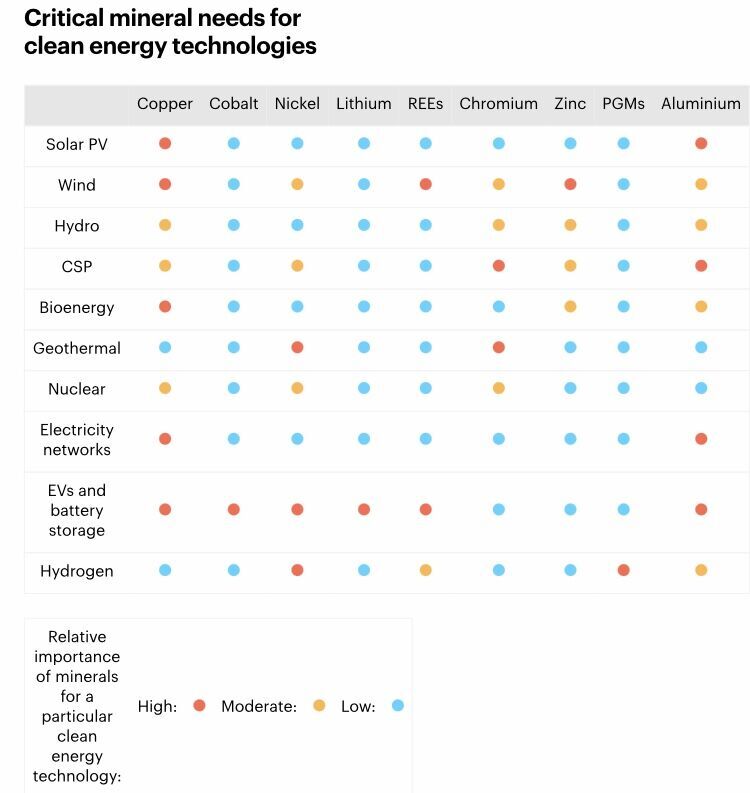

Metals Copper, Nickel, Tin and Rare Earths: Metal prices such as copper and nickel tend to rise far higher when the economies are booming and crash down when there is a major recession or slow down in economic growth. Fiat currency printing tends to stimulate commodity prices like oil, gold and copper as well. However, we have some interesting conditions for copper, tin, silver, nickel and rare earth prices at the moment because of the combined massive monetary stimulus and the start of what many people believe is a super cycle of growth cause by the electrification of so many things electric vehicles, solar, wind and the renewables boom. Below is handy table showing which metals are required for which renewable energy business. For sure, - wind, solar and electric cars are going to boom so if you invest in the successful miners that supply the batteries and electric cables with raw materials its likely to be a lucrative investment. Its certainly worth researching.

High Technology: Finally we want to describe how these industrial sectors compare with the technology sector. Below are some example of technology sub-sectors that have seen gigantic growth in the last 20 years:

Crypto Assets Bitcoin, Ethereum

Artificial Intelligence Tesla, Google

Data Analytics and Cloud Computing Google, Amazon, Microsoft

Social Media Facebook, Twitter, Instagram, TikTok

Retail Internet Shopping ebay, Amazon

iPhones and Apps Apple, Samsung

Quantum Computing

Gnome-DNA Biotech

Electric Cars Tesla, Nio, VW

Energy storage-Batteries

Renewable Energy solar, wind, hydrogen - Dong, RWE, ITM Power

Adoption Curve: These technology companies tend to start small with early adoption, then they hit the 8-10% adoption curve then go ballistic in sales, adoption and market penetration. For example, Crypto Asset adoption globally is around 6% - its just about to hit the sweat spot of 8-10% when there is exponential growth. Electric cars are the same overall adoption globally is around 6% - with some countries running at 25% (Norway) whist many African countries are down at the 0-5%. Electric cars are about to hit their sweat spot. This is also true of solar power and wind power. This is one reason why we are so bullish on mining of copper, nickel, tin and rare earths all required to produce renewable energy and electric cars and batteries.

Breakthrough: When a technology starts to break out into the high growth adoption it normally goes from 105 to 70% global adoption with 5-8 years. This is when fortunes are made. But if there are ten companies vying for stop spot, normally one of them gets hold of say 40-50% market share because they have the best technology, platform and network then they crush the opposition. Examples are Apple, Facebook, Amazon, Google the so call FANG stocks. So the big question for all investors is can you spot the next FANG stock to invest in. If you spot it early and hold onto it you will make huge profits. For examples, you might bet on Nio which is a successful Chinese electric car manufacturer - it could be huge one day. Many Americans are investing in Telsa because they think they could dominate electric car manufacturing. In Europe people often invest in Volkswagen because they believe in their long term electric vehicle manufacturing strategy.

So we hope we have give you a summary about why commodities tend to go in cycles that are mean reverting whilst technology companies often go meteoric in growth and continue to boom as adoption increased from 10 to 90% - with the most dominant company often destroying most of the competition getting 50% or more market share like Amazon, Google, Apple and Facebook.

We hope you have found this Special Report insightful. If you have any queries, please contact us on enquiries@propertyinvesting.net .